Geoff Green, President of Green Team Realty, welcomed everyone to the February 2021 Housing Market Update. The webinar, held on February 16 at 12 p.m.. examined the housing market on both national and local levels.

If you missed the webinar or would like to view it again, it is available here.

“Existing home sales totaled 5.64 million in 2020, up from 5.6% from 2019 and the most since before the Great Recession.” – NAR

“Home seller profits skyrocketed in 2020. Seller profit on typical sale in 2020: $68,843. Up from $53,700 in 2019 and $48,500 in 2018.” – Atom Data

As Geoff has pointed out throughout 2020, sellers were the ones benefitting from that market. The amount of money made by sellers in 2020 was historic. Furthermore, price projections for 2021 signal an average of 5%. Historically, the housing market appreciates by approximately 3.8%.

Low mortgage rates have been driving the sustained market and affordability. The projections are showing that rates will start to climb from 2021 into 2022. However, the increases are not major. Predictions are a gradual increase to 3.2%.

Inventory at a historical low point

“Total housing inventory at the end of December totaled 1.07 million units, down 16.4% from November and down 23% from one year ago (1.39 million). Unsold inventory sits at an all-time low 1.9-month supply at the current sales pace, down from 2.3 months in November and down from the 3.0-month figure recorded in December 2019. NAR first began tracking the single-family home supply in 1982.” – NAR

Working from home

According to this 2020 Panel Consensus Forecast from NAR, there is a shift towards working from home since 2019. While down from 2020, the forecasts for 2021 and 2022 are at least twice as much as 2019. Geoff sees a restructuring of business models as employees and businesses see benefits of working from home.

What else are we talking about?

We’re talking about the price of lumber and new home sales activity. Also, exiting forbearance plans, housing affordability, and equity benefit of price appreciation

All of these topics are discussed in the February 2021 Housing Market Update.

Housing Market stats on national and local levels

Existing home sales and prices were up, with inventory way down, making for a true supply and demand marketplace.

“Housekeeping” Items

Hear from our Panelists

Finally, the realtors, all from Green Team New Jersey Realty this month, and Michael Giannetto of Cross Country Mortgage, discussed what they are seeing “on the ground.”

Again, if you missed the webinar, you can watch it now to hear the panel discussion. Just click here. And below is the contact information for this month’s panelists.

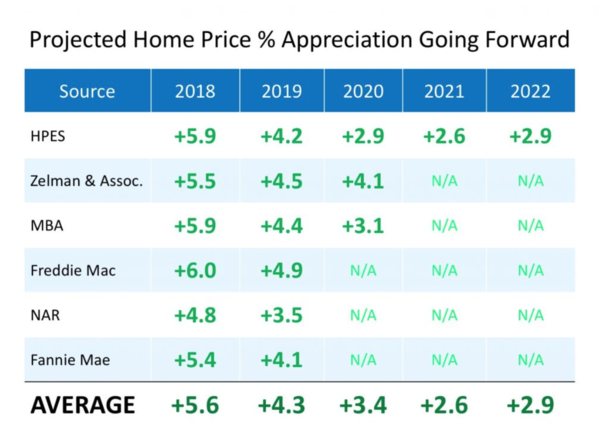

Talk of a housing bubble is beginning to crop up as home prices have appreciated at a rapid pace this year. This is understandable since the appreciation of residential real estate is well above historic annual averages. According to the Federal Housing Finance Agency (FHFA), annual appreciation since 1991 has averaged 3.8%. Here are the latest 2020 appreciation numbers from three reliable sources:

It’s easy to jump to the conclusion that house appreciation is out of control in today’s market. However, we need to put these numbers into context first.

Inflation and the Comeback from the Housing Crash

Following the housing crash, home values depreciated dramatically from 2007-2011. Values are still recovering from that unusually long period of falling prices. We must also realize that normal inflation has had an impact.

Bill McBride, the founder of the well-respected Calculated Risk blog, recently summed it up this way:

“It has been over fourteen years since the bubble peak. In the Case-Shiller release today, the seasonally adjusted National Index, was reported as being 22.2% above the previous bubble peak. However, in real terms (adjusted for inflation), the National index is still about 2% below the bubble peak…As an example, if a house price was $200,000 in January 2000, the price would be close to $291,000 today adjusted for inflation.”

The COVID Impact on Home Prices

The pandemic caused many households to reconsider whether their current home still fulfills their lifestyle. Many homeowners now want larger yards that are both separate and private.

Their needs on the inside of the home have changed too. People now want home offices, gyms, and living rooms well-suited for video conferencing. Barbara Ballinger, a freelance writer and the author of several books on real estate, recently wrote:

“While homeowners continue to want their outdoor spaces that offer a safe retreat, that appeal has shifted into other parts of the home, coupling comfort with function. In other words, homeowners want amenities for work and leisure, and they plan to enjoy them long after the pandemic.”

At the same time, concerns about the pandemic have caused many homeowners to put their plans to sell on hold. Realtor.com just released their November Monthly Housing Market Trends Report. It explains:

“Nationally, the inventory of homes for sale decreased 39.2% over the past year in November…This amounted to 490,000 fewer homes for sale compared to November of last year.”

More people buying and fewer people selling has caused home prices to escalate. However, with a vaccine on the horizon, more homeowners will be putting their houses on the market. This will better balance supply with demand and slow down the rapid appreciation.

That’s why major organizations in the housing industry are calling for much more moderate home appreciation next year. Here are the most recent forecasts for 2021:

Finally, let’s put to rest some of the concerns that today’s scenario is anything like what led up to the last housing crash. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains why this is nothing like 2006:

“Such a frenzy of activity, reminiscent of 2006, raises questions about a bubble and the potential for a painful crash. The answer: There’s no comparison. Back in 2006, dubious adjustable-rate mortgages taxed many buyers’ budgets. Some loans didn’t even require income documentation. Today, buyers are taking out 30-year fixed-rate mortgages. Fourteen years ago, there were 3.8 million homes listed for sale, and home builders were putting up about 2 million new units. Now, inventory is only about 1.5 million homes, and home builders are underproducing relative to historical averages.”

Bottom Line

Most aspects of life have been anything but normal in 2020. That includes buying and selling real estate. High demand coupled with restricted supply has caused home prices to appreciate above historic levels. With the end of the health crisis insight, we will see price appreciation return to more normal levels next year.

With over 90% of Americans now under a shelter-in-place order, many experts are warning that the American economy is heading toward a recession, if it’s not in one already. What does that mean to the residential real estate market?

“A recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

COVID-19 hit the pause button on the American economy in the middle of March. Goldman Sachs, JP Morgan, and Morgan Stanley are all calling for a deep dive in the economy in the second quarter of this year. Though we may not yet be in a recession by the technical definition of the word today, most believe history will show we were in one from April to June.

Does that mean we’re headed for another housing crash?

