Thanksgiving. It’s a time of gratitude, friends and family; of turkey and all the trimmings. And at the Green Team, it’s a time to let clients know how much they are valued. The Client Appreciation Program, or CAP, is the cornerstone of the Green Team’s foundation. The Green Team doesn’t take its clients for granted. Through the CAP program sales associates find ways to say “I appreciate you” throughout the year. However, one of the highlights of the program is Thanksgiving Pie. A Green Team CAP tradition, clients are invited to come to the office for a casual party. And to pick up their Thanksgiving pie. Because this gift from their sales associate is a way of saying “Thank You.” Thank you for your business, your referrals, and your friendship.

Thanksgiving Pie… A “family” event for both the Warwick and Vernon Offices

Walking into either office you can feel the warmth and joy and know that you are welcome. Pies are stacked high, waiting to be distributed. Being a local brokerage, it’s important to the Green Team to support other local businesses. Thus Noble Pies has become part of the tradition. Their pies are baked from locally sourced ingredients when available. Cider, wine, donuts and more await the clients as they drop in to pick up their pies. And, of course, there is laughter; lots of laughter!

Green Team Sales Associates agree that the Client Appreciation Program is something they themselves appreciate. It keeps the focus on the people who are most important to their businesses: their clients. And events like this one bring everyone together, strengthening bonds between associates and between clients and associates. Probably one of the best things is that two days later pies from the Green Team’s sales associates will be sweetening Thanksgiving Dinners at many homes. Again letting clients know how much they are appreciated.

The Green Team’s October 2018 Housing Market Update was held live on Facebook Tuesday, October 16 at 2 p.m. If you missed the live webinar, you can view it at your convenience by clicking here.

Meet this month’s Panelists from Green Team New Jersey Realty and Green Team Home Selling System

Geoffrey Green, President/Broker of Green Team Home Selling System, is the moderator of the monthly webinar and presents stats and market updates for Orange and Sussex County. He is joined this month by Keren Gonen, Pamela Zachowski and Alison Miller of Green Team New Jersey Realty in Vernon and Jacqueline Kraszewski of Green Team Home Selling System in Warwick.

Market Update – The National Perspective

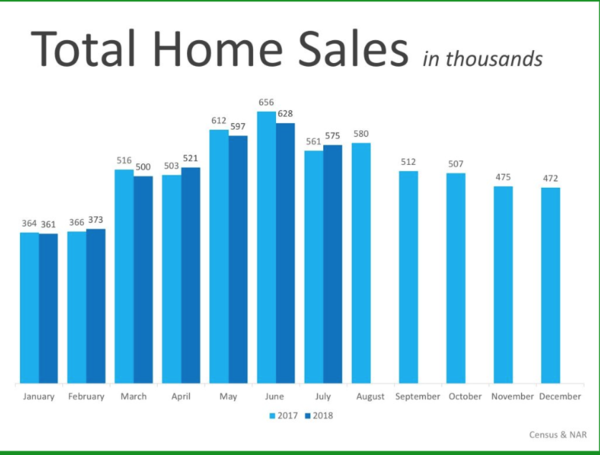

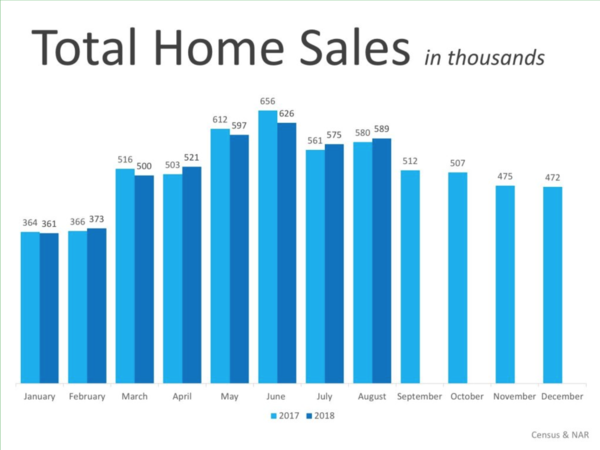

A look at Total Home Sales Nationally

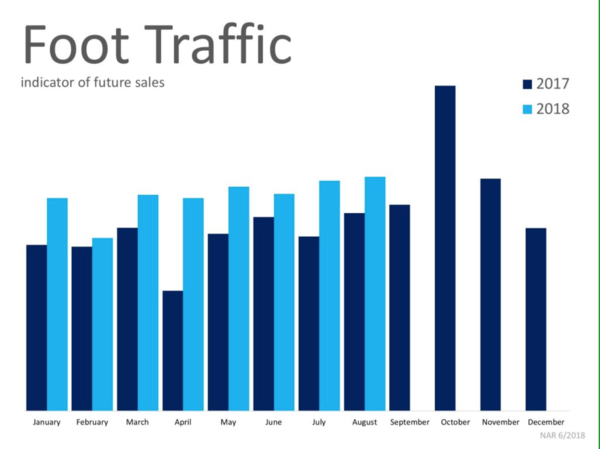

Things seem to be shifting in the housing market. For Geoff, the stats of homes sold are the “mother’s milk” of the industry. Nationally it’s been a mixed bag through 2018. September’s numbers are not yet in, but August numbers for total home sales were just about even for 2017 and 2018. It appears that things are shifting in the market, with the number of sales not increasing like last year, year over year. However, foot traffic in August was much higher in 2018 than in the same period in 2017.

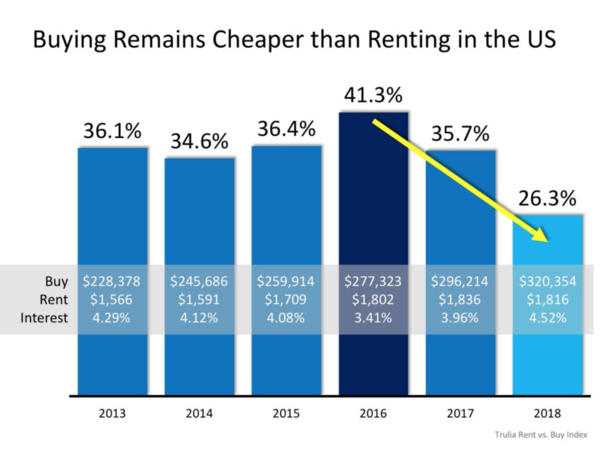

Buying versus Renting…Which is the best way to go?

Lawrence Yun, the economist of NAR, has said that we’ll probably see growth in terms of the housing market on the lower end because the job market is strong. People are working, making money and want to invest their money in real estate. However, there may be a slowdown in the higher end because interest rates are rising. How does affordability of renting compare with buying? There is a steep curve, not a good outlook for renters. Since 2013 it has been cheaper to buy instead of rent on an overall national basis. If you have the ability, it costs less to buy than to rent on an overall monthly basis.

