Green Team New York Realty is pleased to announce that Tammy Scotto has just received her Commercial and Investment Real Estate Certification. The CIREC covers a variety of topics that are important to handling Commercial and Investment transactions.

About Tammy

Tammy was born and raised in the Town of Warwick. She brings 20 years of Real Estate experience as both a Buyers agent as well as a Selling Agent. Tammy also brings with her extensive knowledge of the local market. She joined the Green Team in 2014 and there’s been no stopping her. In 2017 Tammy was in the Green Team’s Captain’s Club, selling between $3-5 million in Real Estate. In addition, she was chosen by Geoffrey Green for that year’s Momentum Builder Award, for creating positive and consistent momentum in both her professional and personal life. This past year, Tammy soared to the newly formed “President’s Club,” after selling between $5-10 Million in 2018.

Tammy has a vast knowledge of the Real Estate Market. She has skills in negotiating and closing deals. And now she is excited to venture into another area of Real Estate.

Headlines spotlight the fact that buying a home is less affordable today than it was at any other time in more than a decade. Those headlines are accurate.

Understandably, buying a home is more expensive now than immediately following one of the worst housing crashes in American history. Over the past decade, the market was flooded with distressed properties (foreclosures and short sales) selling at 10-50% discounts. There were so many that this lowered the prices of non-distressed homes in the same neighborhoods. As a result, mortgage rates were kept low to help the economy.

Prices have since recovered. Mortgage rates have increased as the economy has gained strength. This has impacted housing affordability. However, it’s necessary to give historical context to the subject of affordability.

Two weeks ago, CoreLogicreported on what they call the “typical mortgage payment”. As they explain:

“One way to measure the impact of inflation, mortgage rates and home prices on affordability over time is to use what we call the ‘typical mortgage payment.’ It’s a mortgage-rate-adjusted monthly payment based on each month’s U.S. median home sale price. It is calculated using Freddie Mac’s average rate on a 30-year fixed-rate mortgage with a 20 percent down payment…

The typical mortgage payment is a good proxy for affordability because it shows the monthly amount that a borrower would have to qualify for to get a mortgage to buy the median-priced U.S. home…

When adjusted for inflation, the typical mortgage payment puts homebuyers’ current costs in the proper historical context.”

Here is a graph showing the results of CoreLogic’s research:

As the graph indicates, the most recent calculation remained 28% below the all-time peak of $1,275 in June 2006. That’s because the average mortgage rate at that time was 6.68%. As seen in the graph, both today’s typical payment and CoreLogic’s projection for the end of the year are less than it was in January 2000.

Bottom Line

Even though home prices are appreciating at a slower rate, home affordability will likely continue to slide. However, this does not mean that buying a house is an unattainable goal in most markets. It is still less expensive today than it was prior to the housing bubble and crash.

Get local housing market updates – sign up to receive the Green Team’s Housing Market Update Report.

Green Team New Jersey Realty is the #1 real estate office in Vernon* and they couldn’t be prouder.

Some of Green Team New Jersey Realty Partners share their thoughts

According to Equity Partner Charles Nagy, “2018 was an exciting year for Green Team New Jersey Realty on a number of fronts. First and foremost, it was a year of great accomplishments for the team. Not only did we bring on some new and experienced talent, but we also bought our own office building. And, as a result of the team effort, we ended the year as the #1 real estate office in sales volume and transactions in all of Vernon, NJ after only our second year in business. It is exciting to see what we accomplished as a team for the entire year.”

Kim Lasalandra, Managing Broker, described how she felt. “I’m ecstatic! To be the #1 office in terms of sales volume within two years of opening our doors is truly remarkable. And it’s a tribute to the incredible work ethic and determination of our sales associates.”

Geoffrey Green, the founder of Green Team New York Realty and a partner in Green Team New Jersey Realty, shared his thoughts. “I’m very proud of everyone at Green Team New Jersey Realty for taking Green Team Realty’s model, bringing it to Vernon, growing it, and achieving #1 status. I just can’t wait to see what 2019 brings!”

Green Team Realty’s dedicated approach…

Green Team Realty’s dedicated approach has proven that the results are impressive when you provide productive, dedicated agents with continual training and support, a culture that values clients through excellent service and an appreciation program, and an array of competitive advantages. Furthermore, Green Team Realty’s commitment to local community and charities is another aspect that attracts like-minded real estate professionals.

Green Team New Jersey Realty’s new office is located at 293 Route 94, Vernon, NJ. To learn more, visit GreenTeamHQ.com or call 973-814-7344.

*As compared to all GSMLS Offices located in Vernon Township by closed sales volume for the time period of 1/1/18-12/31/18.

The Green Team’s January 2019 Housing Market Update was held on Facebook Live Tuesday, January 15 at 2 p.m. If were unable to view the webinar live, you can watch it at your convenience here. You can also sign up for future updates at GreenTeamHQ.com/hmu.

This month’s panelists…

Geoffrey Green, President/Broker of Green Team Realty, moderates the monthly webinars. He also presents national statistics, together with local updates for Orange County, NY and Sussex County, NJ. This month he is joined by Carol Buchanan of Green Team New York Realty, Keren Gonen of Green Team New Jersey Realty and Patrick “PJ” Keelin of Family First Funding.

The National Outlook

The above charts are raw numbers – the number of homes that were sold from 2014-2018. It appears that things are softening a bit, but it doesn’t appear that it will be drastic.

The analytic showing inventory levels is important. It has been difficult to find homes for buyers over the last few years. However, it appears that inventory levels may be coming back a bit. Lower demand should yield more inventory, but hopefully what some inventory may do is bring some people back into the game who may have been been frustrated previously.