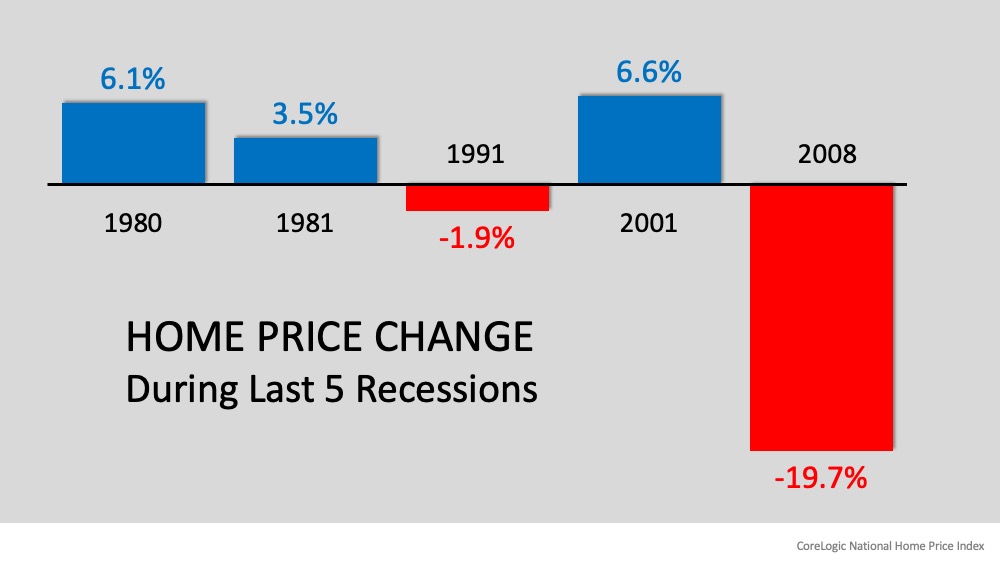

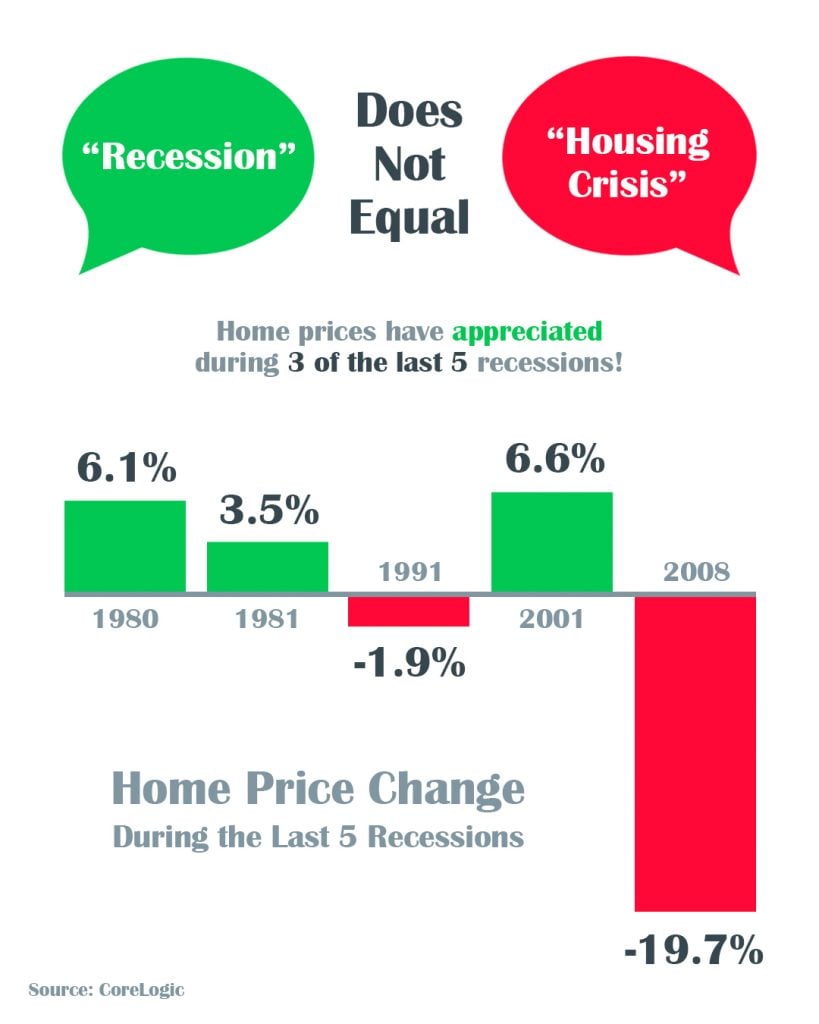

Many fear a recession will mean a repeat of the housing crash that occurred during the Great Recession of 2006-2008. The past, however, shows us that most recessions do not adversely impact home values. Doug Brien, CEO of Mynd Property Management,explains:

“With the exception of two recessions, the Great Recession from 2007-2009, & the Gulf War recession from 1990-1991, no other recessions have impacted the U.S. housing market, according to Freddie Mac Home Price Index data collected from 1975 to 2018.”

CoreLogic, in a second study of the last five recessions, found the same. Here’s a graph of their findings:

What are the experts saying this time?

This is what three economic leaders are saying about the housing connection to this recession:

“The housing sector enters this recession underbuilt rather than overbuilt…That means as the economy rebounds – which it will at some stage – housing is set to help lead the way out.”

“Last time housing led the recession…This time it’s poised to bring us out. This is the Great Recession for leisure, hospitality, trade and transportation in that this recession will feel as bad as the Great Recession did to housing.”

John Burns, founder of John Burns Consulting, also revealed that his firm’s research concluded that recessions caused by a pandemic usually do not significantly impact home values:

“Historical analysis showed us that pandemics are usually V-shaped (sharp recessions that recover quickly enough to provide little damage to home prices).”

Bottom Line

If we’re not in a recession yet, we’re about to be in one. This time, however, housing will be the sector that leads the economic recovery.

Geoff Green, President of Green Team Realty, welcomed everyone to the February 2020 Housing Market Update held on Tuesday, February 18 at 2 p.m.. Topics to be discussed include the coronavirus and its potential impact, as well as the upcoming elections and local stats. If you missed the webinar, click here to watch it now.

National Stats

Recession Talk

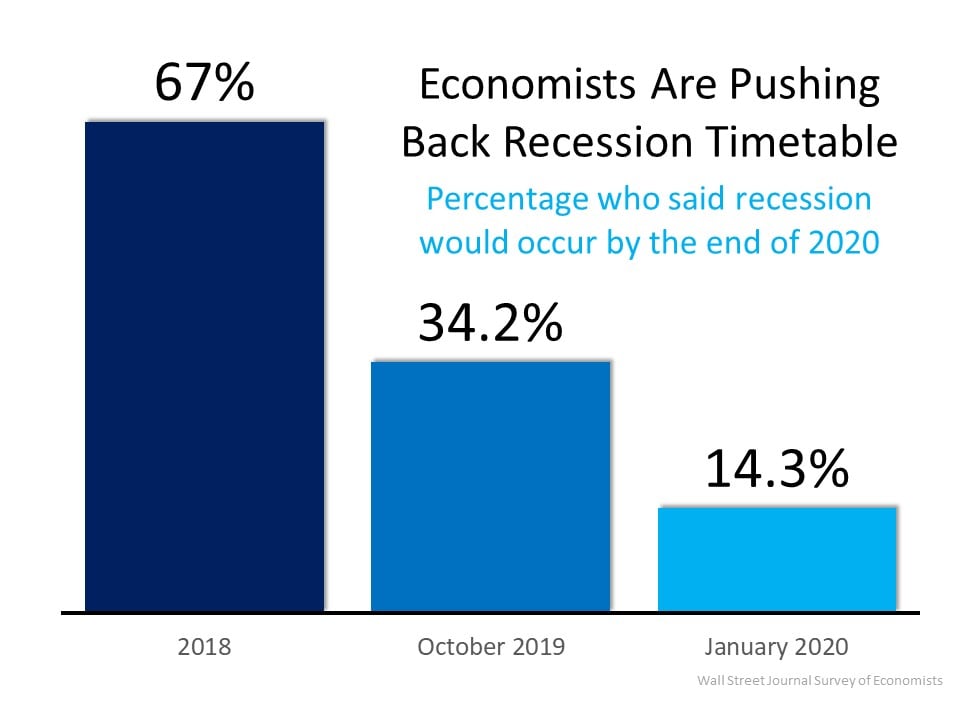

The above graphic reflects the views of economists surveyed by the Wall Street Journal. In 2018, 67% of economists thought that by the end of 2020 there would be a recession. As early as October of 2019, that number was 34.2%. However, in January of 2020, that number was down to 14.3%.The economy seems to be outpacing the expectations of many who are watching a variety of analytics very closely.

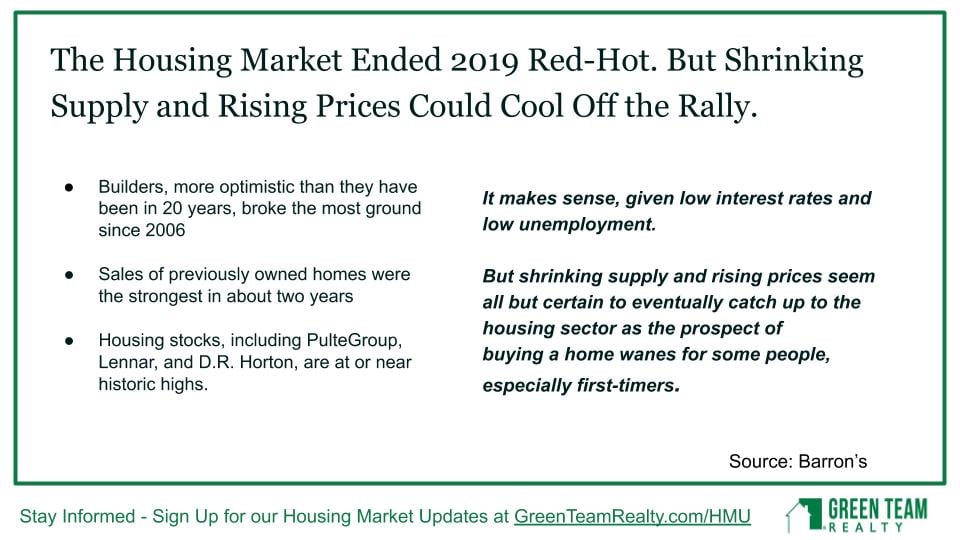

Shrinking supply, rising prices

There is no question that the housing market did end red-hot in 2019.. Prices are continuing to rise, inventory is still low. While builders are more optimistic, they are still not meeting demand. Later, Geoff and David Willner, a home inspector, will be sharing thoughts on why more new construction houses aren’t happening.

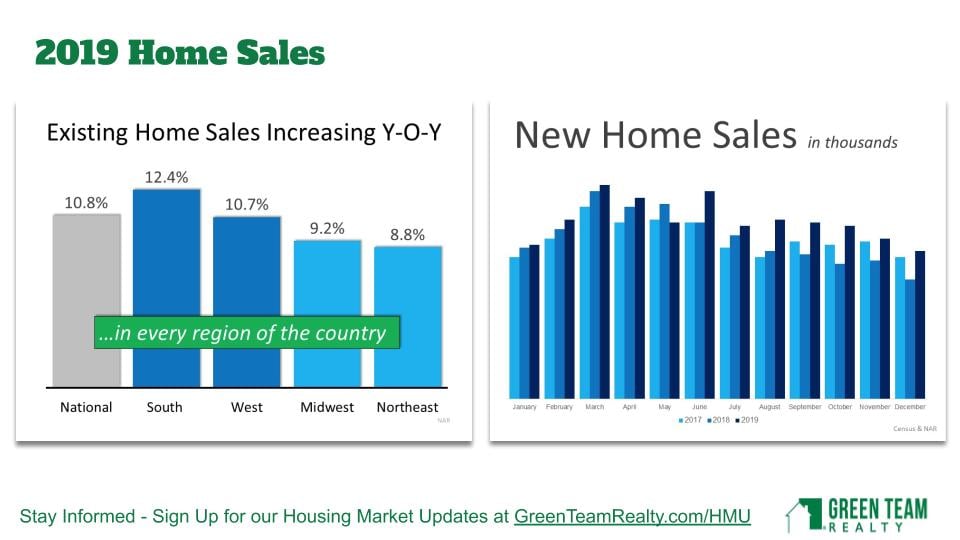

2019 Home Sales in every region

In 2019 existing home sales were increasing year-over-year in every region. There was also an increase in new construction in 2019 over 2017 and 2018. Everything was increasing throughout 2019, and is expected to continue through 2020.

