Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

This Spring Presents Sellers with a Golden Opportunity

If you’re thinking of selling your house this year, timing is crucial. After all, you’ll want to balance getting the most out of the sale of your current home and making the best investment when you buy your next one.

If that’s the case, you should know – you may be able to get the best of both worlds today. Here are four reasons why this spring may be your golden window of opportunity.

1. The Number of Homes on the Market Is Still Low

Today’s limited supply of houses for sale is putting sellers in the driver’s seat. There are far more buyers in the market today than there are homes available. That means purchasers are eagerly waiting for your house.

Listing your house now makes it the center of attention. And if you work with a real estate professional to price your house correctly, you can expect it to sell quickly and likely get multiple strong offers this season.

2. Your Equity Is Growing in Record Amounts

According to the most recent Homeowner Equity Insight report from CoreLogic, homeowners are sitting on record amounts of equity thanks to recent home price appreciation. The report finds that the average homeowner has gained $55,300 in equity over the past year.

That much equity can open doors for you to make a move. If you’ve been holding off on selling because you’re worried about how rising prices will impact your next home search, rest assured your equity can help fuel your move. It may be just what you need to cover a large portion – if not all – of the down payment on your next home.

3. Mortgage Rates Are Increasing

While it’s true mortgage rates have already been climbing this year, current mortgage rates are still below what they’ve been in recent decades. In the 2000s, the average mortgage rate was 6.27%. In the 1990s, the average rate was 8.12%.

For context, the current average 30-year fixed mortgage rate, according to Freddie Mac, is 3.85%. And while recent global uncertainty caused rates to dip slightly in the near-term, experts project rates will rise in the months ahead. Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, says:

“For homebuyers, we believe that borrowing costs will likely rise with the increase in mortgage rates….”

When that happens, it’ll cost you more to purchase your next home. That’s why it’s important to act now if you’re ready to sell. Work with a trusted advisor to kickstart the process so you can take key steps to making your next purchase before rates climb further.

4. Home Prices Are Climbing Too

Home prices have been skyrocketing in recent years because of the imbalance of supply and demand. And as long as that imbalance continues, so will the rise in home values.

What does that mean for you? If you’re selling so you can move into the home of your dreams or downsize into something that better suits your current needs, you have an opportunity to get ahead of the curve by leveraging your growing equity and purchasing your next home before prices climb higher.

And, once you make your purchase, you can find peace of mind in knowing ongoing home price appreciation is growing the value of your new investment.

Bottom Line

If you want to win when you sell and when you buy, this spring could be your golden opportunity. Let’s connect so you have the insights you need to take advantage of today’s incredible sellers’ market.

How To Navigate a Market Where Multiple Offers Is the New Normal

If you’re thinking of buying a home today, you already know that the number of homes available for sale is low. But what does that really mean for you? As a buyer, low housing supply coupled with high buyer demand means you should be prepared to navigate a highly competitive market where homes sell fast and get multiple offers. Realtor.com has this to say:

“Homes also flew off the market at record pace as buyers put offers in the moment properties came up for sale….”

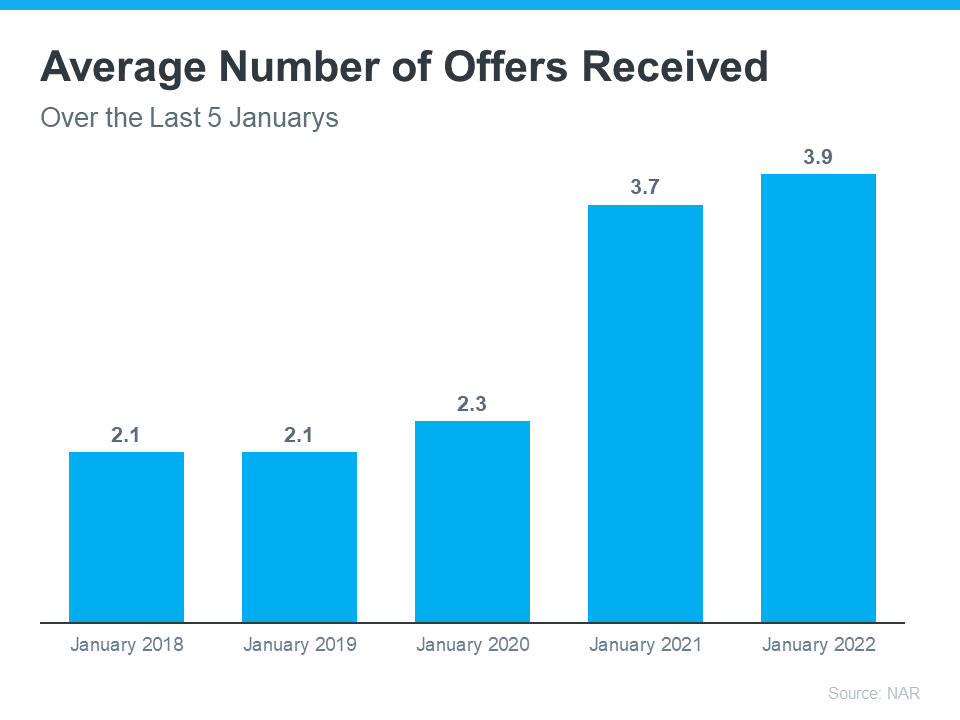

In a bidding war situation like this, doing everything you can to get ahead of the competition is a wise move. That’s because when you find a house and submit an offer, it’ll likely be up against strong offers from other buyers. According to the latest RealtorsConfidence Index from the National Association of Realtors (NAR), homes today are receiving an average of 3.9 offers. That’s the most offers we’ve seen in January for the last 5 years (see graph below):

To help you navigate bidding wars with multiple offers, an expert real estate advisor is key. They know what’s worked for other buyers, what sellers are looking for, and how to help you prepare when it comes time to make an offer. Here are three tips to keep in mind that will help you make the best offer possible.

1. Know Your Numbers

Knowing your budget and what you can afford is critical to your success as a homebuyer. The best way to understand your numbers is to work with a lender so you can get pre-approved for a loan. Pre-approval shows sellers you’re serious, which can give you a competitive edge. You should also know making an offer at the home’s asking price may not be enough. Homes today often sell for more than their listing price. An agent can help you understand the market value of the home and what other homes are selling for in your area.

2. Be Ready To Move Fast

Speed and the pace of sales are contributing factors to today’s competitive housing market. When homes are selling fast, it’s important to stay on top of the market and be ready to move quickly. Your agent will help you stay up to date on the latest listings and help you put together your best offer as soon as you find the home you want to buy.

3. Make a Strong but Fair Offer

When you’re up against other offers, putting your best offer forward from the start is key. Lean on your agent to write a strong offer and use their expertise on which levers you can pull to make your offer as enticing as possible. One option is to wave some of your contract contingencies (conditions you set that the seller must meet for the purchase to be finalized). Just remember there are certain contingencies you don’t want to give up, like the home inspection.

Bottom Line

No matter what, your agent is your best resource for making an offer that stands out in a competitive market. Let’s connect to talk through what you can expect as a buyer and how to kick off a successful home search.

Key Factors That Impact Affordability Today

You can’t read an article about residential real estate without the author mentioning the affordability challenges that today’s buyers face. There’s no doubt homes are less affordable today than they were over the last two years, but that doesn’t mean homes are now unaffordable.

There are three measures used to establish home affordability: home prices, mortgage rates, and wages. Let’s look closely at each of these components.

1. Home Prices

The most recent Home Price Insights report by CoreLogic shows home values have increased by 19.1% from last January to this January. That was one reason affordability declined over the past year.

2. Mortgage Rates

While the current global uncertainty makes it difficult to project mortgage rates, we do know current rates are almost one full percentage point higher than they were last year. According to Freddie Mac, the average monthly rate for last February was 2.81%. This February it was 3.76%. That increase in the mortgage rate also contributes to homes being less affordable than they were last year.

3. Wages

The one big, positive component in the affordability equation is an increase in American wages. In a recent article by RealtyTrac, Peter Miller addresses that point:

“Prices are up, but what about wages? ADP reports that job holder incomes increased 5.9% last year but rose 8.0% for those who switched employers. In effect, some of the higher cost to buy a home has been offset by more cash income.”

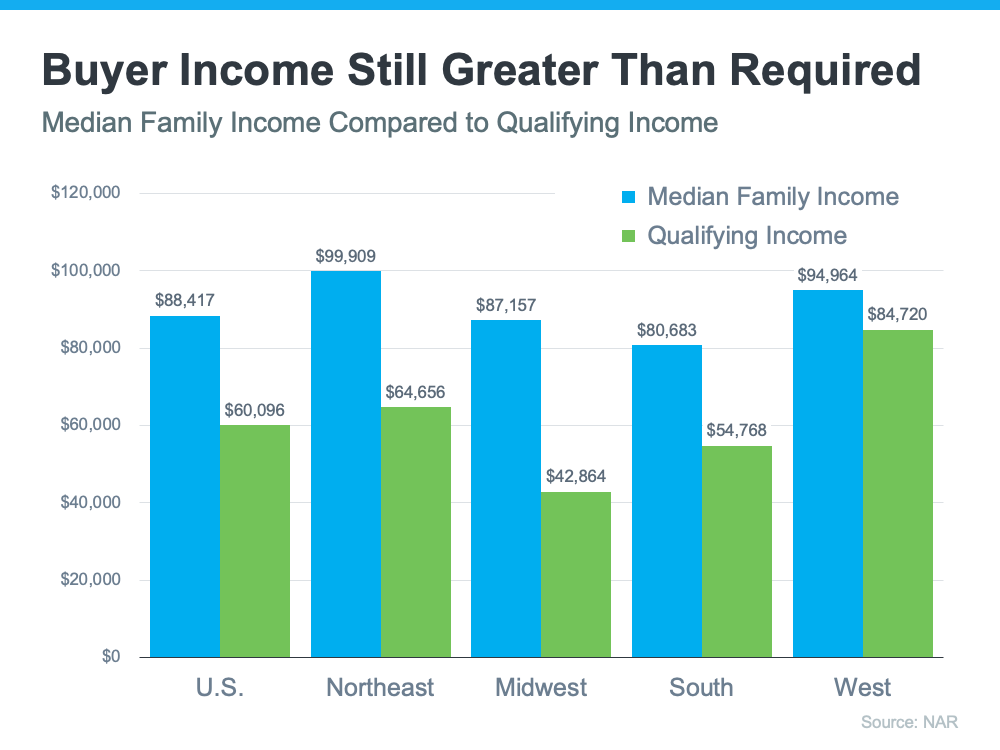

The National Association of Realtors (NAR) also recently released information that looks at income and affordability. The NAR data provides a comparison of the current median family income versus the qualifying income for a median-priced home in each region of the country. Here’s a graph of their findings:

As the graph shows, the median family income (shown in blue on the graph) is greater than the qualifying income needed to buy a median-priced home (shown in green on the graph) in all four regions of the country. While those figures may vary in certain locations within each region, it’s important to note that, in most of the country, homes are still affordable.