This survey of experts, market analysts, etc. addressed the question, “What Will Home Prices Do in 2019?” 100 people were surveyed and 94% projected that housing prices on a national basis will continue to appreciate. Geoff aligns himself with that 94%. He believes that in 2019 prices will come up again in spite of the fact that activity went down. Price always lags activity.

According to Geoff, this quote from Goldman Sachs is a good one. “Despite the headwinds facing the housing market going into 2019, we expect U.S. house prices to generally achieve a soft landing. We expect national average price appreciation to remain positive.” If this comes true, it’s music to Geoff’s ears. He lived and worked through the last downturn, where 50% of the number of homes that sold went away within a 2-year period of time once the market starting declining. It was a difficult time

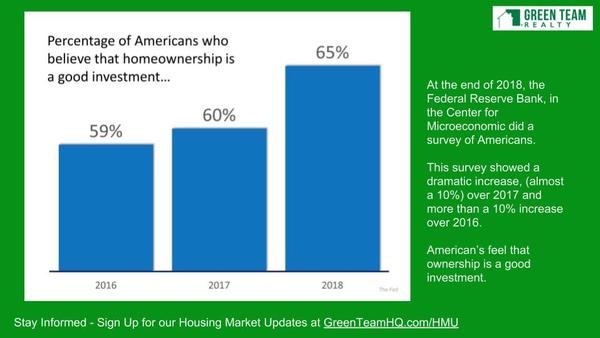

The percentage of Americans who believe homeownership is a good investment continues to increase. The market is at a peak and confidence continues to increase. However, Geoff finds that people tend to buy high and sell low. They should be buying low and selling high. The bottom of the market, 2011, 2012, and 2013 would have been a good time for investment.

However, people are confident that it’s a good time to buy now. And one thing that will never change is that homeownership is a good thing.

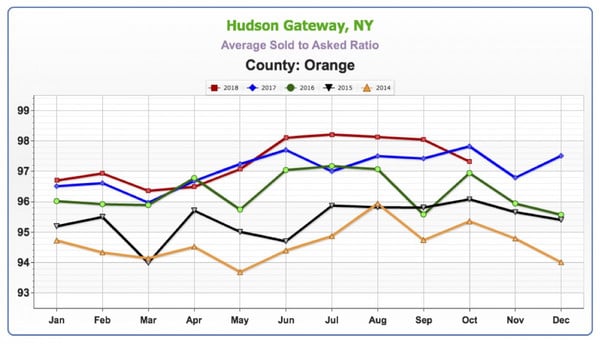

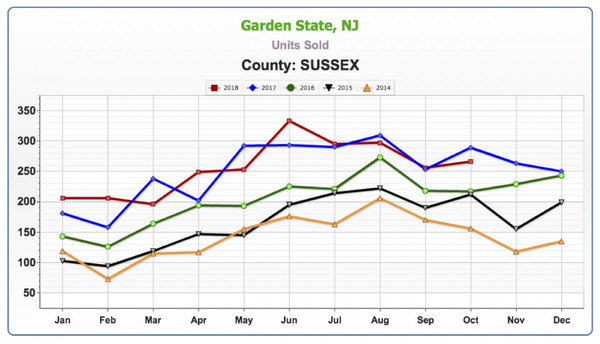

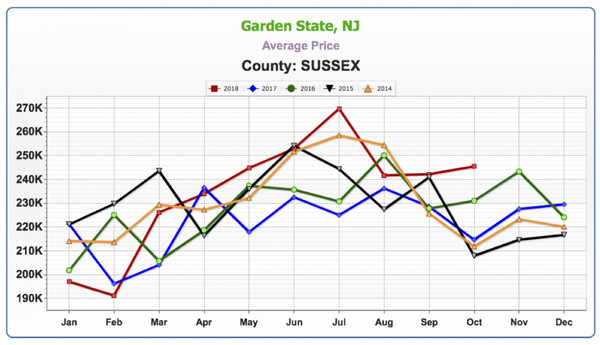

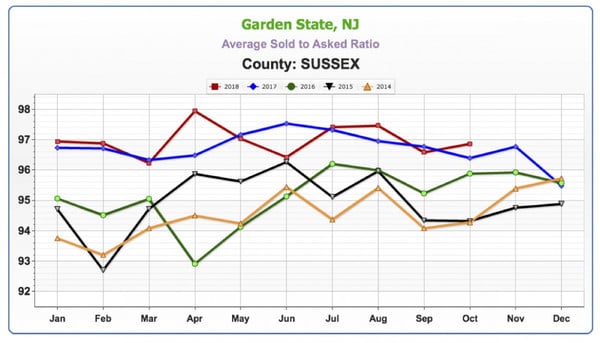

January 2019 Local Housing Market Update for Orange and Sussex Counties

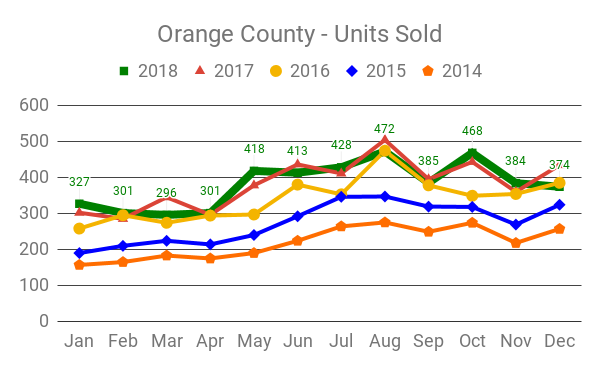

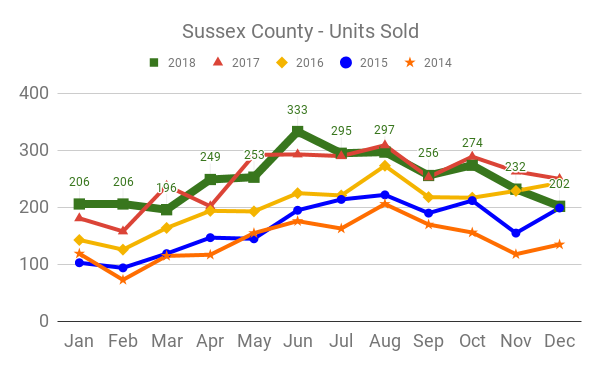

Units Sold

Five year look back. The thick green line is 2018 and while it’s been a mixed bag throughout the year, we ended up just a tad bit lower than the past two years.