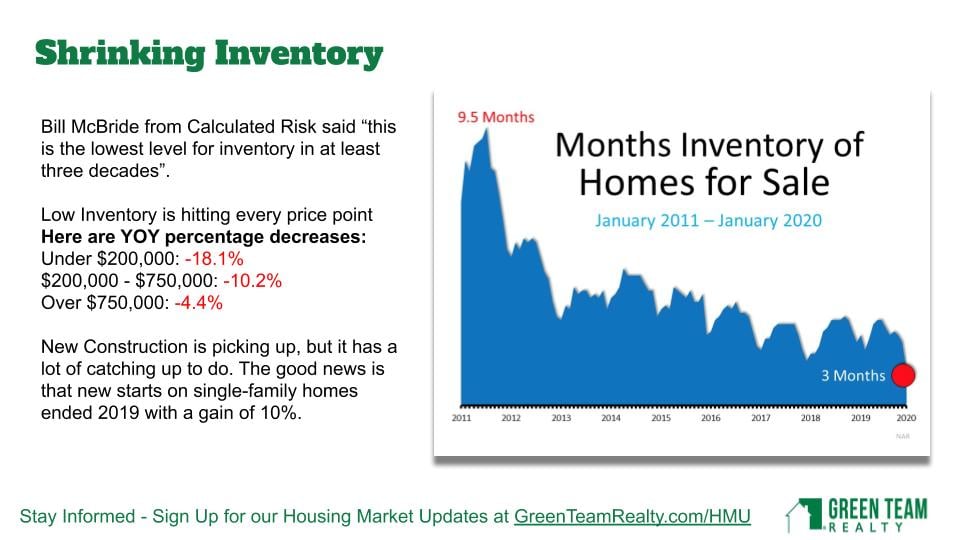

Inventory shrinking

Inventory continues to be a problem. This is the lowest level of inventory in at least three decades. The months inventory of homes for sales is 3 months. A normal market is 6 months. a buyer’s market is 9 months. A seller’s market is below 6 months. There is nothing to indicate that this number will increase. It may actually decrease. The only thing that could possible turn that around would be new construction picking up in big ways. However, it is not that easy to bring new houses online with zoning ordinances, etc.

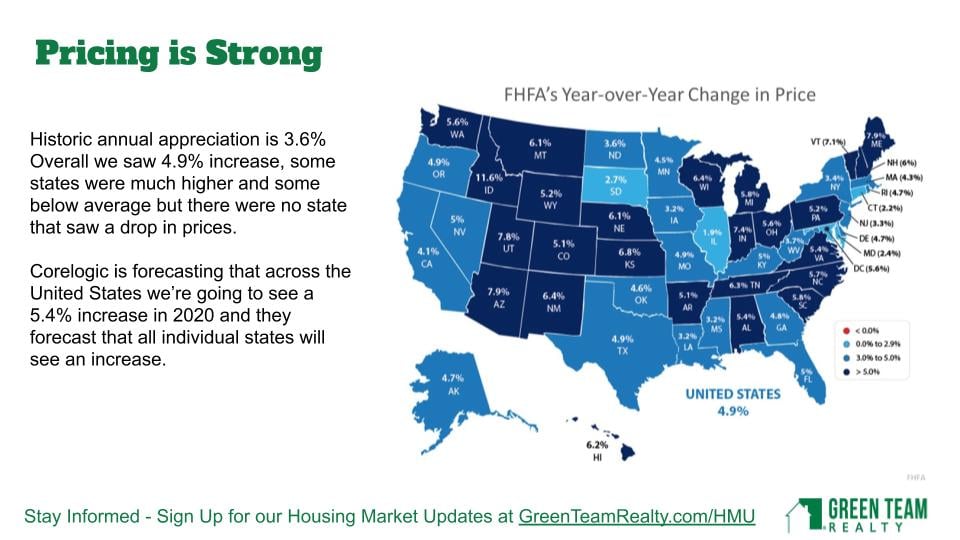

Strong Pricing

Back in the summer of 2018 we started to see different numbers and wondered if the market would rebound. It has rebounded strongly and price increases are anticipated for 2020. Every state is labeled in blue, indicating prices increasing. Corologic and other companies are predicting price appreciation.

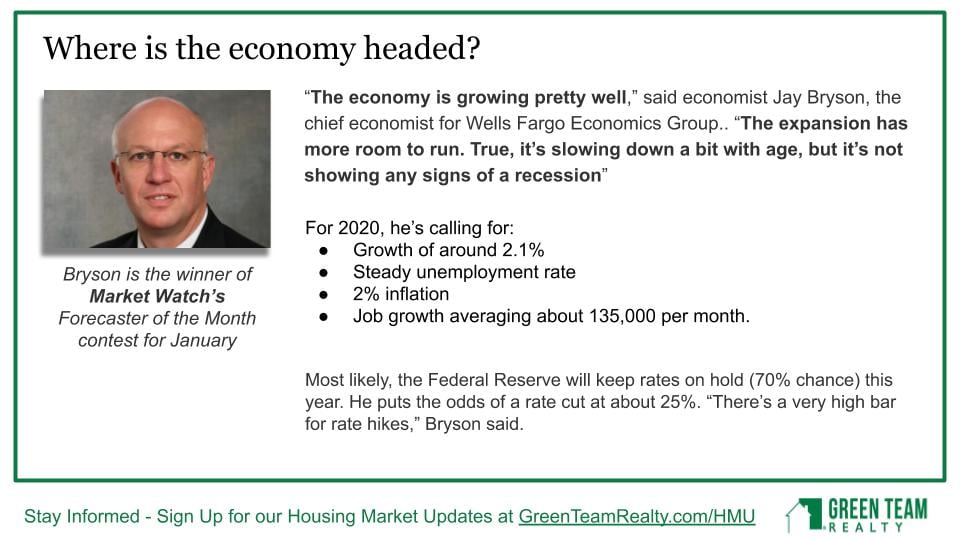

The economy – where is it headed?

According to Jay Bryson, chief economist for Wells Fargo Economics Group, the economy is growing well and the expansion still has room to run. While slowing down a little, the economy is not showing signs of a recession. There is growth of approximately 2.1%. Unemployment rates are steady. We’re at a relatively low rate of inflation. Job growth is good. It does not seem as though anything is poised enough to stop the growth.

Local Stats

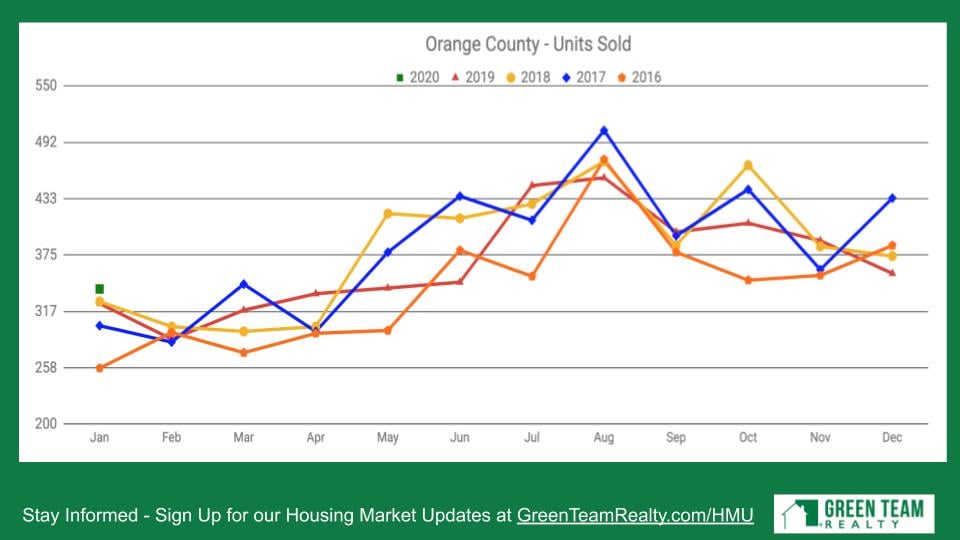

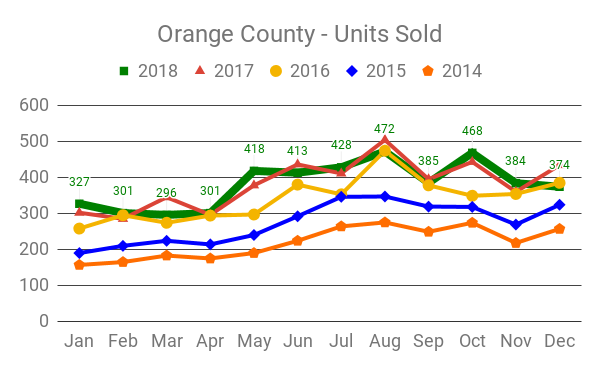

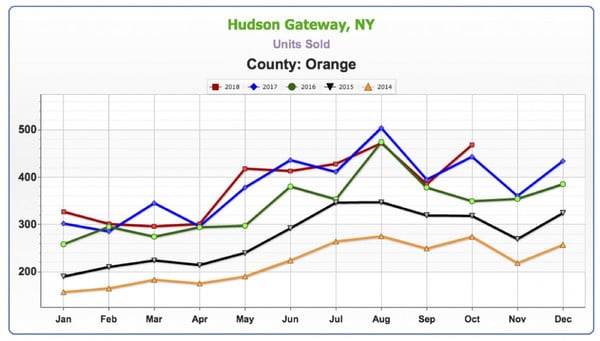

Units Sold

2020 numbers for January show units sold at its highest number in the last five years.