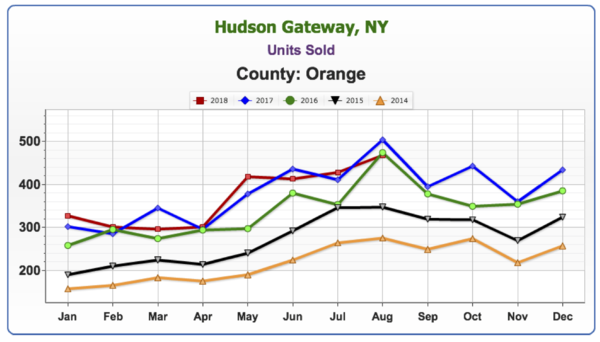

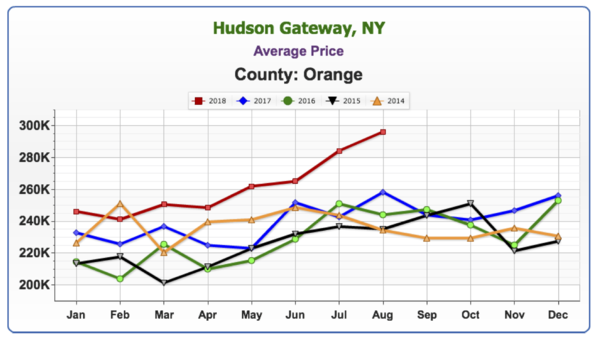

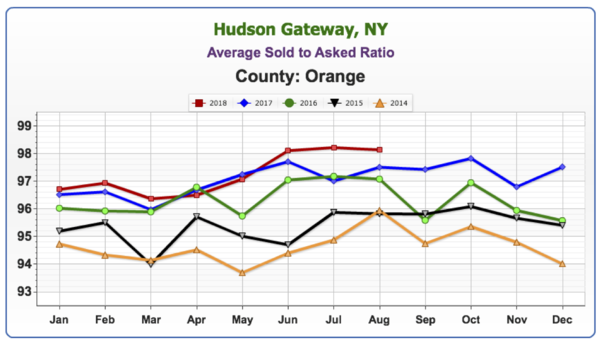

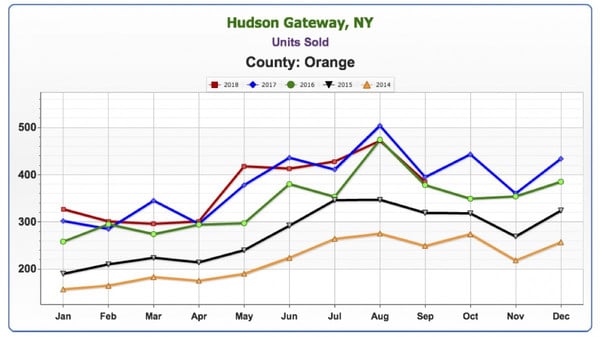

October 2018 Housing Market Update – Orange County

Units Sold

As stated before, Geoff sees this number as the mother’s milk of the housing market. This all-important number gives us a snapshot of how many homes are selling. The number of units sold in Orange County appears to be cooling off. He believes we’ve seen the peak of the last runoff and that it’s behind us. Geoff’s view seems to be backed up by an article that appeared last week in the Wall Street Journal, which referred to a soft downturn in the market.

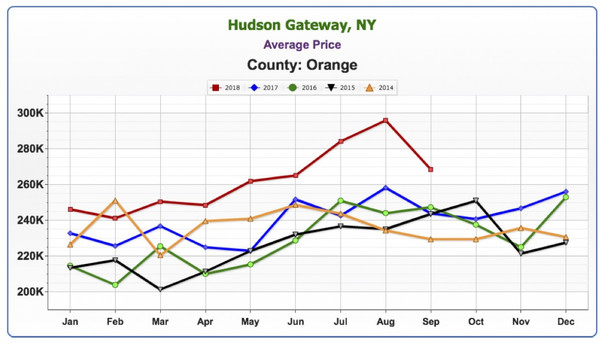

Average Price

There is a big variance in price from where we were last year. The downward trend is a seasonal fluctuation and not a cause for concern. Price always lags units sold at least 6 months or more. Price increases may occur over the next 6 to 12 months, even though the number of units sold is dropping.

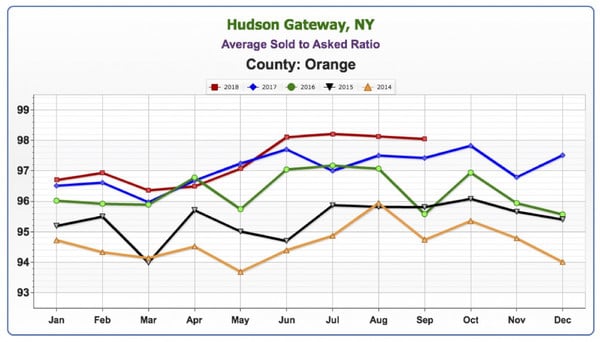

Average Sold to Asked Ratio

We are still pretty high, still over 98%, which means sellers are only having to negotiate 2% from their asking price.