In Sussex County, Units Sold was also a mixed bag, with one of the lowest totals in almost 4 years.

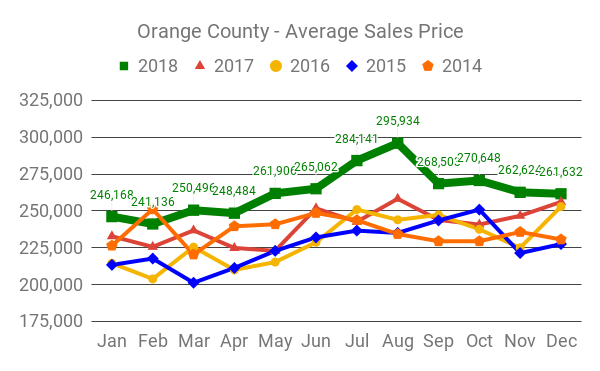

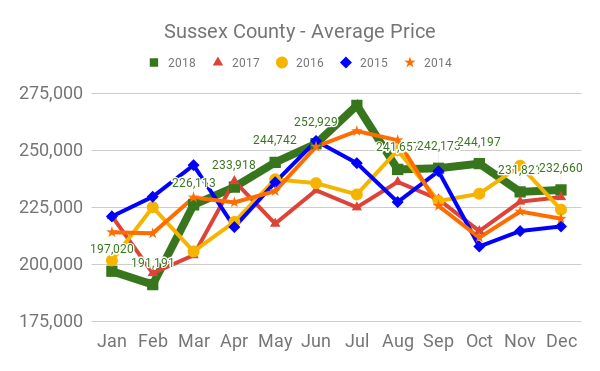

Average Price

In Orange County, prices were up substantially for a good part of the year. However, there was a cooling-off period towards the end of the year.

Sussex County never saw as much of an appreciation as Orange County did. However, 2018 was still a leading year over the past 5 years.

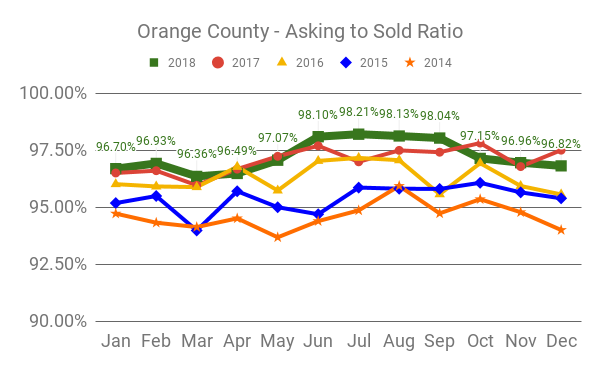

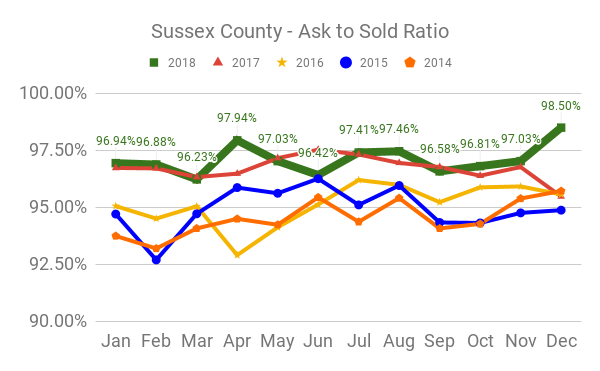

Asking to Sold Ratio

What price do homes on average sell for versus the last asking price? The higher towards 100% the hotter the market. The numbers have been strong for Orange County throughout the year.

Sussex County was strong in this category throughout the year. However, it hit its highest point in December 2018 with a ratio of 98.50%.

Panel Discussion

Geoff asked Carol Buchanan and Keren Gonen what they think of the market, as it appears a softening is underway. Carol stated that inventory is still low, and January and February are common months for the market to slow down. Carol does believe that 2019 is going to be a very good year. People seem undaunted by higher interest rates. Still a lot of buyers; just not enough homes.

Keren also agrees that 2019 will be a very good year. She thinks that people will start listing homes for sale within the next few months. Right now buyers are looking but there is still not enough inventory. She feels there are sellers sitting on the fence, not sure what to do and just holding out for a few more weeks or months. Geoff commented that the bread and butter of the season is March through August. So it’s natural for many homeowners to wait until March to list their homes.

Talking with Keren regarding foreclosure activity, Geoff asked if she see a decline? Banks are fixing up houses and putting them up at market prices. If the quality of work was good, that would be fine. However banks are bidding jobs out and the resulting work is not necessarily good work. Buyers expect to see good quality and are disappointed with what they’re finding. They often would prefer to pay more for a house that is in good shape. Therefore, many of these homes being sold by the banks are just sitting on the market. Banks are now competing with flippers who, generally speaking, do a better job at fixing up homes than the contractors. Buyers most often prefer paying full price for a home that was “flipped” well than on an REO that was not done well.