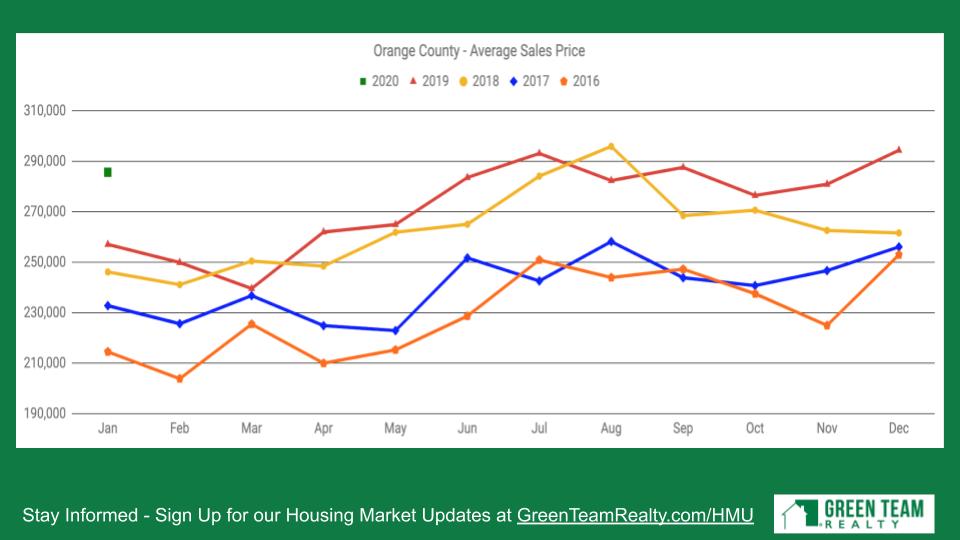

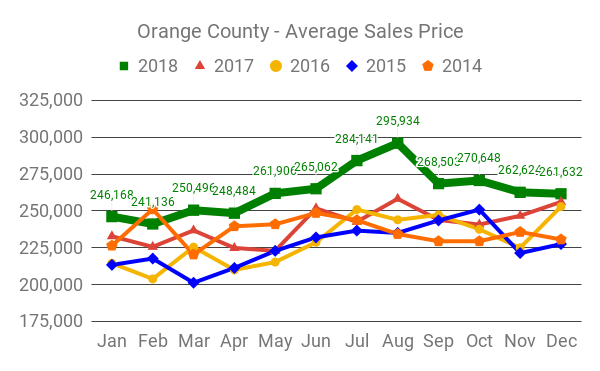

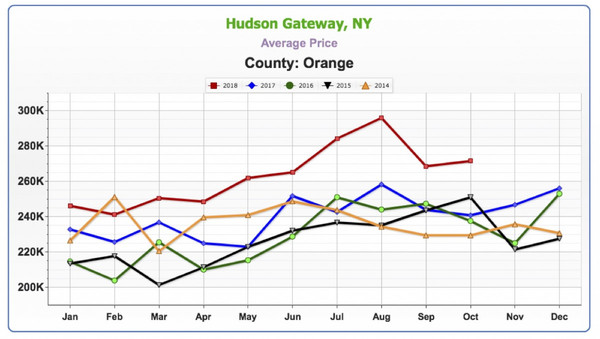

Average Sales Price

Average Sales Price is way up. January is showing a remarkable jump. It will be interesting to see how this plays out the rest of the year.

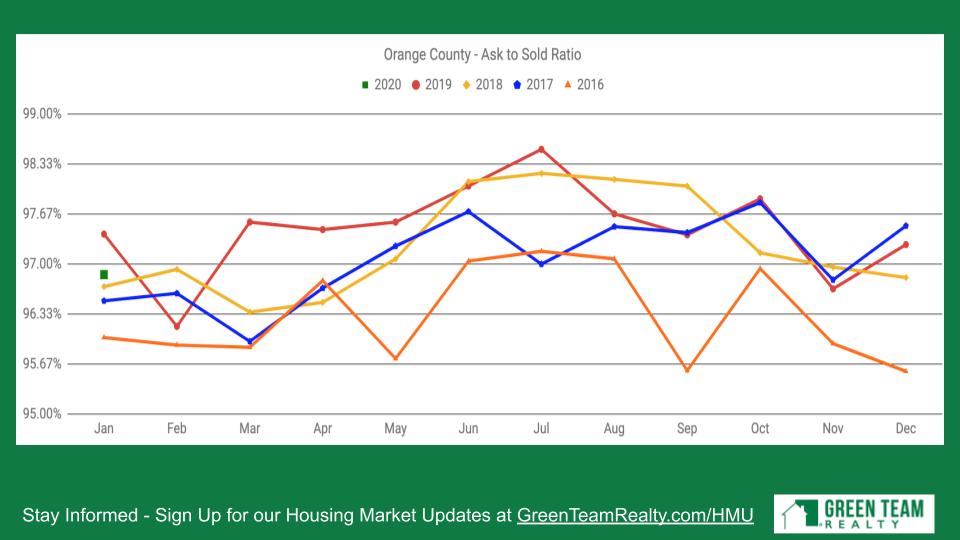

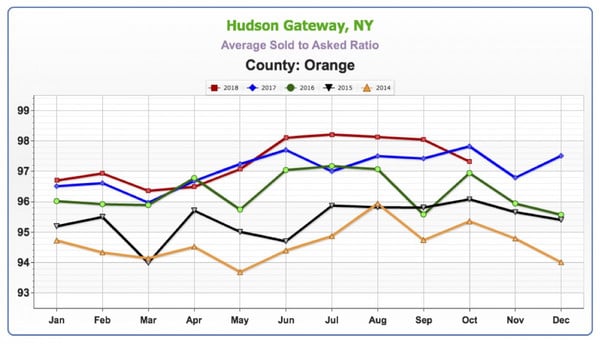

Ask-to-Sold Ratio

This is the last asking price versus what the property sold for. Again, the number is high. Sellers are only having to negotiate about 2% off the asking price. These are strong numbers. And they mean that buyers don’t have too much leverage in this market.

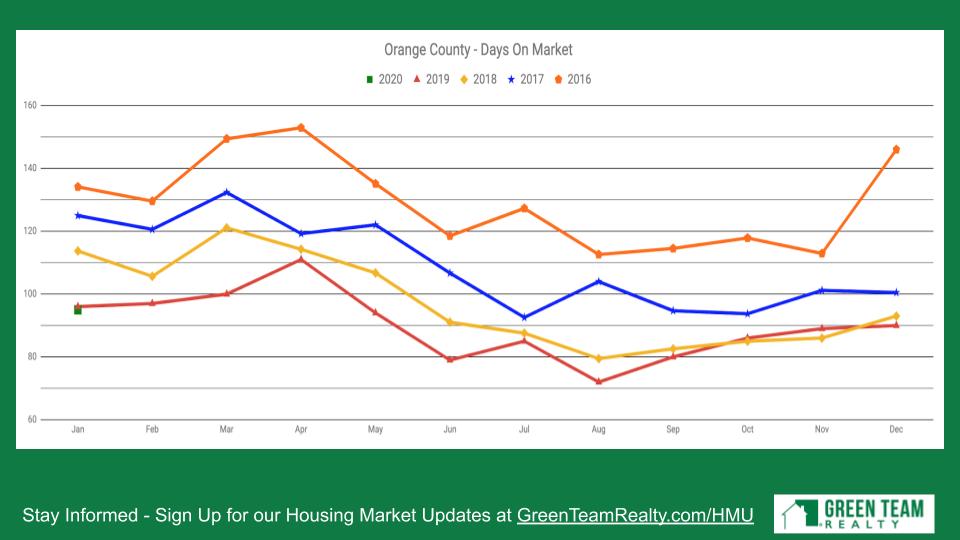

Days on Market

The lower the number of days, the stronger the seller’s market it is. There has been a downward trend, year-over-year, and we’re starting 2020 at the same low mark as 2019. This is a strong number.