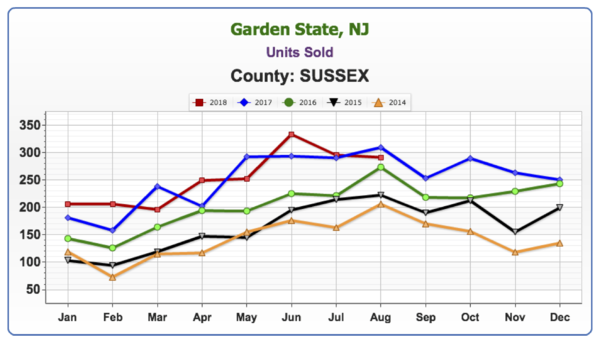

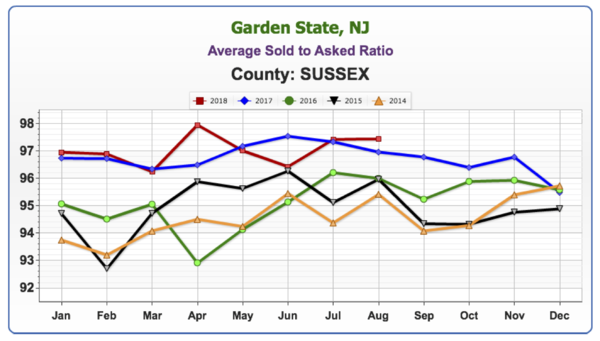

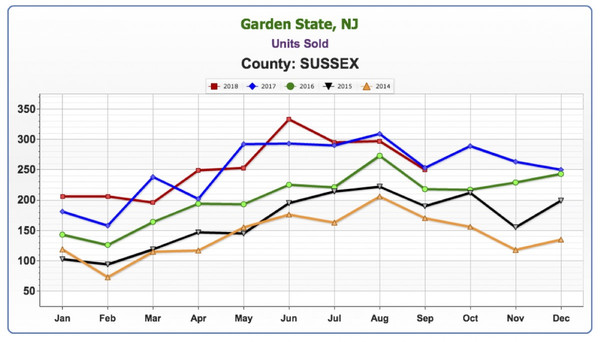

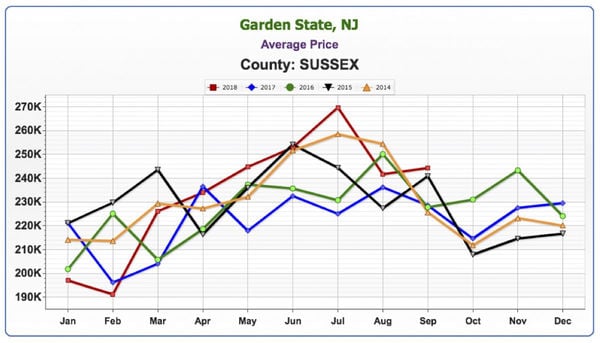

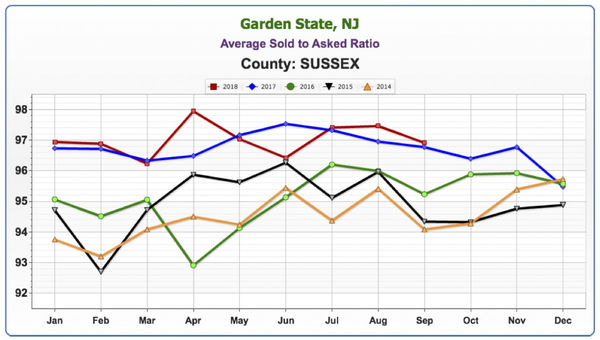

October 2018 Housing Market Update – Sussex County

Units Sold

A similar trend to Orange County, where some months are up, some down, on a year over year basis. It’s a mixed bag, and the numbers seem to indicate a cooling off.

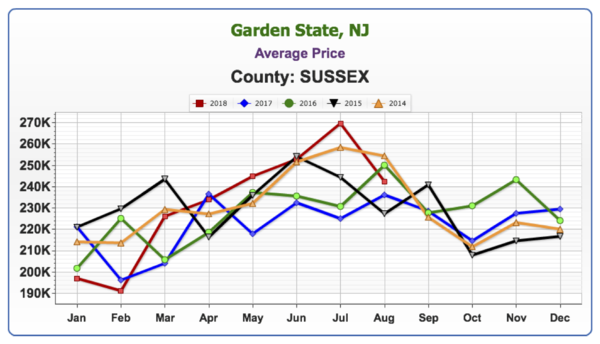

Average Price

Average prices never rocketed in Sussex as they did in Orange County. In previous updates, we’ve spoken about how there is simply more foreclosure inventory and activity which has dragged down the average. However, that doesn’t mean that homes that are well maintained and well located haven’t done well.

Average Sold to Asked Ratio

Average price never rocketed here like it did in Orange County. There has been much more foreclosure inventory and activity in Sussex and that has dragged down the average home price. However, that doesn’t mean that well-located, well-maintained homes haven’t done well.

Slightly below Orange County, the numbers are still hovering around 98%.

Panel Discussion

The Sales Associates Point of View

Geoff believes the market is cooling. He asked the panelists what they were sensing in the field. Keren replied that there are fewer houses that are updated and nicely done, and buyers have higher expectations. During the summer, people were rushing to find homes in order to get situated before the start of the school year. Without that added stress, many buyers are being pickier. Alison finds that people are looking for something that is just not there. Inventory is not meeting the demand. In addition, many of her closings were delayed, affecting numbers for September.

Jacque is finding that there is a lack of finished, move-in-ready homes under the $400,000 price point in Warwick. In addition, many families with school-aged children are waiting for the spring to resume their search. Also, the seasonal fluctuation impacts the market as people are beginning their holiday preparations. Pam is also seeing the issues mentioned by the other sales associates. The inventory shortage, buyers being very picky, even homes that have been flipped that aren’t good enough. It’s difficult for people to find what they’re looking for in their dollar amount.

Geoff summed up these comments by stating it is still a very good time to sell a house. However, there is nothing to stop the housing market from slowing down. Thus he advises sellers not to put off listing their home if they are planning on selling.

Guest Panelist, Matt Zagroda, discusses the bond market…

Matt Zagroda is a Sales Manager at MBS Highway, the leading provider of real-time market data for mortgage professionals. As such, Geoff welcomed his input on the bond market. Geoff asked Matt what is happening with the bond market, as rates seem to be increasing by the minute. Matt explained that at the end of last year the Fed wanted to do quantitative tightening. Previously they had been reinvesting gains from the bond market back into the bond market, which brought their balance sheet up greatly.

They wanted to wind that balance sheet down and made a plan just before Janet Yellen stepped down as Fed Chair. So, October of last year they wanted to reduce it by $10 billion. January of this year, $20 billion, April $30 billion, July $40 billion and October, $50 billion. That was the last tightening session. They weren’t going to continue to reinvest it. There is no Fed buying into the bond market, which is why we’re seeing changes in interest rates. There was a drop in the bond market and a rise in rates.

Matt expects that in the upcoming months we’ll be experiencing volatility. However, this is actually a more normal bond market. If there is any economic news that would potentially hurt bonds, we’ll notice it more. Previously the Fed was buying back into it, softening the blow, creating almost a safety net. Now there is no safety net, so if it’s going to hurt – it’s going to hurt. That doesn’t mean that if there’s good news that it will be the opposite and that it will help the bond market… Again, the Fed is not juicing the good news to buy and make that increase even more so.

More volatility is expected into the future, potentially more to the downside, but it’s not expected to be a straight downward line. Rates may continue to get worse, though the hope is that they’ll remain steady. Much depends on what happens with the Fed and their plans for rate hikes.

Geoff recalled buying his first home around 2003. His 30 year fixed rate was at 6.5%. We’re hovering now at about 5% now. Matt agreed that was about right.