Geoff mentioned that this was not the trend in the past. Banks would not fix up their properties and try to sell them for more money. They’d just try to unload them at lower prices and buyers could get a good deal. Over the course of time we’ll see if banks decide to go back to the way they used to handle foreclosures.

Regarding the financing environment, Geoff asked Patrick “PJ” Keelin what we’re looking at for 2019. As Geoff put it, at the end of the day we’re really in the land of the banks, dependent on what they’re willing to do. And how many times the Federal government is willing to let banks leverage their money. PJ indicated that on a global scale, at the end of the year there was talk of the Feds raising the interest rate. That usually indicates a stronger economy; stronger aspects coming from the financing angle and mortgage-backed securities, etc. Unfortunately, at the end of the year there was a huge difference and the Dow dropped significantly. The drop in the Dow affected reports of things they were coming out with. So trends and thoughts of increased interest rates by the end of the year through that New Year boom fizzled out. There are reports that there is potentially going to be a decrease in interest rate for the year 2019. PJ believes that is something being put out there for a little bit of hope.

However, the biggest thing we’re competing with is the lack of inventory and what people will be able to purchase. Looking at an average household income of $60,000 to $70,000, that probably puts a person on average of what they can afford in terms of a property at $1,500 to $1,600 range. That gives them a certain price point that they have to stay in, and with increases in interest rates that is going to affect their eligibility to be able to purchase properties within a certain price range.

Geoff stated that all signs point to Fed raising interest rates. He asked PJ if he thinks that won’t be the case in 2019. PJ replied that there will be a lot less than they were expecting in 2018. They may skip the first interest rate rise. Hopes on the industry side are that there will be a potential interest rate drop. That may push that boom for people who are still sitting on the edge. He sees a stronger trend with the amount of people who are actually motivated in purchasing. They may finally be believing the reports that interest rates are not going to stay historically low and will go up. So many reports are going in different directions that it’s unsure what to make of it. Industry leaders are saying the market is staying relatively steady, but be prepared. There could be a drastic change.

Right the now trend is slow and steady. PJ commented that Geoff is proactive in all that he does; communicating with his sales associates and with the lenders they work with. Because ultimately these transactions need to happen quickly in order for them happen. When they remain open, bigger changes are coming.

Geoff wrapped up, saying that at the end of the day, interest rates are impacted by bond markets. As long as there is no major economic collapse, the housing market should be fine. He predicts a good 2019. PJ agrees, that it will be a good, strong year. People are getting more motivated.

Join us for the next Market Update

The next Housing Market Update will be held on Tuesday, February 12 at 2 p.m., when the Green Team will again be going live on Facebook. Sign up for updates at Greenteamhq.com/hmu.

Agents and staff of Green Team Realty gathered together on January 18 at the Warwick Country Club to celebrate a year that was momentous in many ways. Geoff Green welcomed everyone and outlined some of the year’s milestones.

Among them, a new home for Green Team New Jersey Realty and a beautiful renovation of the Warwick Office. Add to that the many new sales associates that have joined Green Team New York Realty and Green Team New Jersey Realty.

Growth was an important topic. Through dedication, hard work, support, creative marketing and consistent training programs, many Green Team sales associates saw their businesses grow. And both offices saw sales volume increase. In fact, Green Team New Jersey Realty became #1 in Vernon (based on a comparison to all GSMLS offices in the township by closed sales volume for the period of 1/1/18-12/31/18). This achievement is made even more impressive considering GTNJR first opened its doors in 2016.

Award Presentations

Geoff Green believes in acknowledging and rewarding both growth and achievement. And what makes the award presentations so special is the support and pride that the whole Green Team family shows to the recipients.

Yearly Sales Leaders & 4th Quarter Sales Leaders

For the third year in a row, Jennifer DiCostanzo has earned the Yearly Sales Leader Award. And she also received the 4th Quarter Sales Leader Award for 2018. (photo left)

In the New Jersey office, the team of Charles Nagy and Ted VanLaar also received both the Yearly Sales Leader and 4th Quarter Sales Leaders awards. Charles ad Ted were also the 2nd Quarter Sales Leaders in 2018. (photo right)

President’s Club

As several sales associates achieved between $5 and $10 Million in Sales Volume, a new award category became necessary. Meet the charter members of the President’s Club.

Each year Geoff selects a sales associate who has demonstrated hard work and determination while overcoming obstacles. Someone who has come through a tough spot in life and turned challenges into great success; not just in real estate but in life. A person who shows no signs of going backward. Because it’s all about building momentum towards a brighter future. This year’s Momentum Builder is Joyce Rogers of Green Team New Jersey Realty. She is a single mom with an amazing work ethic. Her hard work earned her a place in the President’s Club. It also enabled her to achieve her goal of buying a house, exactly where she wanted to. She’s no longer in commuting distance from the office. However, that isn’t stopping Joyce from being part of the Green Team family. She’s now in a long distance “relationship” with the office. Something made possible by Geoff’s advancement of a tech-based office that allows people the freedom to work from wherever they choose.

The People’s Choice Awards

The winners of these awards are selected by their peers.