So, when you think about affordability, remember that the picture includes more than just home prices and mortgage rates. When prices rise and rates rise, it does impact affordability, and experts project both of those things will climb in the months ahead. That’s why it’s less affordable to buy a home than it was over the past two years when prices and rates were lower than they are today. But wages need to be factored into affordability as well. Because wages have been rising, they’re a big reason that, while less affordable, homes are not unaffordable today.

Bottom Line

To find out more about affordability in our local area, let’s discuss where home prices are locally, what’s happening with mortgage rates, and get you in contact with a lender so you can make an informed financial decision. Remember, while less affordable, homes are not unaffordable, which still gives you an opportunity to buy today.

Are Home Prices Continuing To Rise?

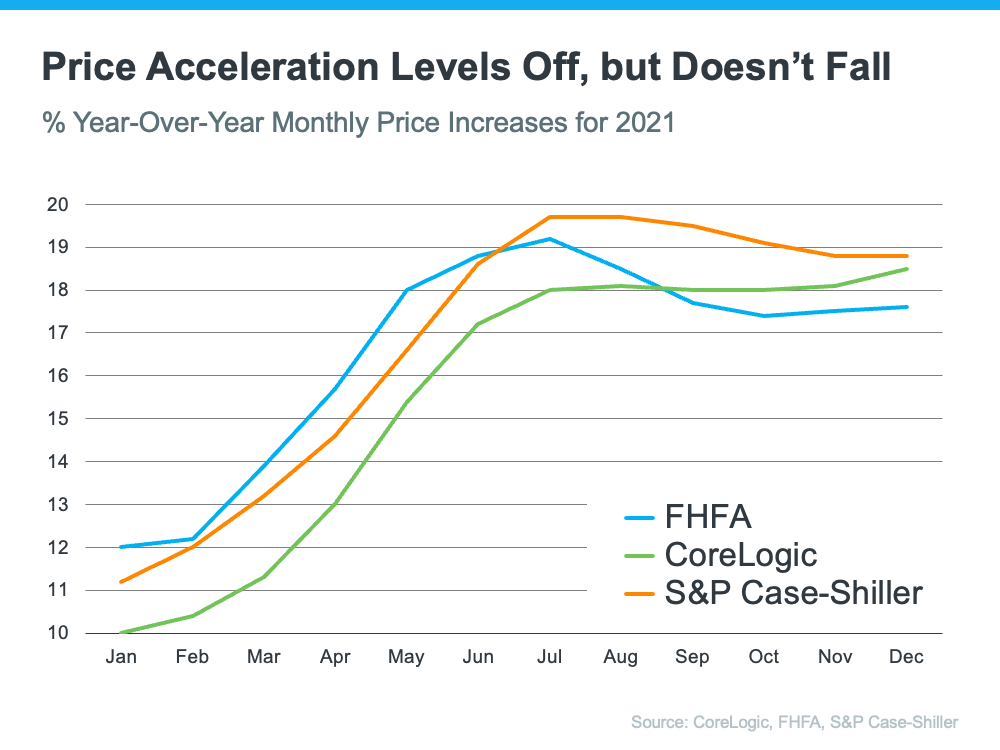

Many analysts projected home price appreciation would slow dramatically in the fall of 2021 and then continue to soften throughout 2022. So far, that hasn’t happened. The major price indices are all revealing ongoing double-digit price appreciation. Here’s a look at their reports on year-over-year price appreciation for December:

- Federal Housing Finance Agency (FHFA): 17.6%

- S&P Case-Shiller: 18.8%

- CoreLogic: 18.5%

To show that they’re not seeing signs of softening, here’s a graph that gives the progression of all three indices for each month of 2021.

As the graph above reveals, last year, home price appreciation accelerated dramatically from January to July according to all three indices. Then, it began to decelerate in August when prices appreciated at a slower pace, but it didn’t decline. Many thought that would be the beginning of a rapid slowdown in the level of home price appreciation, but as the data shows, that wasn’t the case. Instead, prices began to level off for a few months before two of the three indices saw appreciation re-accelerate again in December.

To clarify, deceleration is not the same as depreciation. Acceleration means prices rise at a greater year-over-year pace than the previous month. Deceleration means home values continue to rise but at a slower pace of year-over-year appreciation. Depreciation means prices drop below current values. No one is forecasting that to happen.

In fact, the FHFA revealed that price appreciation accelerated in December in six of the nine regions it tracks. Case Shiller showed that appreciation accelerated in 15 of the 20 metros they report on. As Selma Hepp, Deputy Chief Economist at CoreLogic, explains:

“After some signs of slowing home price growth . . . monthly price growth re-accelerated again, indicating home buyers have not yet thrown in the towel.”

What Does This Mean for You?

Whether you’re a first-time purchaser or someone looking to sell your current house and buy a home that better fits your needs, waiting to decide what to do will cost you in two ways:

- Mortgage rates are forecast to rise this year.

- Home prices should continue to appreciate at double-digit levels for some time.

If you wait, rising mortgage rates and high home price appreciation will have a dramatic impact on your monthly mortgage payment.

Bottom Line

Maybe the best thing to do is listen to the advice of Len Kiefer, Deputy Chief Economist at Freddie Mac:

“If you’re thinking about waiting until next year and that maybe rates are higher, but you’ll get a deal on prices – well that’s risky. It may be more advantageous to purchase this year relative to waiting until 2023 at this time.”

Down Payment Assistance Programs Can Help You Achieve Homeownership

For many homebuyers, the thought of saving for a down payment can feel daunting, especially in today’s market. That’s why, when asked what they find most difficult in the homebuying process, some buyers say it’s one of the hardest steps on the path to homeownership. Data from the National Association of Realtors (NAR) shows:

“For first-time home buyers, 29 percent said saving for a downpayment [sic] was the most difficult step in the process.”

If you’re finding that your down payment is your biggest hurdle, the good news is there are many down payment assistance programs available that can help you achieve your goals. The key is understanding where to look and learning what options are available. Here’s some information that can help.

First-Time and Repeat Buyers Are Often Eligible

According to downpaymentresource.com, there are thousands of financial assistance programs available for homebuyers, like affordable mortgage options for first-time buyers. But, of the many programs that are available, down payment assistance options make up the large majority. They say 73% of the assistance available to homebuyers is there to help you with your down payment.

And it’s not just first-time homebuyers that are eligible for these programs. Downpaymentresource.com notes:

“You don’t have to be a first-time buyer. Over 38% of all programs are for repeat homebuyers who have owned a home in the last 3 years.”

That means no matter where you are in your homeownership journey, there could be an option available for you.

There Are Local Programs and Specialized Programs for Public Servants

There are also multiple down payment assistance resources designed to help those who serve our communities. Teacher Next Door is one of those programs:

“The Teacher Next Door Program was designed to increase home ownership among teachers and other public servants, support community development and increase access to affordable housing free from discrimination.”

Teacher Next Door is just one program that seeks to help teachers, first responders, health providers, government employees, active-duty military personnel, and veterans reach their down payment goals.

And, most importantly, even if you don’t qualify for these types of specialized programs, there are many federal, state, and local programs available for you to explore. And the best way to do that is to connect with a local real estate professional to learn more about what’s available in your area.

Bottom Line

If saving for a down payment seems daunting, there are programs available that can help. And if you work to serve our community, there may be even more opportunities available to you. To learn more about your options, let’s connect so you can start your homebuying journey today.

Geoff and Joe Green – Son & Father Together Again

Forty years after founding his own brokerage, Joe Green has joined his son’s company. And father and son are a force to be reckoned with.

In Orange County, NY the name Green is synonymous with Real Estate. Furthermore, it is associated with exceptional client service. Joseph Green Realtor was founded in 1978, and 27 years later that’s where Geoff Green began his career. That’s where Geoff learned from some of the best in the business – his mom and dad, Marie Pennings and Joe Green.

Eventually Geoff did what kids do. He decided to spread his wings. And in 2005, Geoff founded Green Team New York Realty.

Meet Joe Green

Joe didn’t start out wanting to be in the real estate business. Rather, his goal was to teach. He taught physical education and coached football in Warwick. His wife, Marie, was a registered, part-time nurse.

Joe loved what he was doing, but back in 1974 a teacher’s salary wasn’t enough to support a family with 5 kids. Since he needed to supplement his income, Joe saw real estate as a way to make extra money if he worked hard at it

Finding His Calling

However, once he got into it, he discovered he’d found his calling. Because it wasn’t just about making more money. It was about meeting new people, and the adventure that came with each unique transaction. Maybe the most important aspect was that helping people was becoming emotionally rewarding. Marie also got her license, and real estate became a family affair.

In 1980, Joe and Marie decided it was time to go into real estate full-time. They purchased the building at 7 Main Street in Warwick. In 1982 they bought a building in Goshen and opened their 2nd office. Finally, they expanded into Washingtonville.

