Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Is Buying a Home Today a Good Financial Move?

[et_pb_section fb_built=”1″ admin_label=”section” _builder_version=”3.0.47″ custom_padding=”22px|0px|0px|0px|false|false”][et_pb_row custom_padding=”13px|0px|32px|0px|false|false” admin_label=”row” _builder_version=”3.0.48″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text admin_label=”Text” _builder_version=”3.0.74″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]There’s no doubt 2020 has been a challenging year. A global pandemic coupled with an economic recession has caused heartache for many. However, it has also prompted more Americans to reconsider the meaning of “home.” This quest for a place better equipped to fulfill our needs, along with record-low mortgage rates, has skyrocketed the demand for home purchases.

This increase in demand, on top of the severe shortage of homes for sale, has also caused more bidding wars and thus has home prices appreciating rather dramatically. Some, therefore, have become cautious about buying a home right now.

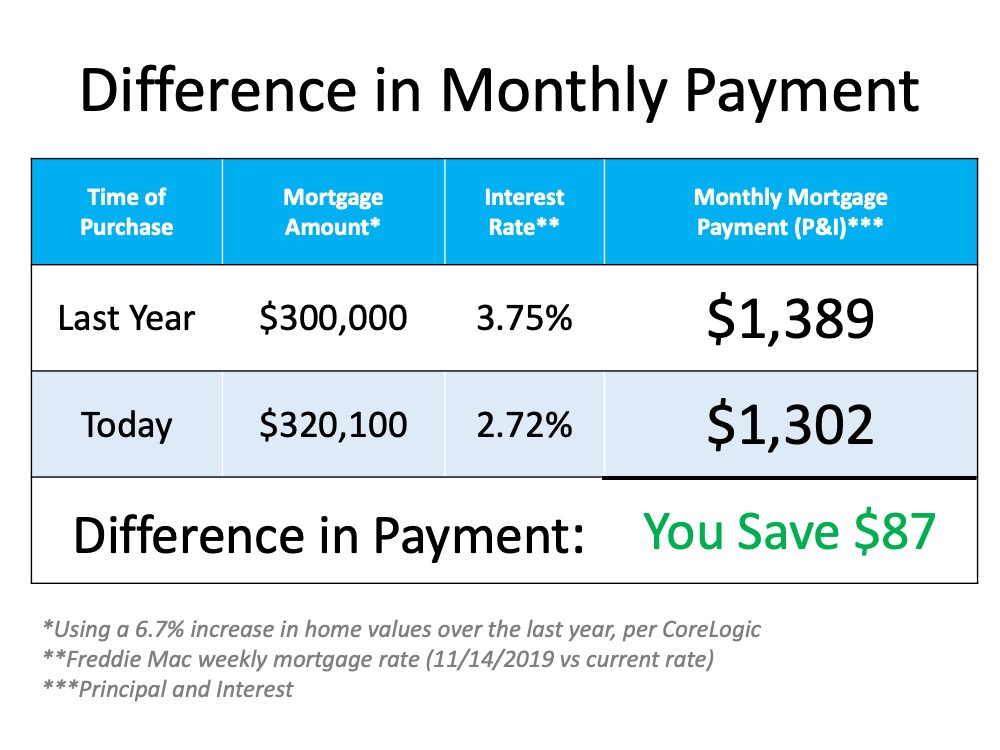

The truth of the matter is, even though homes have appreciated by a whopping 6.7% over the last twelve months, the cost to buy a home has actually dropped. This is largely due to mortgage rates falling by a full percentage point.

Let’s take a look at the monthly mortgage payment on a $300,000 house one year ago, and then compare it with that same home today, after it has appreciated by 6.7% to $320,100: Compared to this time last year, you’ll actually save $87 dollars a month by purchasing that home today, which equates to over one thousand dollars a year.

Compared to this time last year, you’ll actually save $87 dollars a month by purchasing that home today, which equates to over one thousand dollars a year.

But isn’t the economy still in a recession?

Yes, it is. That, however, may make it the perfect time to buy your first home or move up to a larger one. Tom Gil, a Harvard trained negotiator and real estate investor, recently explained:

“When volatile assets are facing recessions, hard assets, such as gold and real estate, thrive. Historically speaking, residential real estate has done better compared to other markets during and after recessions.”