Citizen of the Year

Recipients of this award are nominated by their co-workers. Both have made outstanding contributions to our local communities. This is the third year in a row that Jen DiCostanzo has been named Citizen of the year by the Warwick Office. Jen originated Light up the Holidays for the Green Team, to raise funds for local charities. The program has evolved into Team Up for Hope. This is an initiative to raise funds and awareness of the local affiliates of NAMI (National Alliance on Mental Illness) and bring attention to mental illness in our communities. She is also the organizer of the holiday gift baskets for a family sponsored by the Green Team through the local food bank. And Keren Gonen has been named Citizen of the Year by her peers in Vernon for the second year. Keren has been instrumental in raising funds for the local charities. She is also extremely active in the Team up for Hope program. These women truly believe in giving back to the community and put in the time, effort and commitment to make things happen

Team Player Award

Recipients of this award were deemed the most reliable, positive and dependable. Furthermore, they work well with others and have great problem solving skills. It’s no coincidence that the award went to the Agent Service Managers of each office. Donna Roberts was voted Team Player by her peers in Warwick. And Lora Chandra received this recognition from her co-workers in Vernon.

And a special thank you goes to…

The 2018 Awards Ceremony was sponsored by Amy Green, Vice President of Mortgage Lending, Joe Moschella, Regional Manager, and Mark Slepian, Home Renovation specialist, all from Guaranteed Rate.

In addition, we had another special treat… The Kim Lesley Band had us dancing the night away. The genuine affection that members of the Green Team share is part of what makes Green Team Realty so special. Most importantly, people support and help each other and celebrate each other’s successes. And this wonderful event was the perfect way to launch into 2019!

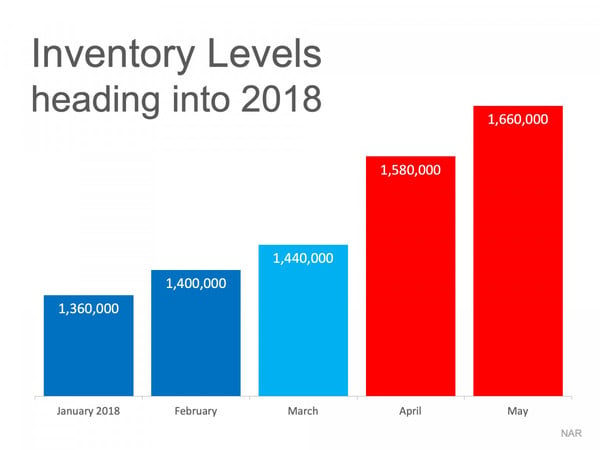

The price of any item (including residential real estate) is determined by the theory of ‘supply and demand.’ If many people are looking to buy an item and the supply of that item is limited, the price of that item increases.

The supply of homes for sale dramatically increases every spring, according to the National Association of Realtors (NAR). As an example, here is what happened to housing inventory at the beginning of 2018:

Putting your home on the market now, rather than waiting for increased competition in the spring, might make a lot of sense.

Bottom Line

Buyers in the market during the winter are truly motivated purchasers and they want to buy now. With limited inventory currently available in most markets, sellers are in a great position to negotiate.

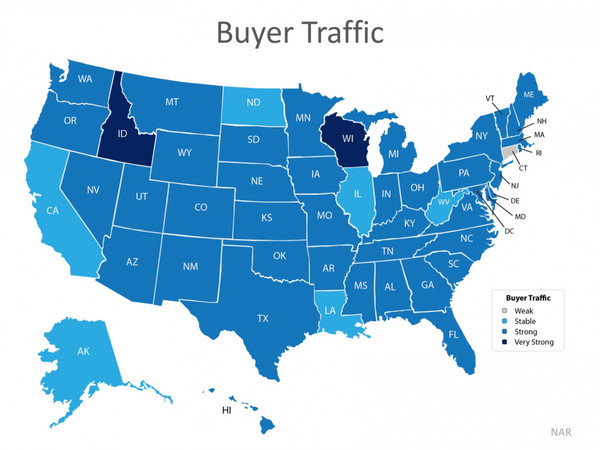

How Does the Supply of Homes for Sale Impact Buyer Demand?

The price of any item is determined by the supply of that item, as well as the market’s demand for it. The National Association of REALTORS (NAR) surveys “over 50,000 real estate practitioners about their expectations for home sales, prices and market conditions” for their monthly REALTORS Confidence Index.

Their latest edition sheds some light on the relationship between seller traffic (supply) and buyer traffic (demand).

Buyer Demand

The map below was created after asking the question: “How would you rate buyer traffic in your area?”

The darker the blue, the stronger the demand for homes is in that area. The survey showed that in 38 out of 50 states buyer demand was slightly lower than this time last year but remains strong. Only six states had a ‘stable’ demand level.

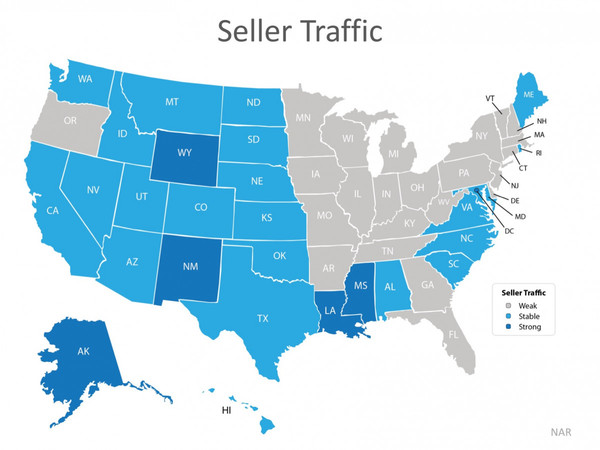

Seller Supply

The index also asked: “How would you rate seller traffic in your area?”

As you can see from the map below, 23 states reported ‘weak’ seller traffic, 22 states and Washington D.C. reported ‘stable’ seller traffic, and 5 states reported ‘strong’ seller traffic. This means there are far fewer homes on the market than what is needed to satisfy the buyers who are out looking for homes.