Life is what happens while you’re busy making plans

When Geoff was in the third grade, everything changed. Joe and Marie divorced, and the children went to live with their mom. While divorce is hard for the parents, it is also difficult for the children.

But life goes on, even when families are divided. Joe continued to build his real estate business, but found that divorce wasn’t the only hardship. In 1987 the housing market tanked, and they had to downsize. Marie took over the Warwick office. Joe closed down the Washingtonville office and kept the Goshen office. Despite all of the hardships Joe persisted.

Experience that spans decades

Joe has been in this ever-changing profession for over 40 years. Back in 1974, when Joe first started practicing, everything was open listing. Clients would call several brokers and they’d all be in direct competition with each other. Then MLS came along and exclusive right to sell became the norm. One brokerage firm tried to impress Joe with the latest in technology, which would change the way business was done. And so, Joe received his introduction to the fax machine.

However, it’s the experience that counts. And Joe and his team provided a full complement of real estate services. That included residential, commercial, land, farm and ranch sales, investment sales, leasing, property management, residential appraising, financial and legal referral services, and relocation services. They covered Orange, Rockland, Westchester, Sullivan and Ulster Counties. Furthermore, his expertise and vision helped to safely guide his clients through some very difficult economic cycles.

Change in the Air

In 2013 Joe decided to shut down the Goshen office and moved his Agency to Chester. However, he began to see that the key to a successful brokerage was technology. And his son was a master at using technology to grow his business. When Geoff opened his own office in 2005, at the 7 Main Street location, Joe couldn’t have been prouder or more excited.

And through the years, he saw what was happening at the Green Team. Technology was enhancing the way brokers worked. Consequently, Joe decided that it was time to join forces with his son and combine the best of both worlds. Each man brings incredible experience and expertise. Together, there is no stopping them.

And Joe doesn’t come to the Green Team alone. He brings with him three of his best agents. Cam Monaco has been with Joe for 30 years. While Krissy Many is newer to the business, she’s a powerhouse. And Vilma Lawla is also excited to be part of the Green Team.

The Future Looks Bright

Joe looks forward to sharing his knowledge. His advice? “Every day you can learn something new. Be like a sponge. Do it your way. Don’t copy but learn from everyone else. Experience can help some of the more inexperienced.” And Joe hopes that his years of experience will help newer agents.

Geoff is excited about having his dad join the firm, “I can’t explain how blessed I feel that Pop is now part of our Agency. It’s amazing to not only see him around the office, but to watch him doing what he does best: sharing his wisdom. Pop is one of the most experienced Real Estate Brokers I know. It’s a simple fact that our Agency just got a lot better as a result of Pop deciding to come on board with the Green Team.”

The two men respect each other and their individual contributions to the industry and their community. They look forward to combining over 50 years of experience and forging a new beginning. They are indeed a force to be reckoned with.

Thanksgiving Pie – A Green Team Tradition

Thanksgiving Pie – A Green Team Tradition

Thanksgiving. It’s a time of gratitude, friends and family; of turkey and all the trimmings. And at the Green Team, it’s a time to let clients know how much they are valued. The Client Appreciation Program, or CAP, is the cornerstone of the Green Team’s foundation. The Green Team doesn’t take its clients for granted. Through the CAP program sales associates find ways to say “I appreciate you” throughout the year. However, one of the highlights of the program is Thanksgiving Pie. A Green Team CAP tradition, clients are invited to come to the office for a casual party. And to pick up their Thanksgiving pie. Because this gift from their sales associate is a way of saying “Thank You.” Thank you for your business, your referrals, and your friendship.

Thanksgiving. It’s a time of gratitude, friends and family; of turkey and all the trimmings. And at the Green Team, it’s a time to let clients know how much they are valued. The Client Appreciation Program, or CAP, is the cornerstone of the Green Team’s foundation. The Green Team doesn’t take its clients for granted. Through the CAP program sales associates find ways to say “I appreciate you” throughout the year. However, one of the highlights of the program is Thanksgiving Pie. A Green Team CAP tradition, clients are invited to come to the office for a casual party. And to pick up their Thanksgiving pie. Because this gift from their sales associate is a way of saying “Thank You.” Thank you for your business, your referrals, and your friendship.

Thanksgiving Pie… A “family” event for both the Warwick and Vernon Offices

Walking into either office you can feel the warmth and joy and know that you are welcome. Pies are stacked high, waiting to be distributed. Being a local brokerage, it’s important to the Green Team to support other local businesses. Thus Noble Pies has become part of the tradition. Their pies are baked from locally sourced ingredients when available. Cider, wine, donuts and more await the clients as they drop in to pick up their pies. And, of course, there is laughter; lots of laughter!

important to the Green Team to support other local businesses. Thus Noble Pies has become part of the tradition. Their pies are baked from locally sourced ingredients when available. Cider, wine, donuts and more await the clients as they drop in to pick up their pies. And, of course, there is laughter; lots of laughter!

Green Team Sales Associates agree that the Client Appreciation Program is something they themselves appreciate. It keeps the focus on the people who are most important to their businesses: their clients. And events like this one bring everyone together, strengthening bonds between associates and between clients and associates. Probably one of the best things is that two days later pies from the Green Team’s sales associates will be sweetening Thanksgiving Dinners at many homes. Again letting clients know how much they are appreciated.

October 2018 Housing Market Update

The Green Team’s October 2018 Housing Market Update was held live on Facebook Tuesday, October 16 at 2 p.m. If you missed the live webinar, you can view it at your convenience by clicking here.

You can also sign up for future updates at GreenTeamHQ.com/hmu

Meet this month’s Panelists from Green Team New Jersey Realty and Green Team Home Selling System

Geoffrey Green, President/Broker of Green Team Home Selling System, is the moderator of the monthly webinar and presents stats and market updates for Orange and Sussex County. He is joined this month by Keren Gonen, Pamela Zachowski and Alison Miller of Green Team New Jersey Realty in Vernon and Jacqueline Kraszewski of Green Team Home Selling System in Warwick.