Looking back, it hasn’t been higher than this since 2009. Previously, it was much higher. Rates have been pretty much below 5% since then. The largest run on the housing market was 2005, 06, 07 and rates were pretty high back then. The rates may impact the mortgage industry insofar as refinancing. However, when rates eventually come down, the refinancing market should open up again.

… the stock market, and global contagion

Geoff asked Matt his thoughts on the stock market and its unbelievable run. Matt expects that eventually we can’t go much higher and things will come back to a more normal range. Not a crash, but just a more normal range that will help bonds and interest rates even a little bit. When money comes out of stocks it is generally invested in bonds, especially when there’s talk of trade wars, etc. When there is uncertainty in the market, many people invest in safer, long-term investments like bonds.

Geoff had a final question… The idea that there could be a global contagion. By and large, there is a lot of risk around the globe. Many governments are not in a good fiscal situation. Currencies are all over the place. There’s a lot of risk around the globe. The US seems like the shining city on the hill, on our own pedestal for some time. He asked Matt his thoughts on the global market. Matt replied that there is turmoil in Europe, and especially Italy right now. The world is interconnected. However, we’re not expecting great leaps and bounds right now because of that turmoil. However, it does affect us.

In closing, Geoff recommends the article he mentioned at the beginning of the update. Written by Laura Kusisto, it was published in the Wall Street Journal on October 13. “Housing Market Positioned for a Gentler Slowdown Than in 2007″ provides a good, historical outlook on the market and its future.

The Green Team Home Selling System is pleased to announce Pip Klein as 3rd Quarter Sales Leader.

“Ever since I got my license in 2011, it was always a personal goal to win a quarterly award. In the beginning it felt unattainable. But with every transaction, every year that passed, I knew I was learning and growing as an agent.”

A Natural People Person…

Pip feels fortunate to be part of the Green Team and to have found a new career at this point in her life. “I was at a turning point,” adds Klein. “Many of my peers were starting to slow down or retire, when Geoff Green encouraged me to dive head first into this fascinating business.” At the time, Pip had her late parents’ home to sell and as a natural “people person,” she was an ideal candidate to become an agent. “I am so grateful that Geoff gave me that push and this opportunity to put my skills to work in this industry. It’s been a great journey and I love working in my hometown!”

According to Geoff Green, “It’s hard to believe, because she is such a great producer, that this is Pip’s first quarterly Sales Leader Award. That said, it has come at the busiest time of the year in the fastest moving market that Pip has experienced in her career as a Realtor. So this is a truly awesome accomplishment. And probably the first of many such awards for Pip.”

As a copywriter for the Green Team, one of my jobs is to do write-ups of the various webinars held by the company. On October 10, 2018 a special webinar was held on Facebook. Team Up for Hope: The Green Team Live with NAMI Orange County, NY. For those unfamiliar with the organization, NAMI stands for the National Alliance on Mental Illness. It is the largest grassroots organization in the nation dedicated to building better lives for the millions of Americans affected by mental illness. It operates on national, state and local levels by volunteers who are themselves impacted by mental illness. And these volunteers go through extensive training to offer education, support and advocacy to those of us who have had our lives turned upside down.

So why is a real estate company spending time talking about mental illness? Because the Green Team cares about what happens in the communities we’re part of and which we serve. Every year we raise money for a local charity. This year, our committee felt that we should do something more than hold a fundraiser. We decided to team up with NAMI for an initiative to help end the stigma surrounding mental illness and to provide much needed information to our communities. Thus, this webinar was held, featuring two members of NAMI Orange who presented the personal side of mental illness as well as information and the services NAMI offers.

About our guest panelists

Marcy Felter and Sheila Sutton are working with the Green Team’s Team Up for Hope Committee, educating us on mental illness and the services that NAMI offers. We are also working with Annie Glynn, President, and Jeri Doherty, Treasurer, of NAMI Sussex. Marcy and Sheila volunteered to do the webinar on behalf of both NAMI Affiliates.

Marcy is Chair of the Education Committee, teaches the NAMI Basics and Family to Family Courses, is a Family Support Group Facilitator and serves as a volunteer for Families Helping Families at Orange Regional Medical Center. She is also teaching a new NEABPD (National Education Alliance on Borderline Personality Disorder) class on Borderline Personality Disorder. Hosted by NAMI, this is the first class of its kind being offered in Orange County.

Sheila is a member of the Board of Directors and manages the lending library. She also teaches the NAMI Basics and Family to Family Courses, is a Family Support Group Facilitator and serves as a volunteer for Families Helping Families at Orange Regional Medical Center. In the webinar, Sheila shares her powerful story of the effects of mental illness on her son and her family and how NAMI changed her life.

To write or not to write, that is the question

As I watched the webinar, I realized that I could not do justice to what I was hearing and seeing. To do so would be to rob it of its power, its intent, and its ability to reach people. So I am going to ask everyone reading this to watch the webinar. Spend a few minutes learning about the lives many of you, your family, your friends and your neighbors are living. There are people living in the shadows, afraid of discrimination, bullying, being deserted by friends and family… being judged. Imagine living in fear for a loved one, not understanding what had happened, where that person went, what to do when things got out of control and scary… And then being thrown a lifeline by people like the two women talking to us. And that is exactly what NAMI is, a lifeline.

Mental Health First Aid Class – to learn how to identify, understand and respond to symptoms of mental illnesses and substance abuse disorders in your community

The September Housing Market Update was held live on Facebook Tuesday, September 18 at 2 p.m. If you missed the live webinar, you can view it at your convenience by clicking here.

Geoffrey Green, President/Broker of Green Team Home Selling System, is the moderator of the webinar and presents stats and monthly market updates for Orange and Sussex Counties. Keren Gonen of Green Team New Jersey Realty, and Jacque Kraszewski of Green Team Home Selling System provide perspective on the market from the sales associate’s view. Michael Gianetto of Residential Home Funding provides perspective from the vantage point of the mortgage broker. Behind the scenes is Melissa Bressette, putting it all together!

Market Update – The National Perspective

Year over year numbers – There’s been almost no increase year over year in total home sales over 2017. However, Foot Traffic has increased in 2018 over 2017.

From a pricing perspective, Geoff has found in his 14 years in this industry that price always lags units sold. However, we’re still seeing substantial price increases even though units sold is cooling off. There is typically a 6-month lag.

Existing home prices increased the most in the east. followed by the west. The market is still pretty healthy. Locally, we still haven’t seen a huge increase in price like the 2006/2007 levels.

Market Update – Orange County

We’ve been at or below units sold for the last 3 months.

The average price has really shot up.