Bottom Line

Looking at the maps above, it is not hard to see why prices are appreciating in many areas of the country. Until the supply of homes for sale starts to meet buyer demand, prices will continue to increase. If you are debating listing your home for sale, let’s get together so I can help you capitalize on the demand in the market now!

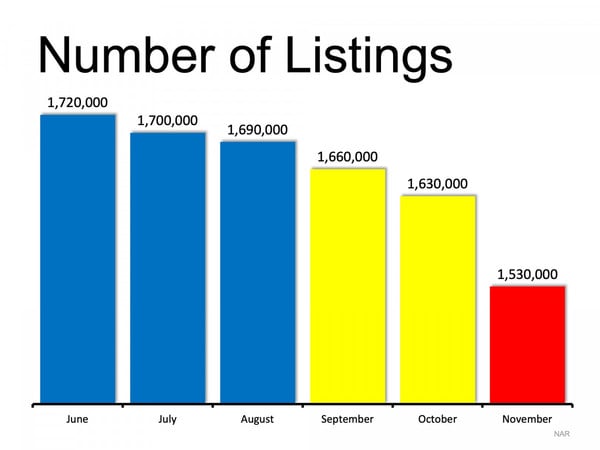

You may have heard that the housing market is softening. There is no doubt that buyer traffic has decreased. There are fewer purchasers in the market than there were last month and at this time last year. What you may not have heard, however, is that there is still a severe shortage of listing inventory in many regions of the country.

In a recent interview discussing the housing market, First American’s Chief Economist Mark Fleming put it simply:

“The biggest challenge is really the availability of supply.”

When we look at available inventory numbers released by the National Association of Realtors (NAR), we see that the actual number of homes for sale has decreased in each of the last five months.

What does this mean to you as a seller?

The best time to sell is when there is less competition. That guarantees you a better price and fewer hassles in the transaction.

Bottom Line

If you are thinking of selling your house this year, the best time to put it on the market might be right now. Let’s get together to evaluate the demand for your house in our market!

Start by finding out what your home is worth, use our quick and free Home Evaluation tool.

The Green Team’s December 2018 Housing Market Update was held on Facebook Live Tuesday, December 11 at 2 p.m. If you were unable to view the webinar live, you can watch it at your convenience here. You can also sign up for future updates at GreenTeamHQ.com/hmu.

This month’s panelists…

Geoffrey Green is the President/Broker of Green Team Home Selling System. In addition to moderating the monthly webinars, Geoff also presents national statistics as well as local updates for Orange County, NY and Sussex County, NJ. This month he is joined by regular panelist Keren Goren, and by Joyce Rogers, both from Green Team New Jersey Realty.

The National Outlook

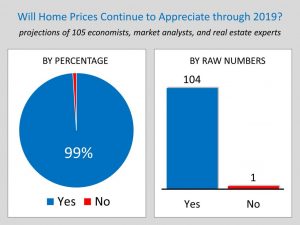

Will home prices continue to appreciate through 2019?

Overall sentiment is that the housing market seems to be cooling off, so now we’re at the prediction stage, trying to foresee what will happen next. Per the graphic, 99% of the 105 economists, market analysts and real estate experts consulted felt that home prices will continue to appreciate through 2019. However, that does not mean that the market won’t continue to slow; it means that the rate of appreciation will continue on a positive note. Most agree that it will continue to appreciate at a lesser value in the coming year.

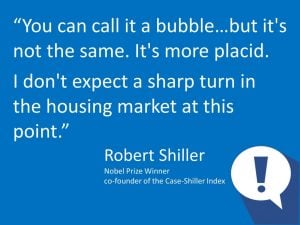

Will there be a sharp turn in the housing market?

Geoff Green finds this quote to be of great importance. Nobel Price Winner Robert Shiller is one of the thought leaders of real estate analytics. Compared to where we were in 2008, where almost 50% of transactions just went away within a two year period of time, and where we are now, Shiller doesn’t expect a sharp turn. This point of view coincides with Geoff’s observation’s over the last several months.

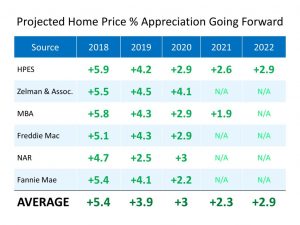

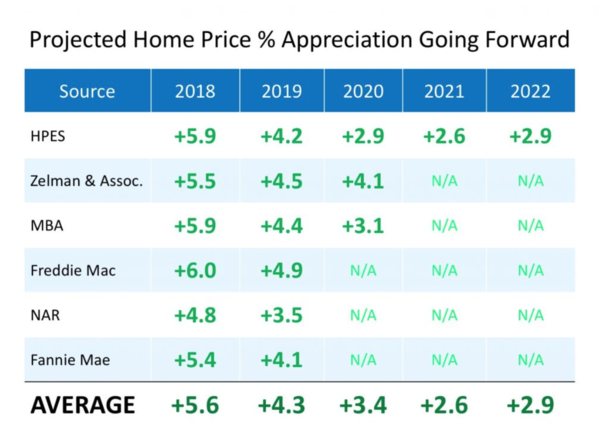

Looking forward – Predictions of the experts on home appreciation growth over the next 3-5 years

This chart has been updated from November to include predictions of where things are headed in the future. Some of the larger organizations that provide information to the industry are showing a slow turn to the downside. And, important to note, there are no numbers indicating a reduction in price.

Corelogic’s State by State forecasted changes in price

Price appreciation most often happens in the south and on the coast, where many people tend to move as they get older. No projections are in the red for any state. Historically speaking, most of the country is looking at a very substantial increase in terms of price. The numbers are solid, and if this trend continues through 2019, it will be a very good year.