Market Update – The National Perspective

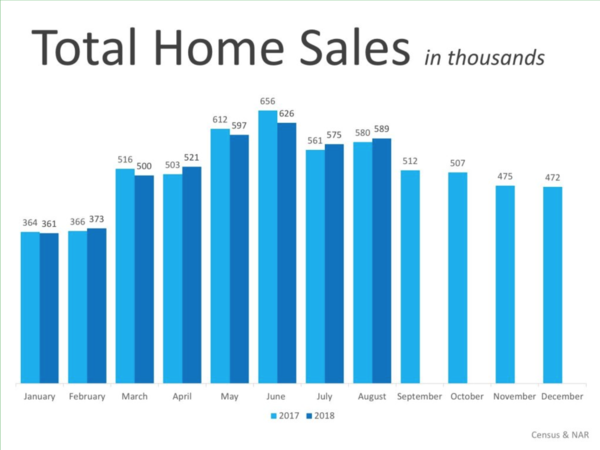

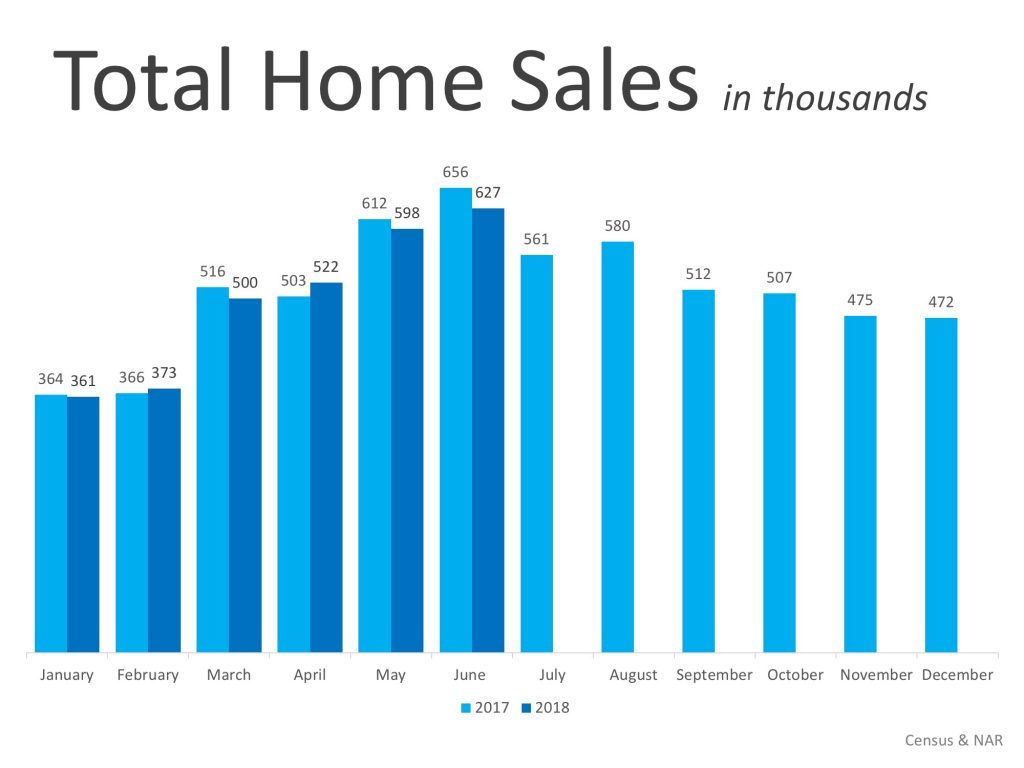

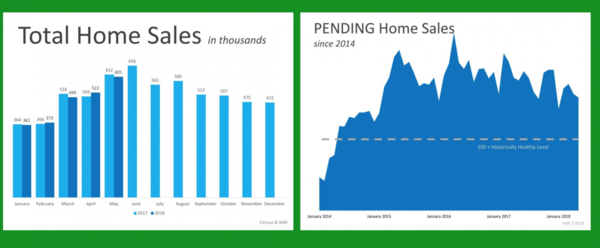

A look at Total Home Sales Nationally

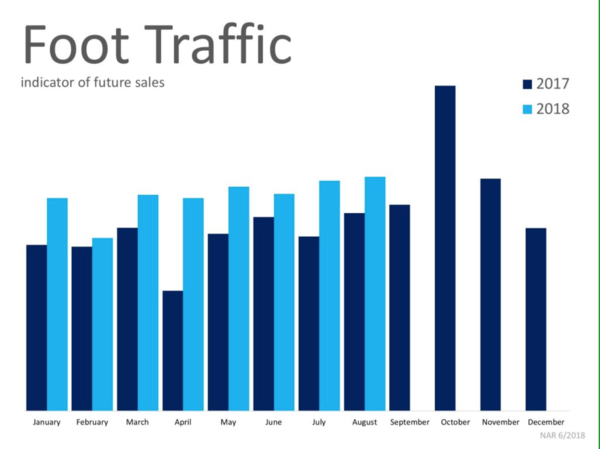

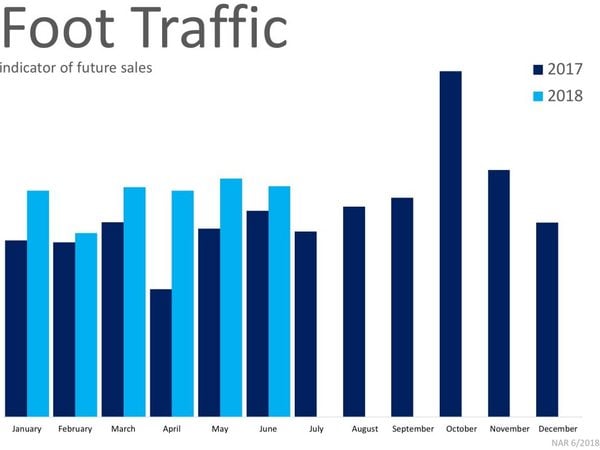

Things seem to be shifting in the housing market. For Geoff, the stats of homes sold are the “mother’s milk” of the industry. Nationally it’s been a mixed bag through 2018. September’s numbers are not yet in, but August numbers for total home sales were just about even for 2017 and 2018. It appears that things are shifting in the market, with the number of sales not increasing like last year, year over year. However, foot traffic in August was much higher in 2018 than in the same period in 2017.

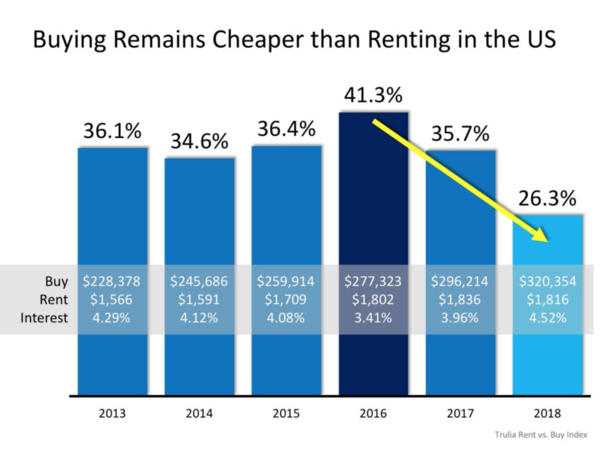

Buying versus Renting…Which is the best way to go?

Lawrence Yun, the economist of NAR, has said that we’ll probably see growth in terms of the housing market on the lower end because the job market is strong. People are working, making money and want to invest their money in real estate. However, there may be a slowdown in the higher end because interest rates are rising. How does affordability of renting compare with buying? There is a steep curve, not a good outlook for renters. Since 2013 it has been cheaper to buy instead of rent on an overall national basis. If you have the ability, it costs less to buy than to rent on an overall monthly basis.

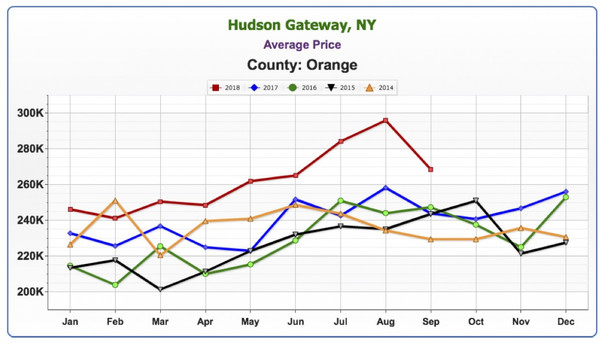

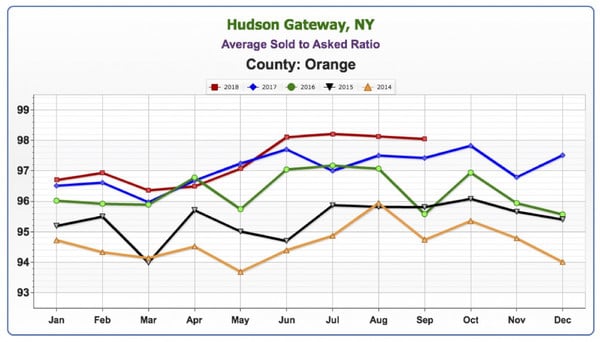

October 2018 Housing Market Update – Orange County

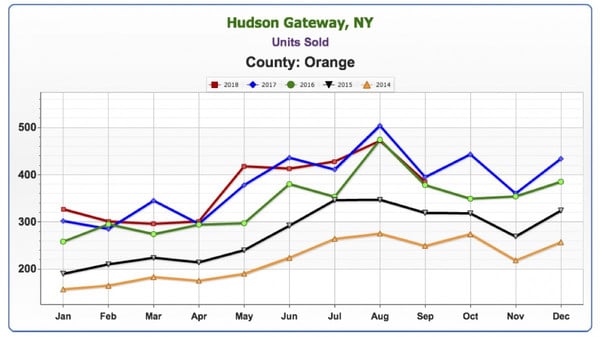

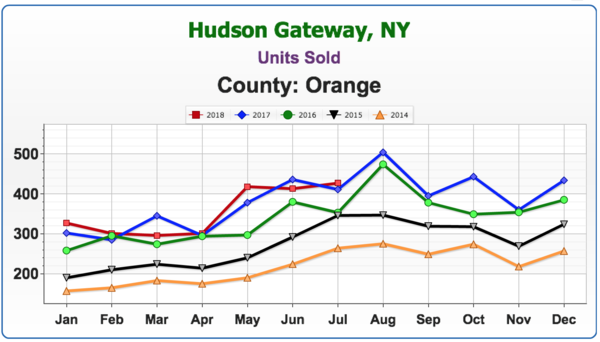

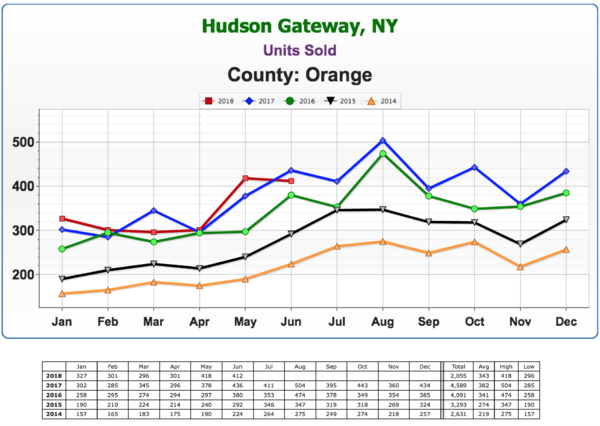

Units Sold

As stated before, Geoff sees this number as the mother’s milk of the housing market. This all-important number gives us a snapshot of how many homes are selling. The number of units sold in Orange County appears to be cooling off. He believes we’ve seen the peak of the last runoff and that it’s behind us. Geoff’s view seems to be backed up by an article that appeared last week in the Wall Street Journal, which referred to a soft downturn in the market.

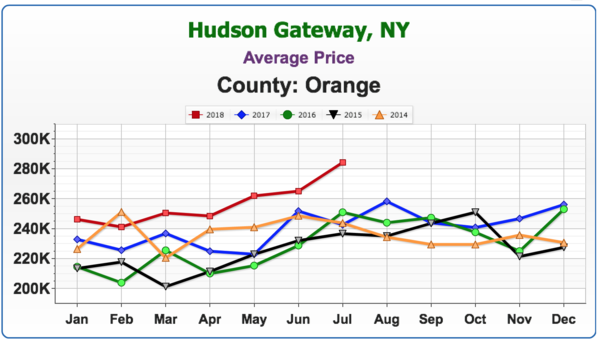

Average Price

There is a big variance in price from where we were last year. The downward trend is a seasonal fluctuation and not a cause for concern. Price always lags units sold at least 6 months or more. Price increases may occur over the next 6 to 12 months, even though the number of units sold is dropping.

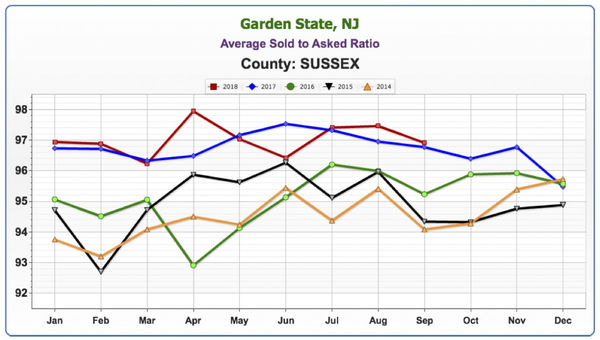

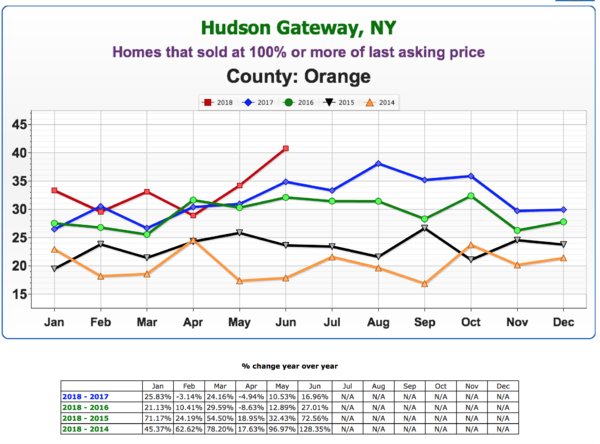

Average Sold to Asked Ratio

We are still pretty high, still over 98%, which means sellers are only having to negotiate 2% from their asking price.