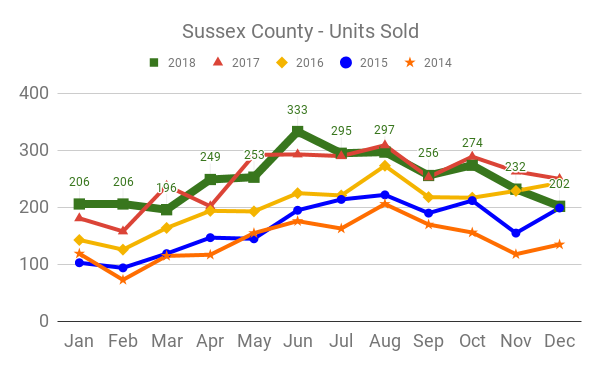

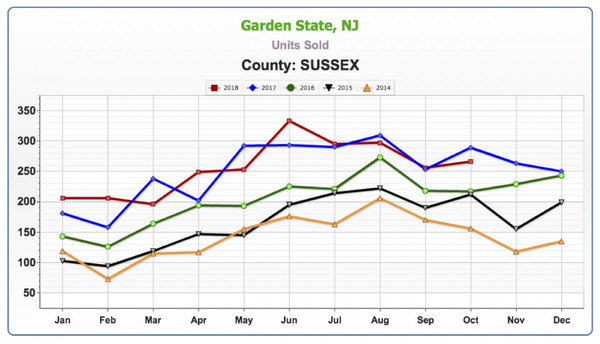

Units Sold

Units sold is same number as 2017. While not starting out at the highest level, it is still a pretty good level for Sussex County.

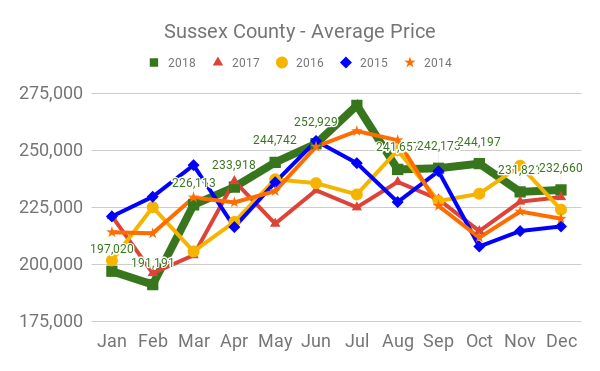

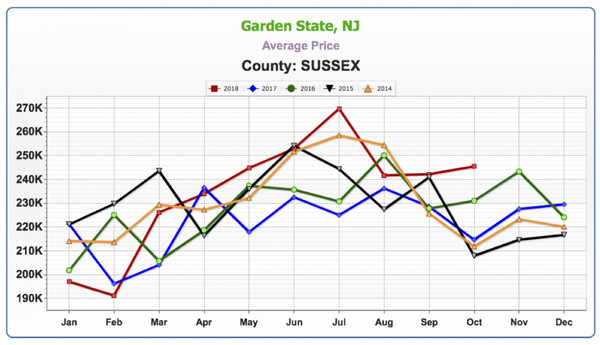

Average Price

Average price is up over the last five years, so that’s a good sign for people looking to sell their homes in Sussex County.

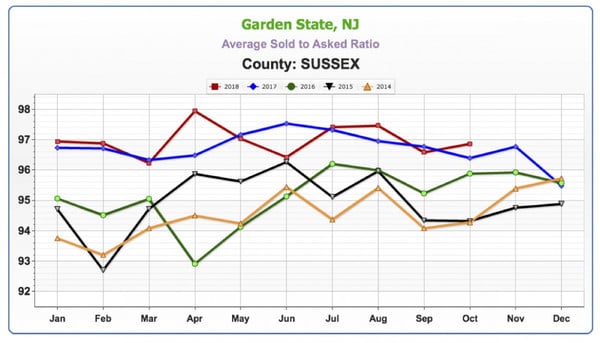

Ask-to-Sold Ratio

This is the last asking price versus what the property sold for. Again, the number is high. Sellers are only having to negotiate about 2% off the asking price. These are strong numbers. And they mean that buyers don’t have too much leverage in this market.

Days on Market

Again, this is the lowest level in five years in Sussex County. Things are going quickly.

Housekeeping Items

Join us for the next Housing Market Update, Tuesday March 17 (St. Patrick’s Day) at 2 p.m. Stay informed. Sign up for our Housing Market Updates at: GreenTeamRealty.com/HMU.

Thanks to our sponsor, REALLY, the Real Estate Referral Community. REALLY is where Professionals who serve the Real Estate Industry can connect, communicate, and securely exchange referrals with speed and ease. The best part? No fees on commissions exchanged between Agents. Join for free at ReallyHQ.com

Geoff introduced Dave Willner and began the discussion with:

Do you foresee anything slowing down the 2020 housing market?

The simple answer was “No!” Dave believes that 2020 is going to be a big year. January started off with a big bang. In January 2020 his company reported its highest earnings in three years. The number of inspections are up. They are seeing a niche in the under $500,000 market. Higher-end homes are not moving as quickly as those selling for $500,000 or less.

Geoff agreed that is definitely true for our area. While in some places, such as New York City and certain areas on the West Coast, $500,000 wouldn’t even buy a “fixer-upper.” Dave said that it definitely depends on the market, but that is what they’re finding here. Geoff also agreed that he doesn’t see anything to indicate that 2020 won’t be a big year. However, he does think that there are some interesting things happening economically on a macro scale that everyone should be aware of.

Economics – the Macro and the Micro

How might the coronavirus on the granular level, impact economics? Geoff shared some of the things he’s learned.

In addition to the coronavirus, there is something happening regarding travel. The Boeing 737 Max was grounded last year. That has had a major impact on the airline industry, which further impacts overall travel spending. There is a “double whammy” happening within the travel industry. Further, travel is a significant segment of the U.S. economy; not something to be dismissed. A micro example would be Corning in Upstate New York. A lot of their revenue is received from people traveling from New York City up to Niagara Falls. As it’s a midway point, a lot of international travelers go to the Corning plant to see how glass is manufactured. So many people have traveled there from China that they have tours in Mandarin. Thus, the coronavirus and the Boeing 737 Max have impacted this local economy.

As real estate is local, there could be a locally impacted market while the nation is booming. Those in travel-related economies should keep an eye on these developments. Dave asked if vacation housing in Orange and Sullivan Counties might be affected as a result of these issues. For example, would more people seek a summer retreat? Geoff didn’t think that market would be especially impacted, since much of the tourism in the area is people traveling from other countries. Second homes are more for people in the NYC/metro area who want to get away for a weekend. He doesn’t necessarily see the coronavirus as impacting that end of the travel spectrum. However, the idea is not to be dismissed. It’s an interesting dynamic to keep an eye on.

The Coronavirus and the Impact of Quarantines

Another aspect of the coronavirus is quarantine. China is literally quarantining cities, shutting down transportation, etc. Not only can people not leave their city. They can’t travel. But many also cannot go to work. Stores are being closed, factories shut down and unable to operate. You are now seeing headlines about Apple revising its earnings. They’re saying the supply chain is being affected because much of their manufacturing is done in China. Not only is demand being impacted by the economy in China, which has been affected by the virus. The supply chain is being impacted as well in terms of production. Further, you have to think about commodities. If factories are not running, you don’t need iron, heavy metals. Commodity prices, such as oil, are dropping.

Globally a lot of things are happening now that many people seem to overlook. Right now, things are good in the United States. However, globally many economies have not been doing so well for the last few years. Hopefully the coronavirus will have reached its peak and begin to dissipate.

The Presidential Election

It will be interesting to see what evolves in this election year. There are candidates who are at the opposite economic spectrum of the Trump administration. And if elected, what would the impact be? It would probably not affect 2020 as the election is not till November. However, needless to say, it’s an issue that should not be dismissed.

Trade agreements with Canada and Mexico and China will also impact the economy. Again, it will be interesting to see the impact of global factors.

Keren Gonen joins the conversation

Keren Gonen of Green Team New Jersey Realty joined the panel discussion. Having just arrived from a closing, Geoff filled Keren in on what had been discussed regarding the 2020 market stats. He asked if she agreed with their prediction that 2020 would be a big year. Geoff also talked about inventory pressure and problems. Then he asked what she is seeing now. Keren stated that she’s seeing the same things, and that Spring Market has already started. She’s as busy now as she should be at the end of April. This month alone she has 3 closings. And she’s projecting another 5 closings for next month.

Geoff said that the mild winter might also be a factor. Many people just don’t want to go out and look at homes when it’s raining, snowing, etc. While it has been cold, there has not been a lot of snow to deal with, which helped catapult things. More importantly, interest rates are really low. And that is something that can help offset the high price of homes for some buyers. While the price may be on the high end, it’s what fits the monthly budget that really counts. If that low rate can be locked in buyers can set themselves up for success as home owners.

Wrapping it up

Geoff asked Dave and Keren if they could think of anything that might stop this market from churning as fast as they think it’s going to in 2020. Dave replied it’s about managing the inventory out there. It is definitely a limited-inventory market, and the good deals have been had. Dave has seen a strong influx of people coming up to more rural communities from the city. That’s where many of the buyers are coming from, looking to get out of renter-ship. As long as interest rates stay low, people will continue to buy.

According to Geoff, the Fed is in a holding pattern, neither raising or lowering the federal funds rate that they use to manipulate the economy. It’s interesting that in the last 10-15 years that lever they had, that once meant so much, has little meaning now. Needless to say, it looks like the Fed will hold in place, which just provides more information to consider.

Home Ownership vs. Renting

Keren added that there are plenty of people renting, even in Sussex County, that could actually afford to be home owners. They would pay less for a mortgage than they pay for rent right now. That’s something important to remember. A lot of renters don’t realize they can afford to be homeowners, so they should get in touch with a mortgage broker to see what their options are. In our area, you can pay $800 in a mortgage payment opposed to $1,200 in rent. It’s important to educate people as to what their options are.

Geoff agreed, saying that many people got caught in the downturn of the market 10 or 12 years ago.To them he says, don’t be afraid. Research. Talk to a mortgage professional to see if your income and credit is where it needs to be, and get in the game. Banks who have been renting homes are starting to sell those homes, leaving renters in the lurch. They can’t find other rentals and are in a bad spot. It’s in their best interest to own a home.