A very strong number; prices are aggressive, and there are bidding wars.

Market Update – Sussex County

The number sold is still at historic heights, though it is a little lower than August 2017.

Prices went down, August was the lowest number in 3 years. Sussex is still a vibrant market with lots of transactions happening.

Similar to Orange, at or above the 97.5%-98% range.

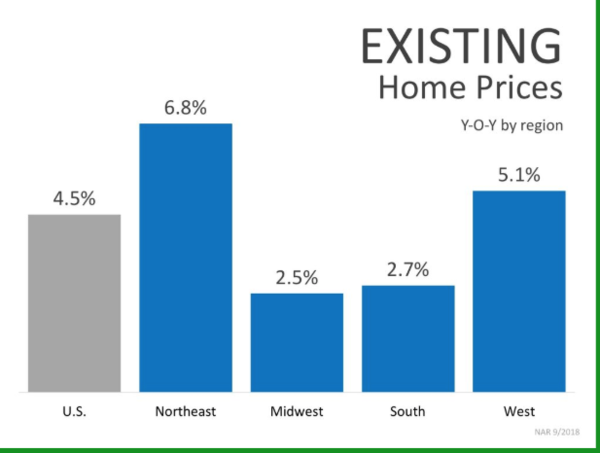

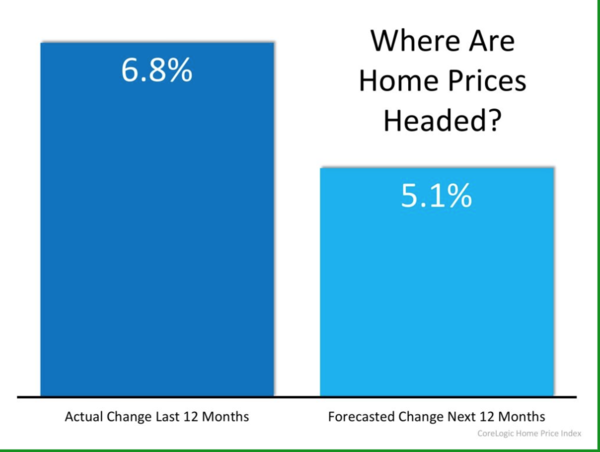

Where are Home Prices Headed?

Nationally, the actual change in the last 12 months was 6.8%, a huge increase. Corelogic Home Price Index is forecasting a 5.1% increase for the next 12 months. This does not mean that prices will be decreasing. It just means they will increase by a lesser amount, which Geoff agrees with. Price usually lags in what is happening with units sold, and we’re seeing that happen. However, it is still a very robust market.

Panelists Discuss the Market

Sussex County Market

Because of the inverse numbers in New Jersey, Geoff asked Keren Gonen her opinion on what’s happening. Keren noted that a lot of transactions had been delayed. It was not an issue of not enough houses or buyers, but a delay in closings. There may be a rise in units sold in September. Regarding the lower price, the banks have released another batch of low priced homes. These usually are bought by flippers and investors, often for cash. That can skew the numbers. These homes were released at the end of July, closed in August. Keren invests and flips homes herself, so she is very knowledgeable on this subject. There are many more foreclosures available in Sussex than in Orange County. Therefore, that’s a major reason for the difference in home price stats for the two counties.

Orange County Market

Geoff asked Jacque Kraszewski where she thought the market was headed. She believes we’re still in a seller’s market. Inventory is still low. She has several buyers she can’t find houses for. She put a house on the market and within 2 days she had 7 offers. People may want to move, downsize, or rent. However, there are no rentals available. The inventory is a problem for renters as well as buyers. Also, some people don’t want to sell then purchase something at a higher interest rate.

Geoff recalled one listing that had 26 offers within 3 or 4 days. It’s hard to talk about a market cooling off when this is going on. You want to look ahead and see what is coming…. From the number of homes being sold on a national, regional and local level, we’ve seen the highs from this last run up and he’s hoping for a soft landing – not a precipitous decline. Jacque commented that there is usually a decline this time of year, with people who are looking to move to a certain school district now waiting for spring to find a home their children can start in, in September.

Geoff replied that there are always seasonal fluctuations, but year over year decreases, same period each year, tell the story. We’re seeing very steady increases in units sold for 4 to 5 years. And now, for the first time, not seeing big increases. The market does seem to be cooling a little.

Mortgage Rates and Availability

Geoff discussed with Mike Gianetto the major factor of the last precipitous decline. There, 50% of the marketplace was lost in a 2-year time span. This was due to the financial mess, mostly created by mortgage-backed securities. He asked Mike if we see a lot of sub-prime lending happening? Are we seeing the mistakes of the past being repeated?

Mike said there was a period of product elimination over 1-1/2 to 3 years. This took the market from somebody fogging a mirror to not giving any money at all. It was prohibitive for buyers less than perfect trying to buy a home. There are now safeguards and regulations saving the downside a little. There is a rise in products that are out there to help people buy. It allows for a lot more people in this marketplace. We have a shortage of inventory but we still have availability of credit and funding. People are lending, the money is out there, and people can get mortgages.

Geoff noted that not only did we have a financial crisis, but also a real tightening of credit making it hard to make a comeback. He asked Mike what’s going on with rates?

Mike said there has been a little uptake in rates. Further, there will probably be another. He thinks next year we may be in for lower rates. We’re at mid to high 4’s now, for a 30 year fixed mortgage. which is still a great rate. People will buy no matter what the rate, but this is still a very good rate.

Geoff replied that it would be good news if rates stabilize or come down next year. He also noted that the unemployment rate is at an 18 year low as of August. Wages are increasing. And the Construction sector added 23,000 jobs in August. Builders are ramping up. So many people were crushed during the last downturn – plumbers, general carpenters, framers, etc. Seeing them become the largest sector of jobs is good news.

Geoff’s take – if you need to buy or sell a home now, just do it. Mike said they can find mortgages for most buyers. If you’d like to contact Mike to discuss a mortgage, you can reach him at his office, 845-496-0836 or visit rhfunding.com/michaelgianetto. You can find Jacque or Keren at greenteamhq.com

Join us for the next Housing Market Update

We’ll be on Facebook live on Tuesday, October 16 at 2 pm. You can also sign up for our Housing Market Updates at GreenTeamHQ.com/HMU.

The Housing Market Update webinar is now sponsored by REALLY – Agent to Agent Referral App. You can learn more at reallyhq.com

Home values have risen dramatically over the last twelve months. In CoreLogic’s most recent Home Price Index Report, they revealed that national home prices have increased by 6.2% year-over-year.