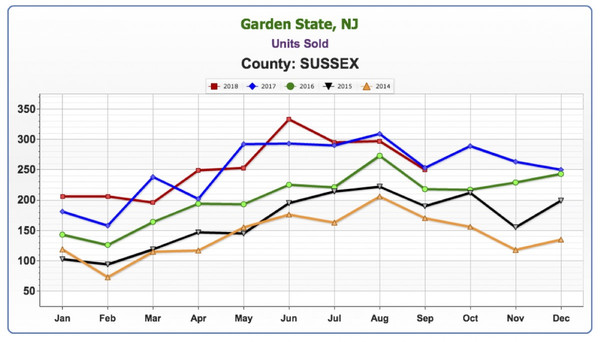

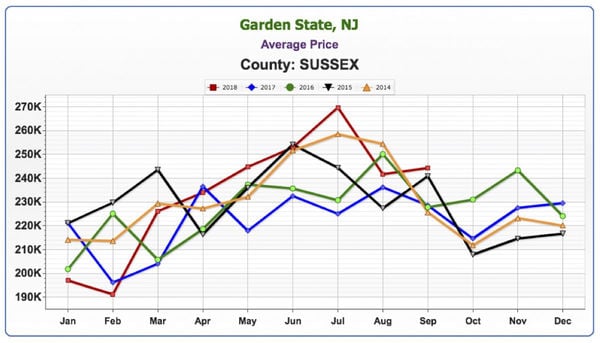

October 2018 Housing Market Update – Sussex County

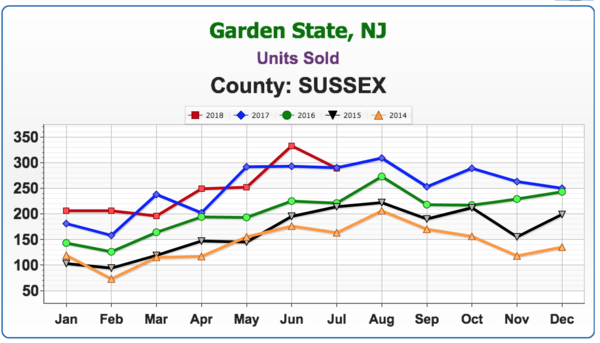

Units Sold

A similar trend to Orange County, where some months are up, some down, on a year over year basis. It’s a mixed bag, and the numbers seem to indicate a cooling off.

Average Price

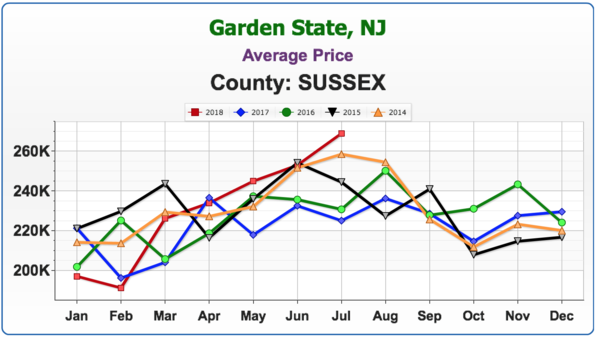

Average prices never rocketed in Sussex as they did in Orange County. In previous updates, we’ve spoken about how there is simply more foreclosure inventory and activity which has dragged down the average. However, that doesn’t mean that homes that are well maintained and well located haven’t done well.

Average Sold to Asked Ratio

Average price never rocketed here like it did in Orange County. There has been much more foreclosure inventory and activity in Sussex and that has dragged down the average home price. However, that doesn’t mean that well-located, well-maintained homes haven’t done well.

Slightly below Orange County, the numbers are still hovering around 98%.

Panel Discussion

The Sales Associates Point of View

Geoff believes the market is cooling. He asked the panelists what they were sensing in the field. Keren replied that there are fewer houses that are updated and nicely done, and buyers have higher expectations. During the summer, people were rushing to find homes in order to get situated before the start of the school year. Without that added stress, many buyers are being pickier. Alison finds that people are looking for something that is just not there. Inventory is not meeting the demand. In addition, many of her closings were delayed, affecting numbers for September.

Jacque is finding that there is a lack of finished, move-in-ready homes under the $400,000 price point in Warwick. In addition, many families with school-aged children are waiting for the spring to resume their search. Also, the seasonal fluctuation impacts the market as people are beginning their holiday preparations. Pam is also seeing the issues mentioned by the other sales associates. The inventory shortage, buyers being very picky, even homes that have been flipped that aren’t good enough. It’s difficult for people to find what they’re looking for in their dollar amount.

Geoff summed up these comments by stating it is still a very good time to sell a house. However, there is nothing to stop the housing market from slowing down. Thus he advises sellers not to put off listing their home if they are planning on selling.

Guest Panelist, Matt Zagroda, discusses the bond market…

Matt Zagroda is a Sales Manager at MBS Highway, the leading provider of real-time market data for mortgage professionals. As such, Geoff welcomed his input on the bond market. Geoff asked Matt what is happening with the bond market, as rates seem to be increasing by the minute. Matt explained that at the end of last year the Fed wanted to do quantitative tightening. Previously they had been reinvesting gains from the bond market back into the bond market, which brought their balance sheet up greatly.

Matt Zagroda is a Sales Manager at MBS Highway, the leading provider of real-time market data for mortgage professionals. As such, Geoff welcomed his input on the bond market. Geoff asked Matt what is happening with the bond market, as rates seem to be increasing by the minute. Matt explained that at the end of last year the Fed wanted to do quantitative tightening. Previously they had been reinvesting gains from the bond market back into the bond market, which brought their balance sheet up greatly.

They wanted to wind that balance sheet down and made a plan just before Janet Yellen stepped down as Fed Chair. So, October of last year they wanted to reduce it by $10 billion. January of this year, $20 billion, April $30 billion, July $40 billion and October, $50 billion. That was the last tightening session. They weren’t going to continue to reinvest it. There is no Fed buying into the bond market, which is why we’re seeing changes in interest rates. There was a drop in the bond market and a rise in rates.

Matt expects that in the upcoming months we’ll be experiencing volatility. However, this is actually a more normal bond market. If there is any economic news that would potentially hurt bonds, we’ll notice it more. Previously the Fed was buying back into it, softening the blow, creating almost a safety net. Now there is no safety net, so if it’s going to hurt – it’s going to hurt. That doesn’t mean that if there’s good news that it will be the opposite and that it will help the bond market… Again, the Fed is not juicing the good news to buy and make that increase even more so.

More volatility is expected into the future, potentially more to the downside, but it’s not expected to be a straight downward line. Rates may continue to get worse, though the hope is that they’ll remain steady. Much depends on what happens with the Fed and their plans for rate hikes.

Geoff recalled buying his first home around 2003. His 30 year fixed rate was at 6.5%. We’re hovering now at about 5% now. Matt agreed that was about right.

Looking back, it hasn’t been higher than this since 2009. Previously, it was much higher. Rates have been pretty much below 5% since then. The largest run on the housing market was 2005, 06, 07 and rates were pretty high back then. The rates may impact the mortgage industry insofar as refinancing. However, when rates eventually come down, the refinancing market should open up again.

… the stock market, and global contagion

Geoff asked Matt his thoughts on the stock market and its unbelievable run. Matt expects that eventually we can’t go much higher and things will come back to a more normal range. Not a crash, but just a more normal range that will help bonds and interest rates even a little bit. When money comes out of stocks it is generally invested in bonds, especially when there’s talk of trade wars, etc. When there is uncertainty in the market, many people invest in safer, long-term investments like bonds.

Geoff had a final question… The idea that there could be a global contagion. By and large, there is a lot of risk around the globe. Many governments are not in a good fiscal situation. Currencies are all over the place. There’s a lot of risk around the globe. The US seems like the shining city on the hill, on our own pedestal for some time. He asked Matt his thoughts on the global market. Matt replied that there is turmoil in Europe, and especially Italy right now. The world is interconnected. However, we’re not expecting great leaps and bounds right now because of that turmoil. However, it does affect us.

In closing, Geoff recommends the article he mentioned at the beginning of the update. Written by Laura Kusisto, it was published in the Wall Street Journal on October 13. “Housing Market Positioned for a Gentler Slowdown Than in 2007″ provides a good, historical outlook on the market and its future.

August Housing Market Update

The August Housing Market Update was held live on Facebook on Tuesday, August 14, at 9 a.m. If you missed the live webinar, you can view it at your convenience by clicking here.

Next month, the Housing Market Update webinar will take place on Tuesday, September 18 at 2 p.m. You can sign up for updates at GreenTeamHQ.com/HMU.

Meet the Panel

Geoff Green

Keren Gonen

Patrick Keelin

Jeff Lobb

Geoff Green moderated the webinar and presented statistics for Orange and Sussex Counties. Keren Gonen, of Green Team Real Estate New Jersey and Green Team Home Selling System, gave her perspective on the market from the sales associate’s view. Guest panelists were Patrick Keelin, Branch Manager of Family First Funding’s Warwick office, and Jeff Lobb, Founder and CEO of SparkTank Media. Green Team’s Marketing Director, Melissa Bressette, was on hand to make sure everything ran smoothly.