Dave remarked that there has been more of a trend for FHA loans. They are no money down essentially. There are lots of options available. Geoff stated that another great thing for this recovery is that you are not seeing a lot of sub-prime lending. That means this recovery is true.

Contact the panelists

Dave Willner, Pillar to Post Home Inspection, 732-647-5231 or email dave.willner@pillartopost

Keren Gonen, Call or text 551-262-4062

Join us at 2 p.m. on St. Paddy’s day for our next Housing Market Update.

Headlines spotlight the fact that buying a home is less affordable today than it was at any other time in more than a decade. Those headlines are accurate.

Understandably, buying a home is more expensive now than immediately following one of the worst housing crashes in American history. Over the past decade, the market was flooded with distressed properties (foreclosures and short sales) selling at 10-50% discounts. There were so many that this lowered the prices of non-distressed homes in the same neighborhoods. As a result, mortgage rates were kept low to help the economy.

Prices have since recovered. Mortgage rates have increased as the economy has gained strength. This has impacted housing affordability. However, it’s necessary to give historical context to the subject of affordability.

Two weeks ago, CoreLogicreported on what they call the “typical mortgage payment”. As they explain:

“One way to measure the impact of inflation, mortgage rates and home prices on affordability over time is to use what we call the ‘typical mortgage payment.’ It’s a mortgage-rate-adjusted monthly payment based on each month’s U.S. median home sale price. It is calculated using Freddie Mac’s average rate on a 30-year fixed-rate mortgage with a 20 percent down payment…

The typical mortgage payment is a good proxy for affordability because it shows the monthly amount that a borrower would have to qualify for to get a mortgage to buy the median-priced U.S. home…

When adjusted for inflation, the typical mortgage payment puts homebuyers’ current costs in the proper historical context.”

Here is a graph showing the results of CoreLogic’s research:

As the graph indicates, the most recent calculation remained 28% below the all-time peak of $1,275 in June 2006. That’s because the average mortgage rate at that time was 6.68%. As seen in the graph, both today’s typical payment and CoreLogic’s projection for the end of the year are less than it was in January 2000.

Bottom Line

Even though home prices are appreciating at a slower rate, home affordability will likely continue to slide. However, this does not mean that buying a house is an unattainable goal in most markets. It is still less expensive today than it was prior to the housing bubble and crash.

Get local housing market updates – sign up to receive the Green Team’s Housing Market Update Report.

The Green Team’s January 2019 Housing Market Update was held on Facebook Live Tuesday, January 15 at 2 p.m. If were unable to view the webinar live, you can watch it at your convenience here. You can also sign up for future updates at GreenTeamHQ.com/hmu.

This month’s panelists…

Geoffrey Green, President/Broker of Green Team Realty, moderates the monthly webinars. He also presents national statistics, together with local updates for Orange County, NY and Sussex County, NJ. This month he is joined by Carol Buchanan of Green Team New York Realty, Keren Gonen of Green Team New Jersey Realty and Patrick “PJ” Keelin of Family First Funding.

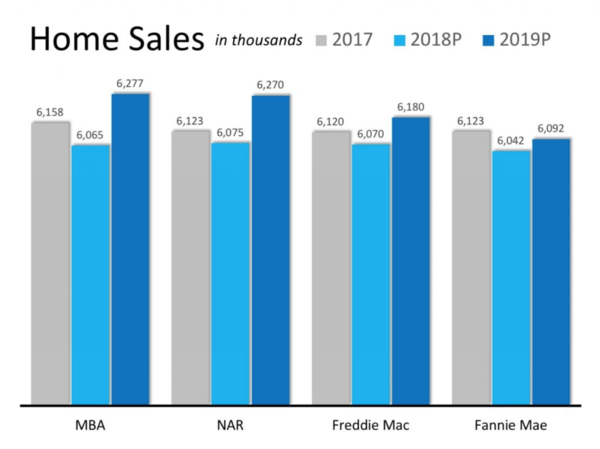

The National Outlook

The above charts are raw numbers – the number of homes that were sold from 2014-2018. It appears that things are softening a bit, but it doesn’t appear that it will be drastic.

The analytic showing inventory levels is important. It has been difficult to find homes for buyers over the last few years. However, it appears that inventory levels may be coming back a bit. Lower demand should yield more inventory, but hopefully what some inventory may do is bring some people back into the game who may have been been frustrated previously.

This survey of experts, market analysts, etc. addressed the question, “What Will Home Prices Do in 2019?” 100 people were surveyed and 94% projected that housing prices on a national basis will continue to appreciate. Geoff aligns himself with that 94%. He believes that in 2019 prices will come up again in spite of the fact that activity went down. Price always lags activity.

According to Geoff, this quote from Goldman Sachs is a good one. “Despite the headwinds facing the housing market going into 2019, we expect U.S. house prices to generally achieve a soft landing. We expect national average price appreciation to remain positive.” If this comes true, it’s music to Geoff’s ears. He lived and worked through the last downturn, where 50% of the number of homes that sold went away within a 2-year period of time once the market starting declining. It was a difficult time

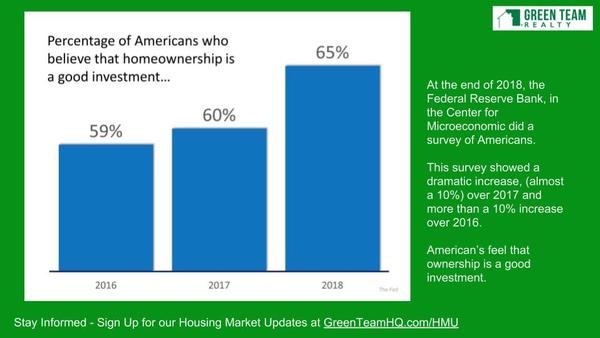

The percentage of Americans who believe homeownership is a good investment continues to increase. The market is at a peak and confidence continues to increase. However, Geoff finds that people tend to buy high and sell low. They should be buying low and selling high. The bottom of the market, 2011, 2012, and 2013 would have been a good time for investment.

However, people are confident that it’s a good time to buy now. And one thing that will never change is that homeownership is a good thing.

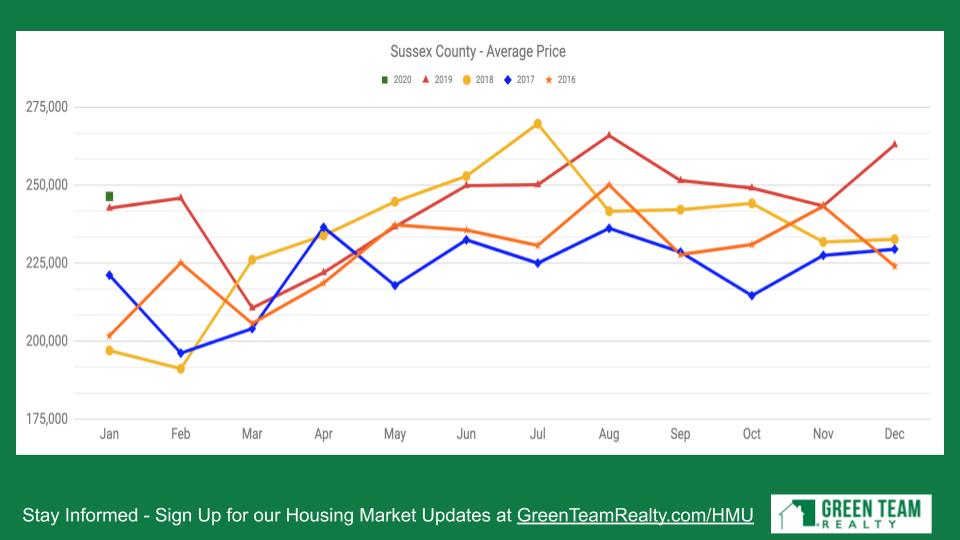

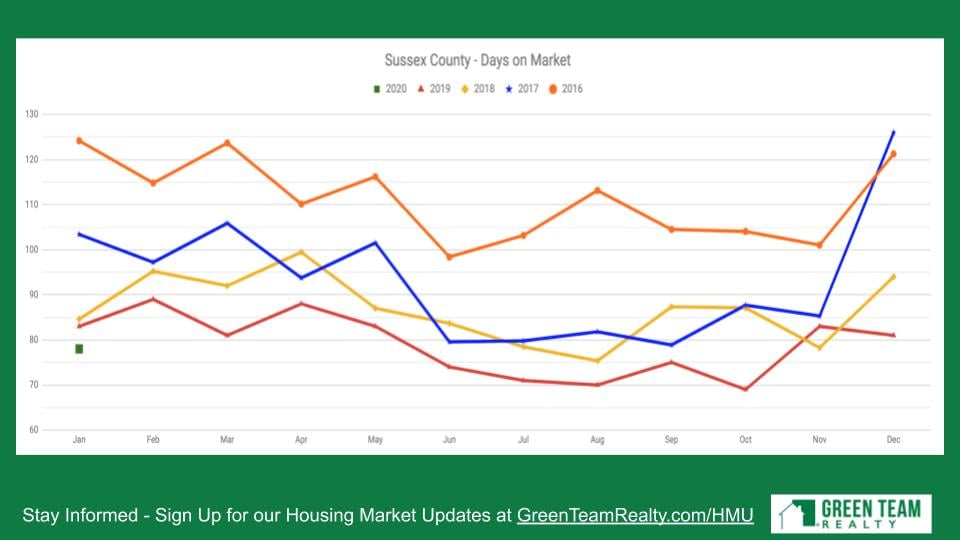

January 2019 Local Housing Market Update for Orange and Sussex Counties

Units Sold

Five year look back. The thick green line is 2018 and while it’s been a mixed bag throughout the year, we ended up just a tad bit lower than the past two years.