December 2018 Housing Market Update – Orange County

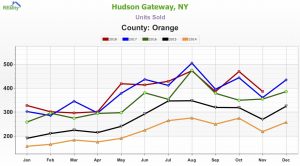

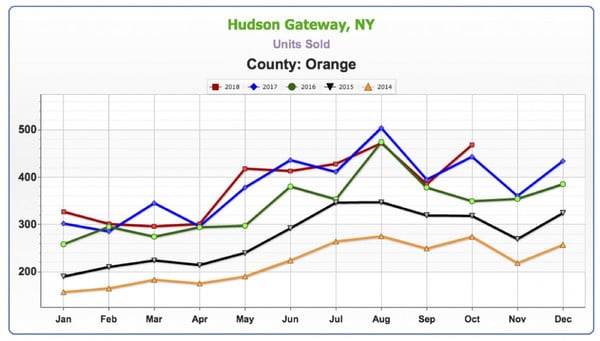

Units Sold

The red line representing 2018 shows there is not too much of a variance between this year and last year.

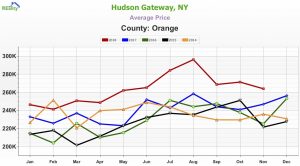

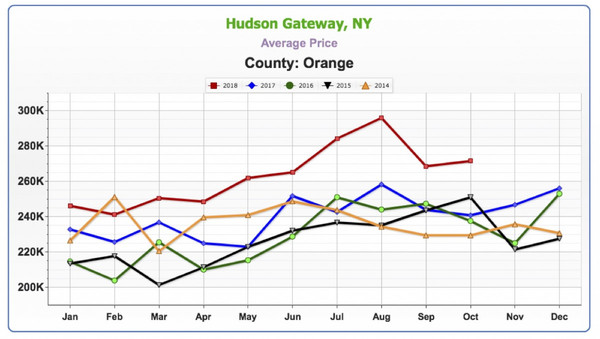

Average Price

Prices spiked during the summer and have been simmering down, coming a little closer to 2017’s numbers.

Average Sold to Asked Ratio

This number shows the price the home sold for versus the last asking price. The higher the number, the hotter the market. This is a mixed bag result from 2018 over 2017.

The Green Team’s November 2018 Housing Market Update was held live on Facebook Tuesday, November 13 at 2 p.m. If you missed the live webinar, you can view it at your convenience by clicking here.

Geoffrey Green , President/Broker of Green Team Home Selling System, moderates the monthly webinar and presents the national stats, as well as the market updates for Orange and Sussex Counties. This month he is joined by Pam Zachowski and Keren Goren of Green Team New Jersey Realty and Vikki Garby, Green Team Home Selling System, Warwick.

Joe Moschella, Branch Manager and Vice President of Lending, and Amy Green, Vice President of Lending, of Guaranteed Rate discuss market updates from a mortgage industry perspective.

The National Outlook

According to Geoff Green, it’s a very exciting time in the housing market right now as we’re starting to see some shifts. We’re experiencing all-time highs reminiscent of 2008 over the last 18 months. It does seem like things are cooling off. According to Michael Fratantoni, Chief Economist of the Mortgage Bankers Association, he expects that home sales growth will pick up again over the next year, even with somewhat higher mortgage rates, though the pace of price growth will likely slow.

Despite the fact that national and local numbers indicate that the velocity of homes selling is actually slowing, Fratantoni and some others are predicting that it is going to increase in 2018. So, it’s not that appreciation is going down, it’s just slowing down.

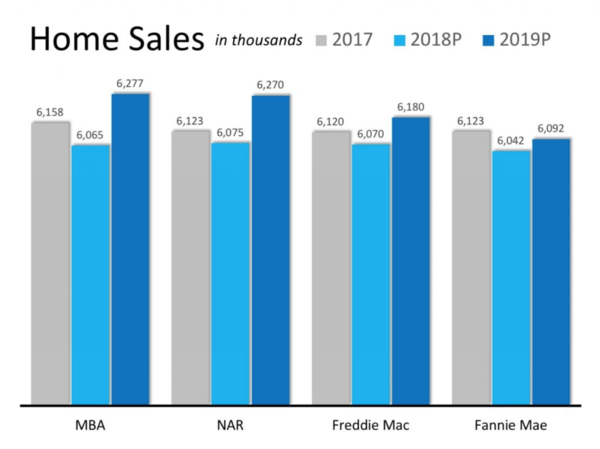

The Mortgage Bankers Association, National Association of Realtors, and Freddie Mac, with the exception of Fannie Mae, all are predicting increases over the past two years. All are predicting increases over the past year. For the most part each of these organizations wants the housing market to continue to grow. Geoff reminds us that it’s in their best interest. It’s important to be aware of the source of information. During the downturn In 2006, 2007 and 2008, during the downturn, some organizations were putting out information that did not accurately portray what was happening. However, you can rely on the Green Team to put out information that is accurate and honest.

In projections for 2018 through 2022, everyone seems to have a positive outlook that the market will continue to appreciate. Just at a slower pace.

November 2018 Housing Market Update – Orange County

Units Sold

While this is hyper local, it is reflective of the 2018 national numbers. While prices may increase and decrease, depending on inventory, units sold have been a mixed bag this year versus last year. It’s been up, it’s been down.

Average Price

Geoff has found that price always lags activity, according to his observations over the past 14 years. If you start to see a slowdown in activity, 6 to 8 months later you’ll start to see a slowdown in the rate of price increases.

Sold to Asked Ratio

This is telling you at what percent of the asking price your home is selling for. The closer you are to 100%, the hotter the market. While this took a little dip recently, it is still at very high levels.

November 2018 Housing Market Update – Sussex County

Units Sold

This is a small data sample that is still reflective of what is happening nationally. Again, it’s a mixed bag, up, down, then often flat.