Housing Market Update – National

Nationally, for the last two months, the number of homes selling is down slightly from 2017. Earlier in the year it was almost even. There is a mixed bag, not a continued trend. Common knowledge says it’s all about inventory. There are just not enough homes for all the buyers out there.

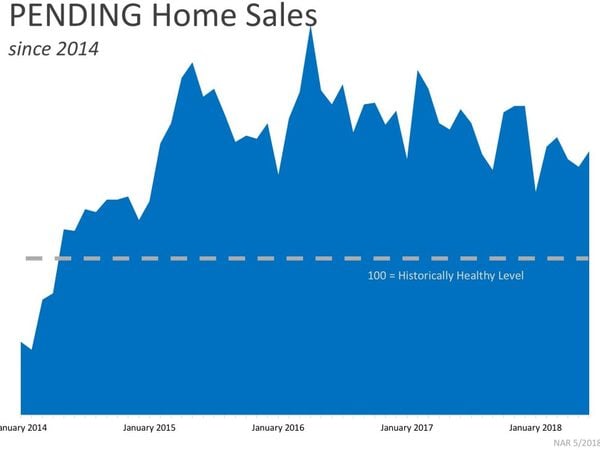

Pending home sales seem to be trending downward nationally.

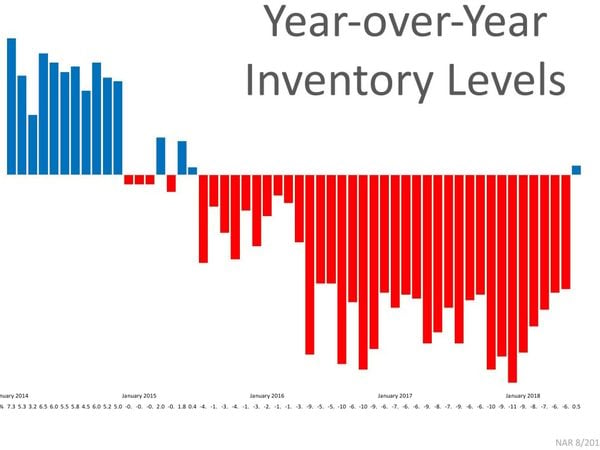

The National Association of Realtors shows year-over-year inventory levels up for the first time in 36 months. It may be a good sign, though it may also be indicative of the market slowing a little. However, foot traffic is up in 2018, compared to 2017. This graphic represents the numbers of people actually in homes, looking to buy. This number has been up consistently all year, though sales are down on a national level. From a national perspective, it’s still a very solid market.

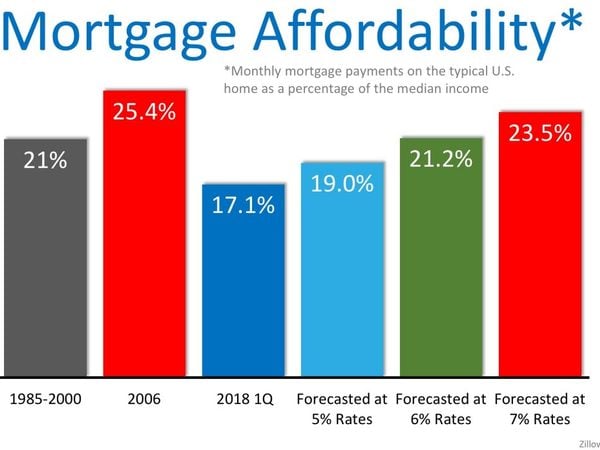

From 1985 to 2000, 21% of household income was dedicated to mortgage payments. In the first quarter of 2018 we’re well below that number. At 17.1%, we’re about 4 points below the historical average over the last 25 years. Therefore, even though prices are rising and inventory is tight, homes are still relatively affordable compared to 1985 to 2000. Even if rates do get to 6% or so, household income dedicated to mortgage payments will be only a few points higher than the 1985 to 2000 average.

Housing Market Update – Orange County, NY

Getting down to local stats, although at a slowing pace, the numbers are still at historical levels. In our area, where the current number of homes selling is the equivalent of 2006 (which was one year after the absolute peak in the market that occurred in 2005), the rate of sales is historically very high. This is a very hot market.

Average price is clearly rising in 2018. Geoff noted that in his experience units sold would increase, but average price didn’t quite get there. Then, units sold would start to decrease but price didn’t follow that trend, with a lag of about 6 months. There was almost a 2-year lag in average price that came after the downturn in the market.

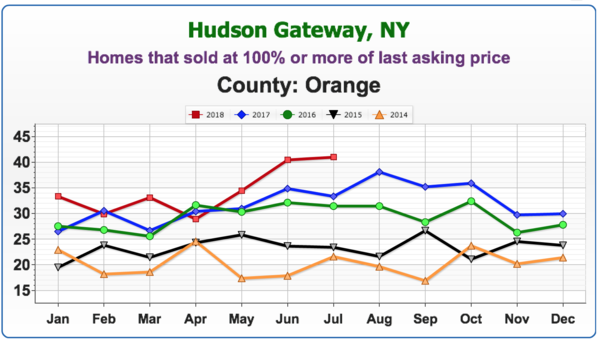

Approximately 40% of homes are selling at 100% or more of their last asking price. There are a lot of bidding wars going on, and this is indicative of how hot the current market is.

This number continues to decline, another sign that this market is hot.

Housing Market Update – Sussex County, NJ

The stats are showing a fluctuation in the number of units sold in Sussex County. It’s a mixed bag – some months below, some months above. No definitive trend has emerged.

Not quite the lift-off that’s occurring in Orange County, but after the first two months of 2018, there is a definite rise in average price and July is at the highest point of the last five years.

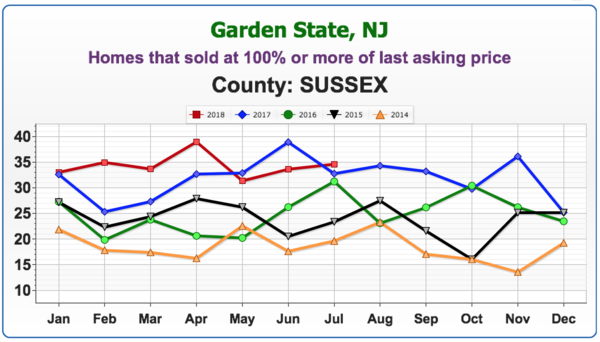

While not quite as high as Orange County, between 30 to 40% of homes are selling at 100% or more of last asking price.

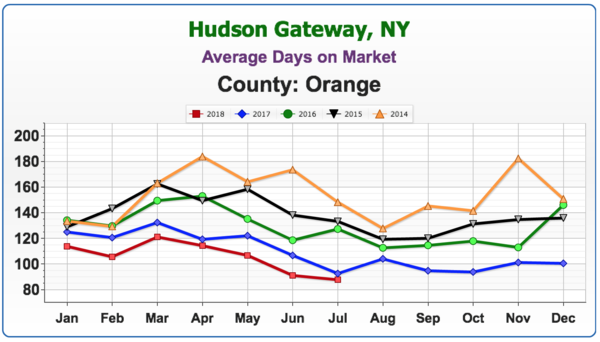

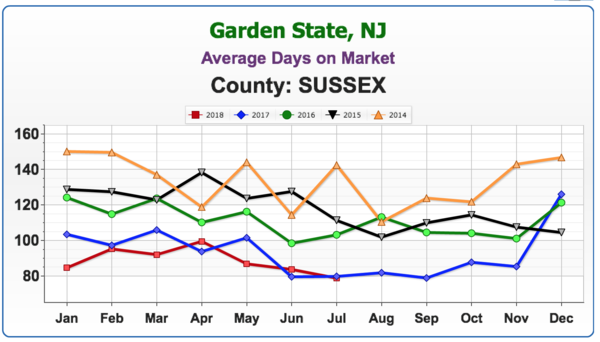

We’re seeing a similar trend to New York, with homes selling at around the 90-day mark.

Keren Goren – A Sales Associate’s Perspective on the Market

Geoff asked Keren Goren, one of Green Team’s top producers, for her thoughts on the current market. Licensed in both New York and New Jersey, Keren finds that there are many prospective buyers for both Orange and Sussex Counties. Lots of bidding wars are going on.

She does feel that some of the flippers in the area are doing less and asking for more. This appears to be a new trend. Keren recalled that flippers used to do a much better job, but many houses on the market now are unfinished and are scaring buyers away as opposed to inviting bids. Therefore, some outdated homes are actually selling for prices higher than they should or would have a few months ago.

Keren sees no sign of the market slowing down. However, she is seeing delays in closings due to issues with some mortgage companies, and with buyers making poor decisions with their finances. Keren did note that her experiences with Family First were extremely positive, and she highly recommended them.

Geoff noted that the current market upturn stands a chance at longevity. Following the downturn, as deep and as long it was, people weren’t moving. Banks have since cleaned up their balance sheets, tightened programs up, and are making money. There are fewer defaults happening. Basically, everything depends on how much money the banks are willing to lend.

PJ Keelin – A Lender’s Perspective

The mortgage industry is doing well, offering a lot more first-time homebuyer programs with as little as 3% down, USDA becoming very popular in Orange and Sussex County areas. Also trending is loosening up a bit and coming up with more portfolio loan products, personal products and using common-sense underwriting and ability to fund when looking at today’s borrowers.

With homes in the $200,000 to $300,000 price range becoming few and far between, they are looking at different programs, such as adjustable rates, less money down, and interest only type payments. However, in these cases, information and education should be given to borrowers upfront. It’s necessary to prepare the borrower for everything that will come together throughout the process. It’s extremely important for borrowers to be aware of what they are getting into with these products and understand how they work.

Geoff noted that with the last downturn, banks were not requiring people to have much “skin in the game.” Zero down, lying about income, jamming loans through. Geoff asked if PJ was seeing any of those practices coming back, or if there remains more oversight. scrutinizing income and the buyer’s comprehensive financial situation, down payments, etc. before loans are going out.