In Sussex County, Units Sold was also a mixed bag, with one of the lowest totals in almost 4 years.

Average Price

In Orange County, prices were up substantially for a good part of the year. However, there was a cooling-off period towards the end of the year.

Sussex County never saw as much of an appreciation as Orange County did. However, 2018 was still a leading year over the past 5 years.

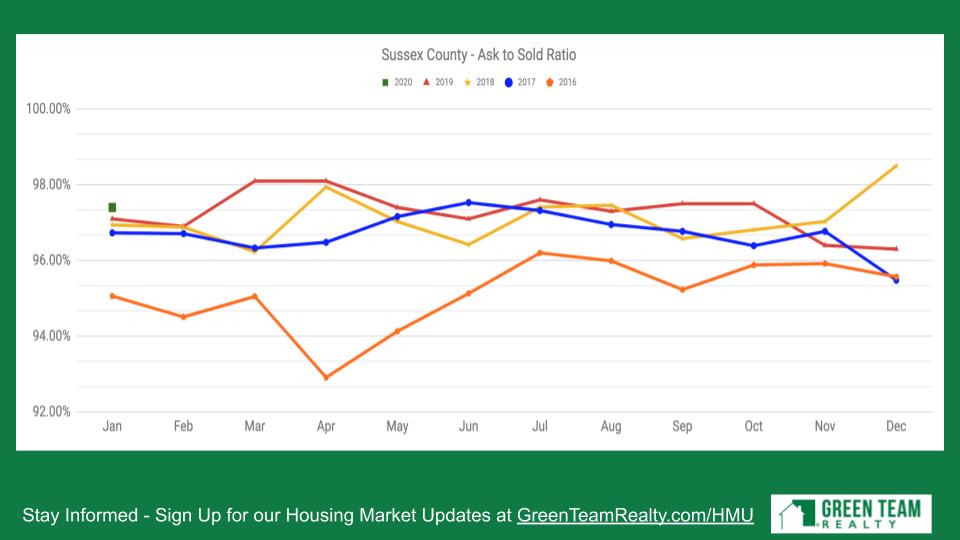

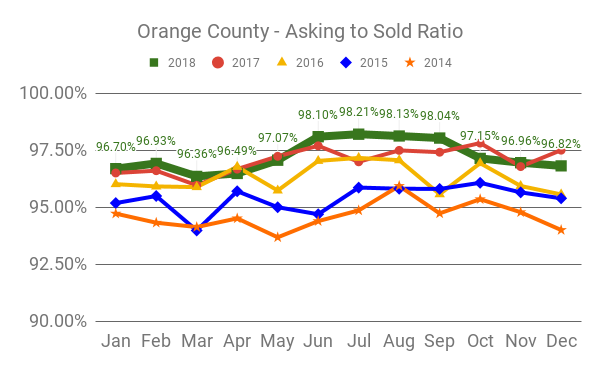

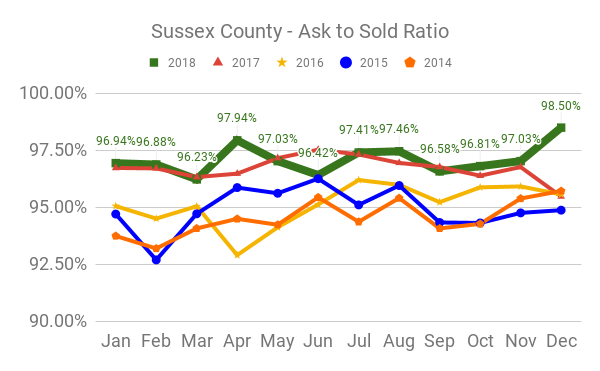

Asking to Sold Ratio

What price do homes on average sell for versus the last asking price? The higher towards 100% the hotter the market. The numbers have been strong for Orange County throughout the year.

Sussex County was strong in this category throughout the year. However, it hit its highest point in December 2018 with a ratio of 98.50%.

Panel Discussion

Geoff asked Carol Buchanan and Keren Gonen what they think of the market, as it appears a softening is underway. Carol stated that inventory is still low, and January and February are common months for the market to slow down. Carol does believe that 2019 is going to be a very good year. People seem undaunted by higher interest rates. Still a lot of buyers; just not enough homes.

Keren also agrees that 2019 will be a very good year. She thinks that people will start listing homes for sale within the next few months. Right now buyers are looking but there is still not enough inventory. She feels there are sellers sitting on the fence, not sure what to do and just holding out for a few more weeks or months. Geoff commented that the bread and butter of the season is March through August. So it’s natural for many homeowners to wait until March to list their homes.

Talking with Keren regarding foreclosure activity, Geoff asked if she see a decline? Banks are fixing up houses and putting them up at market prices. If the quality of work was good, that would be fine. However banks are bidding jobs out and the resulting work is not necessarily good work. Buyers expect to see good quality and are disappointed with what they’re finding. They often would prefer to pay more for a house that is in good shape. Therefore, many of these homes being sold by the banks are just sitting on the market. Banks are now competing with flippers who, generally speaking, do a better job at fixing up homes than the contractors. Buyers most often prefer paying full price for a home that was “flipped” well than on an REO that was not done well.

Geoff mentioned that this was not the trend in the past. Banks would not fix up their properties and try to sell them for more money. They’d just try to unload them at lower prices and buyers could get a good deal. Over the course of time we’ll see if banks decide to go back to the way they used to handle foreclosures.

Regarding the financing environment, Geoff asked Patrick “PJ” Keelin what we’re looking at for 2019. As Geoff put it, at the end of the day we’re really in the land of the banks, dependent on what they’re willing to do. And how many times the Federal government is willing to let banks leverage their money. PJ indicated that on a global scale, at the end of the year there was talk of the Feds raising the interest rate. That usually indicates a stronger economy; stronger aspects coming from the financing angle and mortgage-backed securities, etc. Unfortunately, at the end of the year there was a huge difference and the Dow dropped significantly. The drop in the Dow affected reports of things they were coming out with. So trends and thoughts of increased interest rates by the end of the year through that New Year boom fizzled out. There are reports that there is potentially going to be a decrease in interest rate for the year 2019. PJ believes that is something being put out there for a little bit of hope.

However, the biggest thing we’re competing with is the lack of inventory and what people will be able to purchase. Looking at an average household income of $60,000 to $70,000, that probably puts a person on average of what they can afford in terms of a property at $1,500 to $1,600 range. That gives them a certain price point that they have to stay in, and with increases in interest rates that is going to affect their eligibility to be able to purchase properties within a certain price range.

Geoff stated that all signs point to Fed raising interest rates. He asked PJ if he thinks that won’t be the case in 2019. PJ replied that there will be a lot less than they were expecting in 2018. They may skip the first interest rate rise. Hopes on the industry side are that there will be a potential interest rate drop. That may push that boom for people who are still sitting on the edge. He sees a stronger trend with the amount of people who are actually motivated in purchasing. They may finally be believing the reports that interest rates are not going to stay historically low and will go up. So many reports are going in different directions that it’s unsure what to make of it. Industry leaders are saying the market is staying relatively steady, but be prepared. There could be a drastic change.

Right the now trend is slow and steady. PJ commented that Geoff is proactive in all that he does; communicating with his sales associates and with the lenders they work with. Because ultimately these transactions need to happen quickly in order for them happen. When they remain open, bigger changes are coming.

Geoff wrapped up, saying that at the end of the day, interest rates are impacted by bond markets. As long as there is no major economic collapse, the housing market should be fine. He predicts a good 2019. PJ agrees, that it will be a good, strong year. People are getting more motivated.

Join us for the next Market Update

The next Housing Market Update will be held on Tuesday, February 12 at 2 p.m., when the Green Team will again be going live on Facebook. Sign up for updates at Greenteamhq.com/hmu.

The Green Team’s November 2018 Housing Market Update was held live on Facebook Tuesday, November 13 at 2 p.m. If you missed the live webinar, you can view it at your convenience by clicking here.

Geoffrey Green , President/Broker of Green Team Home Selling System, moderates the monthly webinar and presents the national stats, as well as the market updates for Orange and Sussex Counties. This month he is joined by Pam Zachowski and Keren Goren of Green Team New Jersey Realty and Vikki Garby, Green Team Home Selling System, Warwick.

Joe Moschella, Branch Manager and Vice President of Lending, and Amy Green, Vice President of Lending, of Guaranteed Rate discuss market updates from a mortgage industry perspective.

The National Outlook

According to Geoff Green, it’s a very exciting time in the housing market right now as we’re starting to see some shifts. We’re experiencing all-time highs reminiscent of 2008 over the last 18 months. It does seem like things are cooling off. According to Michael Fratantoni, Chief Economist of the Mortgage Bankers Association, he expects that home sales growth will pick up again over the next year, even with somewhat higher mortgage rates, though the pace of price growth will likely slow.

Despite the fact that national and local numbers indicate that the velocity of homes selling is actually slowing, Fratantoni and some others are predicting that it is going to increase in 2018. So, it’s not that appreciation is going down, it’s just slowing down.