CoreLogicbroke down appreciation even further into four price ranges, giving us a more detailed view than if we had simply looked at the year-over-year increases in national median home price.

The chart below shows the four price ranges from the report, as well as each one’s year-over-year growth from July 2017 to July 2018 (the latest data available).

It is important to pay attention to how prices are changing in your local market. The location of your home is not the only factor which determines how much your home has appreciated over the course of the last year.

Lower-priced homes have appreciated at greater rates than homes at the upper ends of the spectrum due to demand from first-time home buyers and baby boomers looking to downsize.

Bottom Line

If you are planning to list your home for sale in today’s market, let’s get together to go over exactly what’s going on in your area and your price range. Find out what your home’s value is today – click here.

Green Team New Jersey Realty celebrates the opening of their new office building

Just two years and five days after the ribbon cutting that launched the opening of the Green Team’s Vernon office, a new ribbon cutting was held. On Thursday, September 13, Green Team New Jersey Realty (“GTNJR”) celebrated the official opening of its new office building at 293 South Route 94, Vernon, New Jersey. And the ample parking lot was perfect for the celebration that followed.

A little history…

The Green Team Home Selling System, founded in 2005, is in the top ten of all brokerages in Orange County, New York. When Geoffrey Green was approached by agents wanting to open an office in Vernon, New Jersey, it made perfect sense. Vernon was an underserved market, just across the border from Warwick, New York where the Green Team is based. However, even Geoff and equity partners Kim Lasalandra, Charles Nagy and Ted VanLaar couldn’t foresee the rapid growth of Green Team New Jersey Realty. For Charles, real estate has always been about people and making relationships. It’s what he truly loves about the business. However, his long term plans included retirement and relaxation. Now Green Team New Jersey Realty and its rapid success has put all talks of retirement on hold. There are new people to meet, new relationships to forge, and an exciting business to grow.

Utilizing the systems developed by Geoff Green, the Vernon office flourished. At six months there were 8 sales associates. That number kept growing as agents learned about the Green Team’s core values, its unique training and mentoring programs, and its commitment to providing the best possible client service.

In 2017, six GTNJR sales associates were recognized by the New Jersey Association of Realtors for achievement and excellence in sales. Considered among the most prestigious honors awarded to Realtors in the Garden State, the NJAR Circle of Excellence recognizes members who have excelled in the field of salesmanship. Ann Nussberger achieved the Silver Level ($6.5 million and 20 units minimum or 70 units). Recipients of the Bronze award ($2.5 million and 15 units minimum or 30 units) were Barbara Tesa, Joyce Rogers, Charles Nagy, Keren Gonen and Theodore Van Laar.

The future looks great…

As Geoff Green so eloquently put it, “Even though we’re here to celebrate the grand opening of the new building, it’s really a celebration of the people of the Green Team.” In less than two years, Green Team New Jersey Realty has become one of the top 20 real estate agencies in all of Sussex County and is one of the top five in Vernon. Thus, with 18 Sales Associates and a new home, the sky’s the limit. Yes, the Green Team has good reason to celebrate.

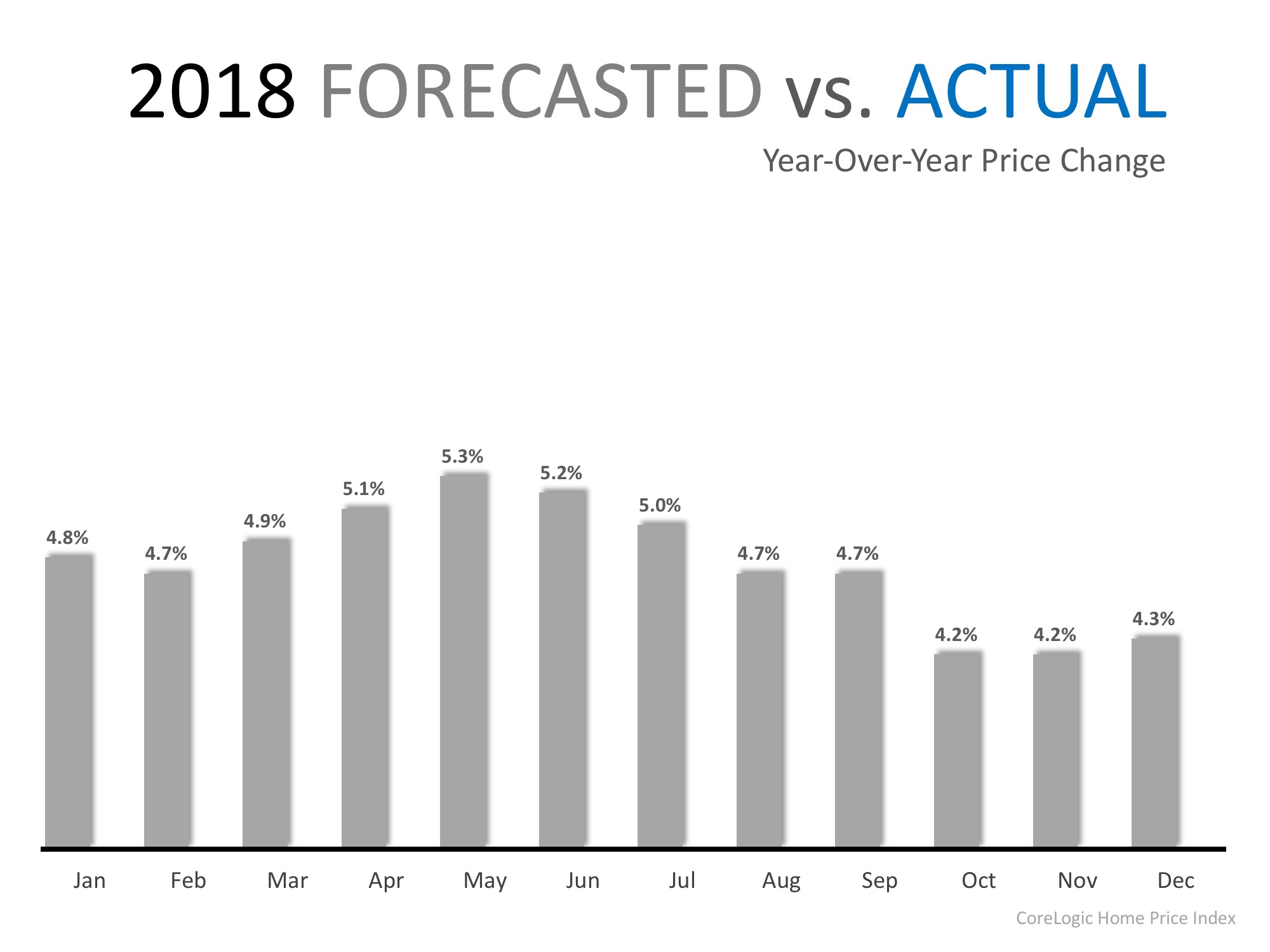

Between 1987 and 1999, which is often referred to as the ‘Pre-Bubble Period,’ home prices grew at an average of 3.6% according to the Home Price Expectation Survey.