PJ replied that FANNIE and FREDDIE are doing a great job operating more with common sense with people who can have a little more risk, etc. They are requiring more skin in the game. Banks are protecting themselves and borrowers by not letting people put themselves under water.

Where are mortgage rates headed?

Geoff noted that the Fed has been raising short-term interest rates and will probably continue to do so to stifle inflation. He asked PJ where he saw mortgage rates landing over the next 12 to 18 months. PJ answered that he believes rates will be consistently in the 5’s through most programs. The market is being built into where those rates are and is slowly trending. Supply and demand are balancing each other out. Geoff feels that if you buy now, the value of your home won’t drop out like it did 12, 14 years ago. Pricing levels appear to be realistic and should hold for some time in the future. Buyers want to know if the asset they’re buying will be worth at least as much or more than they’re paying now. Even though it is a seller’s market, Geoff and PJ concurred that it is a good time to buy.

Furthermore, PJ stated that appraisers are not allowing appraisal inflation to come above where the market truly should be. It’s better for appraisers to be a little tight because that will keep the longevity of this strong market going on for 12, 18, 24 months. Geoff replied that appraisals have been challenging over the last 3 years. Prior to the upturn, prices were a mixed bag, leaving appraisers unwilling to take a chance as they couldn’t see where the market was going. However, he noted that now some appraisers are more willing to take a chance and make an allowance because of the steady upward-trending market, even though there might not be a comp that can exactly substantiate it. There are fewer appraiser issues, though there are still times when they won’t go along with the offering price. This hurts the seller but protects the buyer. And it’s another way of controlling the market.

Jeff Lobb – A Marketing Expert’s Perspective

Geoff asked Jeff for his views on the future of service providers in the real estate industry in this age of technology. Are realtors going to be the next victims of business models like Amazon? Will technology replace realtors just as retail stores (like ToysRUs) and their employees have been replaced?

Jeff’s view? While buzzwords like “disruption” do sell media, there are things happening at higher levels. However, the real estate agent is not going away anytime soon for one simple reason. There are too many moving parts to a transaction, and emotion is one of those. Technology has not reached the stage where it can handle all these parts.

Disruption occurs with more brands trying to change the way we are doing business, making it faster, more tech, or more niche. New companies are coming into play. Compass, Redfin models, Purple Bricks. And new people are coming into the space trying to change and elevate what we do. At the same time. the industry has seen some large teams leave major brands, saying they can do things better by themselves, without the big brand box.

Taking care of business…

One way to keep track of business is to every day look at local inventory. If there are 500 listings, see how many of those you got. If it’s only 2, there is a lot to be done. The business is a marathon; it’s a competitive race, but not many have enough drive to do the hard work that’s needed. To say the business is slow is not valid. Every day more homes come on the market and more get sold. Someone is getting those listings. And that is where the challenge comes in. It’s about doing the day-to-day work. All the technology that is available can make us work faster and smarter, but we still have to do the work.

Philosophically speaking…

Geoff has a broader perspective as to where realtors stand and what the future holds. As an example, despite all the tools available online there are more travel agents now than in the year 2000. It takes time to do all the research, etc., and many people are finding it more desirable to hire someone to do that work for them.

There has been an explosion of information and technology, but at the end of the day, it’s time. Do most people want to spend the amount of time it takes to properly sell their house or negotiate to buy a home? Most people prefer to hire a real estate professional to handle all the parts of the puzzle. In addition, Geoff believes the housing market is important to the overall US and global economy. The economy is revving. largely because of the housing market healing and coming back. And real estate agents are critical to the health of the economy.

Jeff added, “Will Amazon and Facebook get into the real estate marketplace? Probably!” The big picture is that some companies are coming in trying to acquire agents and market share. Others are trying to change the way technology is driven. However, you still need the people to execute the transactions and deal with the emotional process of a sale.

Geoff’s final analysis? We, humans, are complicated beings, and it takes a human to navigate this process of buying a home. And after much consideration, we should continue to invest in real estate agents and our industry because we’re needed and timeless.

Visit our website, greenteamhq.com/HMU to register for our next Webinar on Tuesday, September 18 at 2 pm. You can also view previous webinars videos and access other recaps like this.

July Housing Market Update

The July Housing Market Update was held live on Facebook on Tuesday, July 10, at 9 a.m. If you missed the live webinar, you can view it at your convenience by clicking here.

Meet the Panel

Geoff Green moderated the webinar and also presented relevant statistics in a historical context. Keren Gonen of Green Team Real Estate New Jersey conveyed the sales associate’s perspective on the housing market. Melissa Bressette, Green Team’s Marketing Director, rounded out the company’s participants. This month’s special panelists were Kevin Dolan, Branch Manager and Co-Director of Renovation and Construction Lending at Annie Mac Home Mortgage and Joe Panebianco, CEO of Annie Mac.

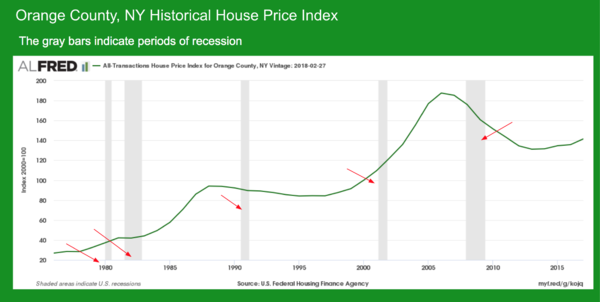

Orange County Historical House Price Index

Geoff presented a historical view of national and local prices, and a look at the market before, during and after recessions. In this chart of the Orange County, NY price index, gray bars indicate periods of recession. As shown in the graph, recessions don’t necessarily trigger downturns in the housing market. The inverse is usually true, with downturns in the housing market generally triggering recessions. Exceptions include the recession between 2000 and 2005. The housing market actually started to downturn around 2005, long before the financial collapse of 2008. Prices peaked in 2006, then continued to slide for over a decade. The steepness and duration of the curve is what is of special interest.

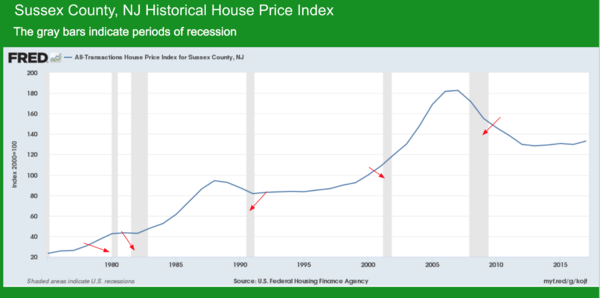

Sussex County NJ Historical House PriceIndex

In a historical context, the Sussex County and Orange County stats show a similarity, reflecting national trends.

National Stats

In Total Home Sales in thousands there are no major increases in the year over year stats.

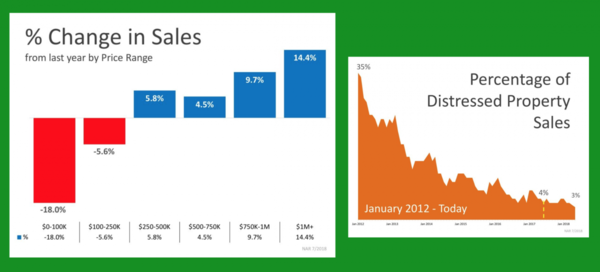

The number of houses available in lower price ranges is way down. However, there is an uptick in higher priced homes. Because of lack of inventory, buyers are being pushed into that higher price bracket.

The percentage of distressed properties for sale is way down from 2012.

Orange County Market Stats for June 2018

Units Sold

According to Geoff, this is one of the most important analytics in the housing market. No matter where pricing is, you can get an idea of the market by how many houses actually sold. There has been a great year over year increase for the past five years, but now it’s slowing down and we’re seeing a flattening now.

Homes that sold at 100% or more of last asking price

There’s a spike in this number. This is a hot market, and any home that is well located and in good condition will most likely have multiple offers at any one particular time. Basically, almost half of every listing on the market is being bid over asking. Note: Stats are based on last asking price, not original asking price.

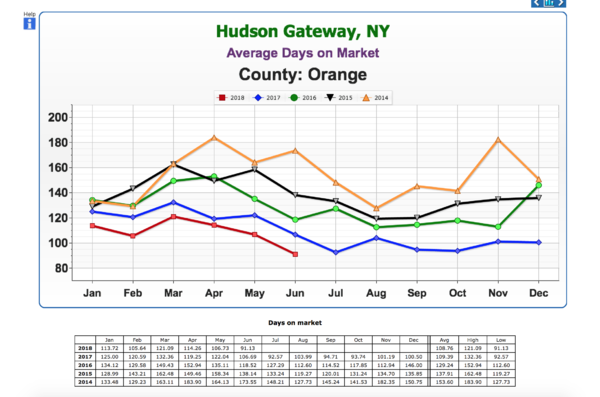

Average Days on Market

This number continues to decline, again showing a strong seller’s market.

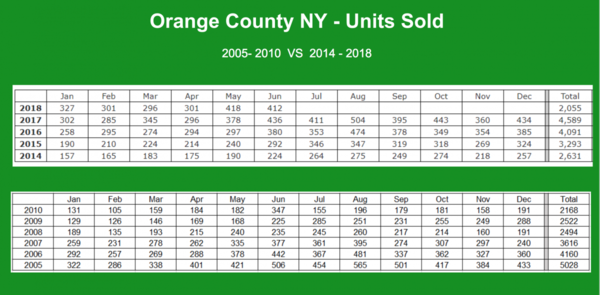

A Comparison of Units Sold from 2005-2010 versus 2014-2018

Geoff researched units sold in Orange County from 2005-2010 versus 2014-2018. Trends here follow National trends. The peak year was 2005 in terms of units sold. 2006 was the highest average home price the County has seen.. However, in 2010, the number of units sold had slid to almost half of the 2005 figure. Last year, we were above 2006 numbers, and close to 2005 in terms of units sold. Whether we’ll match or exceed that number in 2018 remains to be seen.