The Mortgage Bankers Association, National Association of Realtors, and Freddie Mac, with the exception of Fannie Mae, all are predicting increases over the past two years. All are predicting increases over the past year. For the most part each of these organizations wants the housing market to continue to grow. Geoff reminds us that it’s in their best interest. It’s important to be aware of the source of information. During the downturn In 2006, 2007 and 2008, during the downturn, some organizations were putting out information that did not accurately portray what was happening. However, you can rely on the Green Team to put out information that is accurate and honest.

In projections for 2018 through 2022, everyone seems to have a positive outlook that the market will continue to appreciate. Just at a slower pace.

November 2018 Housing Market Update – Orange County

Units Sold

While this is hyper local, it is reflective of the 2018 national numbers. While prices may increase and decrease, depending on inventory, units sold have been a mixed bag this year versus last year. It’s been up, it’s been down.

Average Price

Geoff has found that price always lags activity, according to his observations over the past 14 years. If you start to see a slowdown in activity, 6 to 8 months later you’ll start to see a slowdown in the rate of price increases.

Sold to Asked Ratio

This is telling you at what percent of the asking price your home is selling for. The closer you are to 100%, the hotter the market. While this took a little dip recently, it is still at very high levels.

November 2018 Housing Market Update – Sussex County

Units Sold

This is a small data sample that is still reflective of what is happening nationally. Again, it’s a mixed bag, up, down, then often flat.

Average Price

Average price never really gained a tremendous amount of traction, as compared to Orange County, where there had been increases in price.

Sold to Asked Ratio

This looks similar to what is happening in Orange County.

Panel Discussion

The Sales Associates Points of View

Geoff asked Vikki what changes she’s seen since she was last on the panel about 4 months ago… Vikki agreed that she has been seeing a little bit of a slowdown, part of which she believes is due to timing. Many families time their house hunting to coincide with the start of school. However, what she’s finding is a lot of people are looking for land. Historically, we’ve had low inventory compared to the number of buyers, And, as existing house prices go up, more people are starting to consider new construction. Housing starts will be up 9% beginning of the coming year. So there is still a lack of inventory.

Pam also sees a slowdown. More people are looking for homes, but between the low inventory, the start of the school year, people are taking their time. She still sees investors trying to buy and flip homes but finding it harder and harder to find that good deal that makes it worthwhile.

Geoff then asked about appraisals. Are there issues with properties appraising, or are there now enough comps in the marketplace? Keren has not seen any problems recently. They’re all coming in at asking and a little bit above. One thing she has noticed is Sellers asking for CMA’s or listing presentations, more than she had over the summer. Keren always advises clients that we only know what the market is right now and can’t tell where it’s going. She lets them know that low inventory makes it a good time to put their home on the market, as opposed to waiting for Spring, Geoff replied that sellers that were holding off putting their home on the market may now decide to take a chance, seeing that the market is cooling off a little. This may ultimately bring more inventory and more transactions to the marketplace as a whole. There are still many buyers out there, anxious to find a home.

A Mortgage Industry Point of View

According to Joe Moschella, over the last 5 months they’ve seen a steady rise in interest rates. The year started with a 10-year treasury note at 2.21% and this week it was 3.21%, one full percent. That, along with the Fed stopping its purchasing of mortgage-backed securities, caused a liquidity crunch in the market. This contributed to pushing rates up. They started the year with 4% on a 30-year fixed rate and are now closing in on 5%.

Geoff asked Joe what the bond market was like 4 years ago on a percentage basis, just to give some perspective. Joe brings it back to 9/11, when the Fed didn’t want to see the economy spiral down. They jumped in and started dramatically dropping rates, bringing them down to almost zero. Now we’re seeing the unwinding of these artificially low rates. Thankfully the Fed eased into this, providing a “soft landing.” 2.21 to 3.2% represented about ¾ of a percent, interest rate wise. About 2, 2-1/2 years ago we were at 1.2% on the US Treasury. Before that, we were at the 0.7, 0.8% range. We’ve seen a steady rise, which hopefully the economy is strong enough to handle.

Some of the other changes in the market on the mortgage front are in the role technology is playing. Lenders are able to verify client’s income and assets automatically, do the application online and do the process without sending any paperwork back and forth. The whole process is done digitally.This is revolutionizing the industry and leading to higher consumer satisfaction. The industry is also easing credit standards. Geoff asked if easing credit standards was necessarily a good thing. Joe responded that rising rates have opened the door for new loan products to come out. Those new products are not coming from the banks, but rather from private equity firms flowing back into the market. No verification loans do not exist, but they have a bank statement loan that has come back into play. No seasoning waiting period for someone who had a foreclosure or bankruptcy or short sale, whereas before you had to wait three, four or seven years. Geoff stated that if you’re talking about private equity, they basically can do whatever they want with their money, as long as those products don’t make it into mortgage-backed securities. He asked if there were any controls in place to make sure that didn’t happen again. The trade-off with non-conforming products is that the buyer has to have some “skin in the game.” They need a sizeable down payment, and investors want higher return for higher risk, so rates may be at the 6-1/2% range.

Geoff said it’s important to keep things in perspective. The sky won’t be falling if rates hit 6-1/2%! Historically, it’s a pretty average rate.

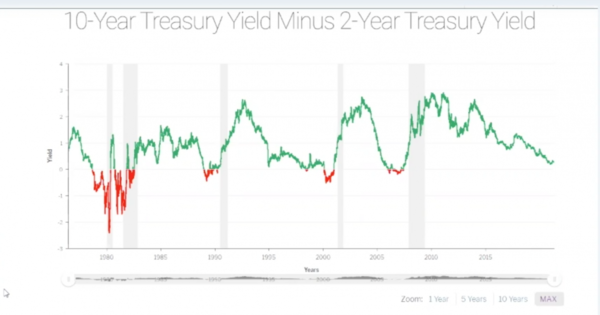

Joe and Amy had a graph showing 10-year treasury yield minus 2-year treasury yield. Historically when those yields come together, it signals a slowdown in the market or a recession. From Joe’s perspective, we might have a slow down in the stock market and see a pull back, but he’d rather see a market that goes up and goes down. In a stale market buyers and sellers are sitting on the fence; there is no call to action. As far as housing goes, everyone can do well and make some money.

Geoff thinks there is enough pent up demand from 2008 to 2016; there are a lot of people who need to buy a home and rates are still low enough. The American housing market is the place to be in the Global real estate market. There may be a continued cooling off and slow down a little. We’ve been at such high levels right now, it had to. Like the stock market, it can’t keep going up indefinitely; at some point it has to come down.

For the last several years, buyer demand has far exceeded the housing supply available for sale. This low supply and high demand have led to home prices appreciating by an average of 6.2% annually since 2012.

With this being said, three of the four major reports used to measure buyer activity has revealed that purchasing demand may be softening. Here are the four indices, how they measure demand (methodology), what their latest reports said, and a quick synopsis of the report.

Methodology: Every month SentriLock, LLC provides NAR Research with data on the number of properties shown by a REALTOR®. Lockboxes made by SentriLock, LLC are used in roughly a third of home showings across the nation. Foot traffic has a strong correlation with future contracts and home sales, so it can be viewed as a peek ahead at sales trends two to three months into the future.

Latest Report: “Foot Traffic climbed 3.2 points to 55.8 mid-summer in July. Additionally, the diffusion index is higher than last year by 13.5 points. Despite a healthy economy and labor market, supply and new construction remains unable to keep up with buyer demand.”

Methodology: The ShowingTime Showing Index® tracks the average number of buyer showings on active residential properties on a monthly basis, a highly reliable leading indicator of current and future demand trends.

Latest Report: “Showing activity throughout the country increased by 0.3 percent year over year in July, the third consecutive month that the U.S. ShowingTime Showing Index recorded buyer interest deceleration compared to the previous year. The June 2018 figures revealed a 0.0 percent change in showing traffic from 2017, while May showed a 1.2 percent year-over-year increase. The 12-month average year-over-year increase was 4.6 percent.”

Methodology: The REALTORS Confidence Index is a key indicator of housing market strength based on a monthly survey sent to over 50,000 real estate practitioners. Practitioners are asked about their expectations for home sales, prices and market conditions.

Latest Report: “REALTORS reported slower homebuying activity in July 2018…The REALTORS® Buyer Traffic Index registered at 62, down from the same month one year ago (69). This is the fifth straight month (since March 2018) that Realtors reported a decline in buyer activity compared to conditions one year ago.”

Methodology: Proprietary survey results of real estate executives.

Latest Report: “While we continue to expect a resumption of growth in resale transactions on the back of easing inventory in 2019 and 2020, our real-time view into the market through our Real Estate Broker Survey does suggest that buyers have grown more discerning of late and a level of “pause” has taken hold in many large housing markets. Indicative of this, our broker contacts rated buyer demand at 69 on a 0-100 scale, still above average but down from 74 last year and representing the largest year-over-year decline in the two-year history of our survey.”

Synopsis: Buyer demand is softening

Bottom Line

Again, three of the four most reliable measures of buyer activity are reporting that demand is softening. We had a strong buyers’ market directly after the housing crash which was immediately followed by a strong sellers’ market over the last six years.

If demand continues to soften and supply begins to grow (as is projected to happen), we will return to a more neutral market which will favor neither buyers nor sellers. This “more normal” market will be better for real estate in the long term.

Want to know what your home is worth? Get a quick and free home valuation report – Click Here

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

![Americans See Major Home Equity Gains [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/03/18144837/20210319-MEM-1046x1558.png)