Every month, the economists at CoreLogic release the results of their Home Price Insights Report, which includes the actual year-over-year change in prices across the country and their predictions for the following year.

The chart below shows the forecasted year-over-year prices for 2018 (predictions made in 2017). According to their predictions, the average appreciation over the course of 2018 should be 4.8%, which is still greater than the ‘normal’ appreciation of 3.6%.

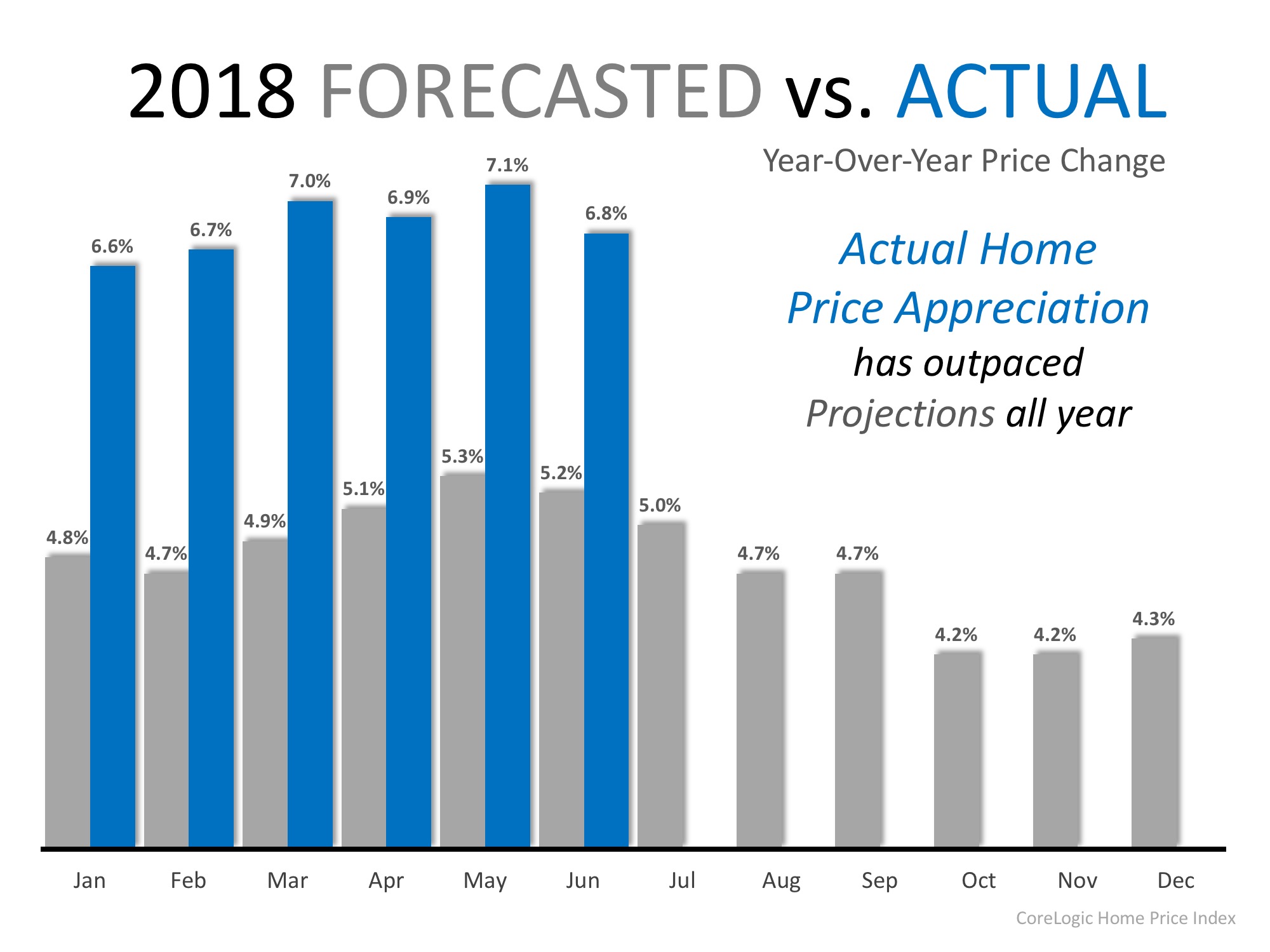

If we layer in the actual price appreciation that has occurred this year, we can see that over the course of 2018, home prices have appreciated by an average of 6.9% and have outpaced projections all year!

What does this mean?

The tale of today’s real estate market is one of low inventory, high demand, and rising prices. The forces at work can be simply explained with the theory of supply and demand. That being said, if a large supply of inventory were to come to the market, prices may start to appreciate closer to the forecasted rate which would STILL be greater than the historic norm!

Bottom Line

If you are a homeowner whose house no longer meets your needs, now may be a great time to list your home and capitalize on the equity you have gained over the last year to make a significant down payment on your next home! Find out what your home is worth.

For the last several years, buyer demand has far exceeded the housing supply available for sale. This low supply and high demand have led to home prices appreciating by an average of 6.2% annually since 2012.

With this being said, three of the four major reports used to measure buyer activity has revealed that purchasing demand may be softening. Here are the four indices, how they measure demand (methodology), what their latest reports said, and a quick synopsis of the report.

Methodology: Every month SentriLock, LLC provides NAR Research with data on the number of properties shown by a REALTOR®. Lockboxes made by SentriLock, LLC are used in roughly a third of home showings across the nation. Foot traffic has a strong correlation with future contracts and home sales, so it can be viewed as a peek ahead at sales trends two to three months into the future.

Latest Report: “Foot Traffic climbed 3.2 points to 55.8 mid-summer in July. Additionally, the diffusion index is higher than last year by 13.5 points. Despite a healthy economy and labor market, supply and new construction remains unable to keep up with buyer demand.”

Methodology: The ShowingTime Showing Index® tracks the average number of buyer showings on active residential properties on a monthly basis, a highly reliable leading indicator of current and future demand trends.