Recession

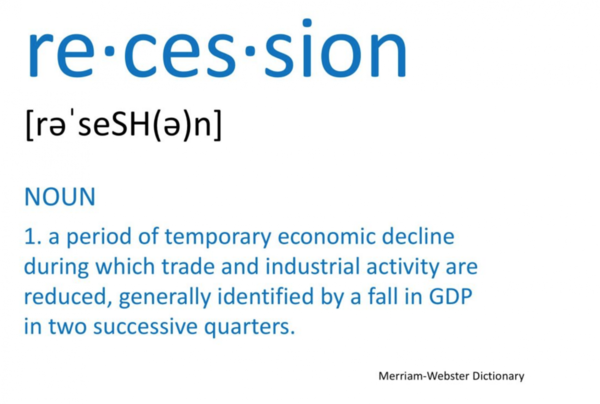

In a capitalist society, it is not a question as to whether or not there will be another recession. The question is when.

As defined in Merriam-Webster Dictionary, recession is “a period of temporary economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.” There is, of course, great interest in when the next recession will hit, and what impact it will have on the housing market.

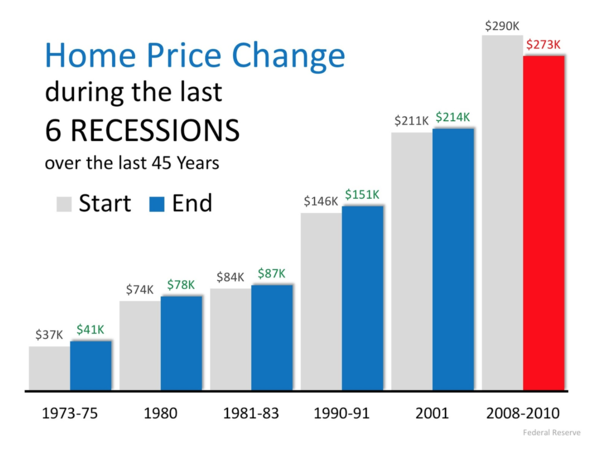

The graph shows home price changes during the last 6 recessions, over 45 years. The recession periods as designated by economists do not include the housing market downturns. Historically, prices haven’t been that affected during the recession; however, the definition of recession doesn’t include the whole downturn. And the real estate market takes time to recover.

‘

Keren Gonen’s perspective on the market from a sales associate’s point of view…

The market is very hot, in both Orange and Sussex Counties. In Warwick, if you don’t jump on a house right away, you can lose it. Keren is seeing bidding wars on homes within days of listing them.

When asked how long she thought the market would remain strong, she estimated about a year. One of the reasons we’re not seeing the lower priced homes sold, Keren indicated, was that banks that do have foreclosures are releasing them at much higher prices. Some banks are also renovating and flipping homes and charging even more.

Geoff commented that previously, when the market was really bad, there was shadow inventory. Banks would hold on to foreclosures, creating fear in the market that they would dump their inventory of low-priced homes, driving down prices. However, the banks seem to be changing their ways of doing things by renting out some homes, and fixing up others and selling them at higher prices.

The Mortgage Market – Where are we now?

Geoff stated that we’re definitely in an increasing rate environment and the Fed has signaled that they are going to continue to increase the overnight lending rates into the foreseeable future. Geoff asked Kevin Dolan to address where we are at now…

Kevin responded that where rates are concerned, they’re turning higher for the foreseeable future. Partly due to media coverage, people are starting to take the rise of interest rates and home prices seriously. They see continual coverage of higher rates on news shows. Thus, people are becoming proactive, buyers and sellers alike, driving productivity level.

Interest rates, inventory and recession. Oh my!

Joe Panebianco does economic analysis and strategy for Annie Mac. His expertise made him the perfect person to discuss specifics and timings of interest rates, inventory and recession.

Interest Rates: We will most likely be range bound from a 10-year treasury perspective from approximately 2.75 to 3.05 yield in the ten year. In other words, we’ll be relatively stable. Should this estimate be incorrect, Joe believes a slightly higher rise in interest rates will not significantly hurt the housing market. At some point, rates rising will have a deleterious effect and purchasers’ ability to afford a home may be impacted. However, we’re not at that point now.

Inflation and economic growth are the two primary components of interest rates. Inflation has remained stubbornly low and will most likely remain so. Hence, one reason why rates should remain relatively low. People talk about the Fed increasing rates, but they are increasing the short end of the curve.

As the Fed continues to hike rates, the result will be 10 and 30-year rates looking more like 2 and 5 year rates. Most of the duration of a mortgage-backed security is in a 7, 10 and 30-year part of the curve. And Joe believes that the more the Fed increases rates, the more likely we are to be in a recession and more likely to have lower, longer-term rates remain where they are or go lower. The mortgage market on Adjustable Rate Mortgages could be hurt because they’re much more likely to rise as they’re sensitive to the shorter end of the curve. 30-year fixed mortgages are more likely to stay in the aforementioned range.

The Global Connection

We live in a globally connected network and there is a yield spread between US 10-year Treasury bond and bonds in other countries, like Germany, Japan, Australia.. For central banks, very large institutions,etc., putting their money in US Treasuries provides a safer, purer investment over countries with significantly lower yields. However, regarding tariffs, trade wars are inherently bad for economies and may throw a curve ball into any predictions.

There are some who refer to our current economy as a “Goldilocks economy.” Not too hot, not too cold, just right… in some ways. The economy is growing enough to create jobs. And, according to Joe, jobs are far more important to home purchases than interest rates are. In the early 1980’s, interest rates were at 15% and yet homes were flying off the market. When rates go up, prices tend to come down. And there is always a buyer, especially if there is value to be had.

The history is if the Fed goes too far, it will drive the country into recession. Joe believes we have approximately 12 to 18 months left in this cycle. And that at the end of this period, we’ll be in a more normal market with a healthier balance between demand and sup

Factors that impact inventory

Labor, or lack thereof, is a major component. Many significant builders have unused land on their balance sheets, on hold because of the great recession of 2007 to 2010. About 70 to 75% capacity of the productive capacity of the home building industry was lost. Brick layers, sheet rockers, carpenters, plumbers, electricians, etc. – left the industry to seek employment in other fields. In addition, when major storms hit Texas, Florida, etc., many people in the industry picked up and went to work in those cities where they could make much more money. There are simply not enough craftsmen and laborer to build all the homes necessary to meet current need.

Municipal Fees, laws – Fees, regulations, etc., have made building a home both difficult and expensive. To help increase taxable base, some municipalities are now trying to make things a little easier for those seeking to build new construction.

Tariffs – The “War of Words” regarding trade with Canada is not good news for the housing industry. A disproportionate share of home building lumber comes from Canada, and price of lumber futures has already risen on expectation of tariffs.

Easing of Credit

In the next 12 months, we may see easing of some requirements. At this time, no one knows how this will be done. However, some options might include reducing Mortgage Insurance on the FHA side, especially for first-time buyers. Also, Freddie Mac might follow Fannie Mae’s lead in reducing Long Term Debt and Debt to Income Ratio. Average renters spends 50-55% on rent. However, the current Debt To Income ratio is in the low 40’s for purchases. There might be a move to update the DTI.

Demand is not going to Cease

According to Joe, by 2025 there will be approximately 10 million new household formations. 35% will be from millenials, 35-40% from among the Hispanic community (with some overlap between the two), and 10% from the African-American community. Many of these new home buyers will be DTI (Debt to Income Ratio) challenged. They will need the services of qualified real estate agents, knowledgeable mortgage specialists/

Geoff pointed out that purchase and rental markets are both hot at the same time. This indicates a true housing shortage. The Millennial population seems to be exceeding Baby Boomers. Pent up demand and limited supply serve to elongate and stretch out the cycle.

Home ownership improves communities – and the economy

Home ownership lends itself to not only building communities, but also to building up business, including home improvement and furniture stores, furniture stores, durable goods vendors, etc., etc.- all of which will help the economy. Inventory may become less of an issue month by month by month.

Renovation Loans

Kevin Dolan is an expert in renovation loans. There are homes on the market that just won’t sell because they are not in good shape. He believes the renovation lending program is under-utilized simply because it is not understood and there are many misconceptions.

There are two types of renovation loan programs – conventional and FHA. This opens up versatility for buyers as to who it can serve, such as a down payment as low as 3-1/2%. It also allows for lower credit scores. These loans can be utilized for primary homes, second homes and investment properties. The loan allows for someone to buy a house in need of repair, and have an approved, qualified contractor bid on work to be done. Depending on scope of work, sometimes a HUD consultant will make sure prices quoted for the work are appropriate. The renovation funds goes into an escrow account, and contractor has specified time to do improvements, usually within six months. The bank pays contractor directly. The process is streamlined and efficient.

Kevin feels that educating buyers and real estate agents alike is key to opening up this market. Keren agreed, stating that she often does sell homes by telling buyers that renovation loans are available, and explaining how they work. It opens up options and vision for the buyers who cannot afford to buy a home in the $300-$400,000 range. Annie Mac does have a certification program available for real estate agents who would like to become expert in this area.

Renovation loans – not just for buyers

Kevin commented that renovation loans can also be helpful for sellers who need to update their homes in order to sell. By adding another bath or more bedrooms, the value of the home can be increased so that the seller can pay off existing mortgage and closing costs, and hopefully make a profit as well. Also, from Seller’s position, if they have a failed septic tank, they can sell the home at a lower price and buyer can get a renovation loan to cover the cost of having the work done themselves.

Joe added that in looking to build wealth in addition to creating a home for their family, renovations can help improve their property, and therefore their investment.

Geoff spoke about the importance of finding someone who truly understands these loans as they can be tricky for the loan originator. Geoff spoke highly of Annie Mac, not just for renovation loans, but for all financing needs.

Stay tuned for the next market update

The next update is August 14, 2018 at 9 a.m. You can sign up at GreenTeamHQ.com/HMU