Average Price

Average price never really gained a tremendous amount of traction, as compared to Orange County, where there had been increases in price.

Sold to Asked Ratio

This looks similar to what is happening in Orange County.

Panel Discussion

The Sales Associates Points of View

Geoff asked Vikki what changes she’s seen since she was last on the panel about 4 months ago… Vikki agreed that she has been seeing a little bit of a slowdown, part of which she believes is due to timing. Many families time their house hunting to coincide with the start of school. However, what she’s finding is a lot of people are looking for land. Historically, we’ve had low inventory compared to the number of buyers, And, as existing house prices go up, more people are starting to consider new construction. Housing starts will be up 9% beginning of the coming year. So there is still a lack of inventory.

Pam also sees a slowdown. More people are looking for homes, but between the low inventory, the start of the school year, people are taking their time. She still sees investors trying to buy and flip homes but finding it harder and harder to find that good deal that makes it worthwhile.

Geoff then asked about appraisals. Are there issues with properties appraising, or are there now enough comps in the marketplace? Keren has not seen any problems recently. They’re all coming in at asking and a little bit above. One thing she has noticed is Sellers asking for CMA’s or listing presentations, more than she had over the summer. Keren always advises clients that we only know what the market is right now and can’t tell where it’s going. She lets them know that low inventory makes it a good time to put their home on the market, as opposed to waiting for Spring, Geoff replied that sellers that were holding off putting their home on the market may now decide to take a chance, seeing that the market is cooling off a little. This may ultimately bring more inventory and more transactions to the marketplace as a whole. There are still many buyers out there, anxious to find a home.

A Mortgage Industry Point of View

According to Joe Moschella, over the last 5 months they’ve seen a steady rise in interest rates. The year started with a 10-year treasury note at 2.21% and this week it was 3.21%, one full percent. That, along with the Fed stopping its purchasing of mortgage-backed securities, caused a liquidity crunch in the market. This contributed to pushing rates up. They started the year with 4% on a 30-year fixed rate and are now closing in on 5%.

Geoff asked Joe what the bond market was like 4 years ago on a percentage basis, just to give some perspective. Joe brings it back to 9/11, when the Fed didn’t want to see the economy spiral down. They jumped in and started dramatically dropping rates, bringing them down to almost zero. Now we’re seeing the unwinding of these artificially low rates. Thankfully the Fed eased into this, providing a “soft landing.” 2.21 to 3.2% represented about ¾ of a percent, interest rate wise. About 2, 2-1/2 years ago we were at 1.2% on the US Treasury. Before that, we were at the 0.7, 0.8% range. We’ve seen a steady rise, which hopefully the economy is strong enough to handle.

Some of the other changes in the market on the mortgage front are in the role technology is playing. Lenders are able to verify client’s income and assets automatically, do the application online and do the process without sending any paperwork back and forth. The whole process is done digitally.This is revolutionizing the industry and leading to higher consumer satisfaction. The industry is also easing credit standards. Geoff asked if easing credit standards was necessarily a good thing. Joe responded that rising rates have opened the door for new loan products to come out. Those new products are not coming from the banks, but rather from private equity firms flowing back into the market. No verification loans do not exist, but they have a bank statement loan that has come back into play. No seasoning waiting period for someone who had a foreclosure or bankruptcy or short sale, whereas before you had to wait three, four or seven years. Geoff stated that if you’re talking about private equity, they basically can do whatever they want with their money, as long as those products don’t make it into mortgage-backed securities. He asked if there were any controls in place to make sure that didn’t happen again. The trade-off with non-conforming products is that the buyer has to have some “skin in the game.” They need a sizeable down payment, and investors want higher return for higher risk, so rates may be at the 6-1/2% range.

Geoff said it’s important to keep things in perspective. The sky won’t be falling if rates hit 6-1/2%! Historically, it’s a pretty average rate.

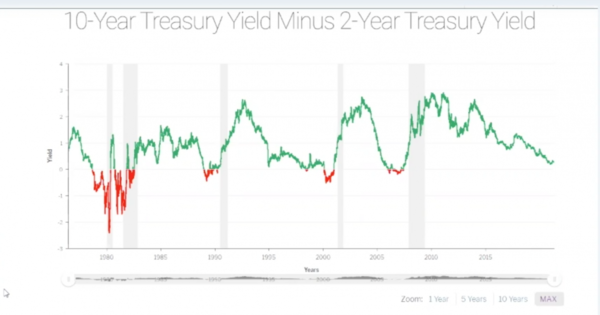

Joe and Amy had a graph showing 10-year treasury yield minus 2-year treasury yield. Historically when those yields come together, it signals a slowdown in the market or a recession. From Joe’s perspective, we might have a slow down in the stock market and see a pull back, but he’d rather see a market that goes up and goes down. In a stale market buyers and sellers are sitting on the fence; there is no call to action. As far as housing goes, everyone can do well and make some money.

Geoff thinks there is enough pent up demand from 2008 to 2016; there are a lot of people who need to buy a home and rates are still low enough. The American housing market is the place to be in the Global real estate market. There may be a continued cooling off and slow down a little. We’ve been at such high levels right now, it had to. Like the stock market, it can’t keep going up indefinitely; at some point it has to come down.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Green Team New York Realty is pleased to announce that Tammy Scotto has just received her Commercial and Investment Real Estate Certification. The CIREC covers a variety of topics that are important to handling Commercial and Investment transactions.

Green Team New York Realty is pleased to announce that Tammy Scotto has just received her Commercial and Investment Real Estate Certification. The CIREC covers a variety of topics that are important to handling Commercial and Investment transactions.