Latest Report: “Showing activity throughout the country increased by 0.3 percent year over year in July, the third consecutive month that the U.S. ShowingTime Showing Index recorded buyer interest deceleration compared to the previous year. The June 2018 figures revealed a 0.0 percent change in showing traffic from 2017, while May showed a 1.2 percent year-over-year increase. The 12-month average year-over-year increase was 4.6 percent.”

Methodology: The REALTORS Confidence Index is a key indicator of housing market strength based on a monthly survey sent to over 50,000 real estate practitioners. Practitioners are asked about their expectations for home sales, prices and market conditions.

Latest Report: “REALTORS reported slower homebuying activity in July 2018…The REALTORS® Buyer Traffic Index registered at 62, down from the same month one year ago (69). This is the fifth straight month (since March 2018) that Realtors reported a decline in buyer activity compared to conditions one year ago.”

Methodology: Proprietary survey results of real estate executives.

Latest Report: “While we continue to expect a resumption of growth in resale transactions on the back of easing inventory in 2019 and 2020, our real-time view into the market through our Real Estate Broker Survey does suggest that buyers have grown more discerning of late and a level of “pause” has taken hold in many large housing markets. Indicative of this, our broker contacts rated buyer demand at 69 on a 0-100 scale, still above average but down from 74 last year and representing the largest year-over-year decline in the two-year history of our survey.”

Synopsis: Buyer demand is softening

Bottom Line

Again, three of the four most reliable measures of buyer activity are reporting that demand is softening. We had a strong buyers’ market directly after the housing crash which was immediately followed by a strong sellers’ market over the last six years.

If demand continues to soften and supply begins to grow (as is projected to happen), we will return to a more neutral market which will favor neither buyers nor sellers. This “more normal” market will be better for real estate in the long term.

Want to know what your home is worth? Get a quick and free home valuation report – Click Here

The last thing in the world you would ever want is to spend a bunch of time searching for a home, finding that perfect place, and then not being approved for your mortgage. There are also many common mistakes homebuyers make that could make the process much more painful than it has to be.

1) Don’t overestimate your budget.

Ever heard the expression “House poor“? Many homebuyers overestimate what they can actually afford and end up with very little wiggle room financially. Before jumping into buying, make sure you have a realistic idea of the yearly costs involved with owning a home.

Remember, there is your mortgage, property taxes, utilities, insurance and repairs. All of this before you even think about making upgrades. Factor in all the costs and leave yourself some room.

2) Don’t let your emotions run wild.

Buying a home is one of the biggest decisions of your life. It’s normal to be excited and fall in love with a home. However, try to keep a level head. Falling in love with a home can cloud your judgement or end in disappointment. This can happen if unforeseen issues are exposed in the inspection or if someone puts in an offer before you.

If you don’t find a home… don’t get discouraged. Home searching can be a lengthy process. It will be worth it when you find the winner.

3) Don’t talk to sellers about plans for the house.

As much as you are excited to get in and put your personal touch on the home, it’s best to keep this to yourself. Sometimes home buyers meet and get to know the home owners. This is fine, but remember that the current owner will have an emotional attachment to the property.

It’s best not to make them feel like you’re going to come in and completely change the place. If you make conversation with the owners, just keep the conversation light.

4) Don’t withdraw or deposit a lot of cash.

Going further with your financial history, cash withdraws and deposits also play a part in your mortgage approval rate. Large quantities of cash going in or out of your accounts signals a warning sign that you do not have stability. Avoid any sporadic withdraws or deposits of large sums of cash.

5) Don’t apply for more credit.

The amount you are approved for on your mortgage comes down to your capital. How much money do you have at your disposal? Applying for extra credit increases your debt. This extra debt decreases the amount you will be approved for on a mortgage.

6) Don’t co-sign a loan.

While a loan may not technically be yours – it will still equally count towards your overall debt. Co-signing a loan can have an impact on not only the amount of your mortgage but approval rate in general. Avoid co-signing any loans until you have purchased your home.

7) Don’t finance a car or furniture.

As financing is again a loan, it is therefore debt. Stay away from financing a car or furniture for the above mortgage approval reasons.

8) Don’t switch or leave your job.

Financial stability is one of the most important factors considered when a bank is approving your mortgage. The key to financial stability is having a dependable income. If you switch or leave your job, often or before applying for a mortgage, this may signal red flags.

If you are thinking about a move, hang tight with your job until after your mortgage is approved.

Ensure you don’t make these mistakes

There are many important things to consider when purchasing a home. It is one of the biggest decisions of your life.

In order to ensure that you get the house you want, when you want it, you need to understand and follow those above tips. Doing so will increase your chances of finding that perfect home and getting it. Remember that financials are very important when it comes time to apply for a mortgage. Make that your priority.

Also keep in mind the emotional aspects of purchasing a home and try to stay cool. It can be a draining process, but it will be worth it when you get the keys to the castle! Contact one of our Sales Agents today to help you through every step of the home buying process.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Thanksgiving. It’s a time of gratitude, friends and family; of turkey and all the trimmings. And at the Green Team, it’s a time to let clients know how much they are valued. The Client Appreciation Program, or CAP, is the cornerstone of the Green Team’s foundation. The Green Team doesn’t take its clients for granted. Through the CAP program sales associates find ways to say “I appreciate you” throughout the year. However, one of the highlights of the program is Thanksgiving Pie. A Green Team CAP tradition, clients are invited to come to the office for a casual party. And to pick up their Thanksgiving pie. Because this gift from their sales associate is a way of saying “Thank You.” Thank you for your business, your referrals, and your friendship.

Thanksgiving. It’s a time of gratitude, friends and family; of turkey and all the trimmings. And at the Green Team, it’s a time to let clients know how much they are valued. The Client Appreciation Program, or CAP, is the cornerstone of the Green Team’s foundation. The Green Team doesn’t take its clients for granted. Through the CAP program sales associates find ways to say “I appreciate you” throughout the year. However, one of the highlights of the program is Thanksgiving Pie. A Green Team CAP tradition, clients are invited to come to the office for a casual party. And to pick up their Thanksgiving pie. Because this gift from their sales associate is a way of saying “Thank You.” Thank you for your business, your referrals, and your friendship. important to the Green Team to support other local businesses. Thus Noble Pies has become part of the tradition. Their pies are baked from locally sourced ingredients when available. Cider, wine, donuts and more await the clients as they drop in to pick up their pies. And, of course, there is laughter; lots of laughter!

important to the Green Team to support other local businesses. Thus Noble Pies has become part of the tradition. Their pies are baked from locally sourced ingredients when available. Cider, wine, donuts and more await the clients as they drop in to pick up their pies. And, of course, there is laughter; lots of laughter!

Matt Zagroda is a Sales Manager at

Matt Zagroda is a Sales Manager at