That thought is substantiated by the fact that homeowners have 40 times the net worth of renters. Odeta Kushi, Deputy Chief Economist for First American Financial Corporation, recently said:

“Despite the risk of volatility in the housing market, numerous studies have demonstrated that homeownership leads to greater wealth accumulation when compared with renting. Renters don’t capture the wealth generated by house price appreciation, nor do they benefit from the equity gains generated by monthly mortgage payments, which become a form of forced savings for homeowners.”

Bottom Line

With home prices still increasing and mortgage rates perhaps poised to begin rising as well, buying your first home, or moving up to a home that better fits your current needs, likely makes a ton of sense.[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section fb_built=”1″ _builder_version=”3.18.2″][et_pb_row _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.18.2″]

Read More News and Insights

[/et_pb_text][/et_pb_column][/et_pb_row][et_pb_row _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_blog fullwidth=”off” posts_number=”3″ include_categories=”38,234″ show_author=”off” show_date=”off” show_categories=”off” _builder_version=”3.18.2″ header_level=”h5″ header_font=”||||||||” body_font=”||||||||” border_radii=”on|12px|12px|12px|12px” text_orientation=”center”][/et_pb_blog][/et_pb_column][/et_pb_row][/et_pb_section]

October 2020 Housing Market Update

Geoff Geen, President of Green Team Realty, welcomed everyone to the October 2020 Housing Market Update. The webinar, held on Tuesday, October 20 at 2 p.m. examined the housing market on both national and local levels.

If you missed the webinar or would like to view it again, it’s available here.

Meet the Panel

October Housing Market Update panelists were Nancy Sardo, and Tammy Scotto of Green Team New York Realty, and Keren Gonen of Green Team New Jersey Realty. Also joining the discussion was Ken Aulicino, Mortgage Loan Originator at Family First Funding.

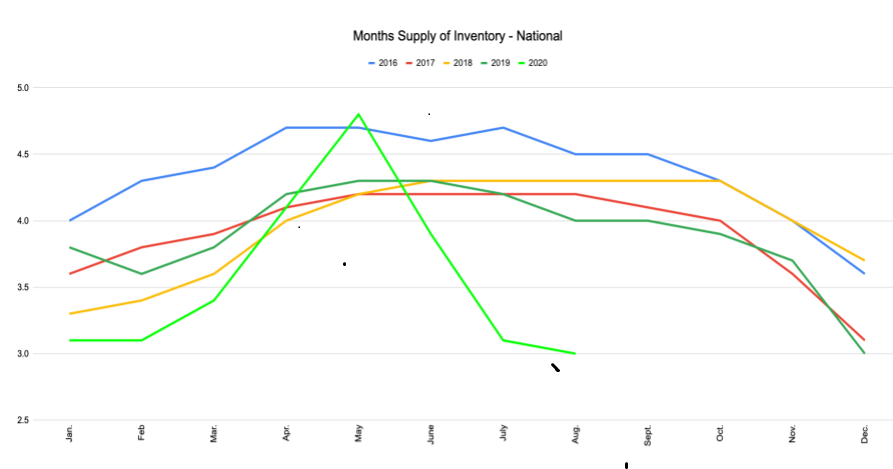

Can the housing market recovery be sustained?

The U.S housing market has been a “V-shaped” Recovery. However, inventory continues to decline and is a big challenge. So, can the housing market keep it up?

Pros

US Consumer Spending is almost in a V-shaped recovery. Unemployment has been coming down the last 6 to 7 months. The number of mortgages in active forbearance is decreasing. Prior to the Great Recession, it was a buyers market, due to the number of homes on the market. In the early 2000s, there was also a lot of new construction happening. Now, we are firmly in a sellers’ market. There are just not enough homes to satisfy the needs of the current market.

Cons

The shortage of inventory remains a major issue. According to Realtor.com,

“Since the beginning of the COVID pandemic in March, nearly 400,000 few homes have been listed compared to last year, leaving a gaping hole in the U.S. housing inventory…

As a result, home prices are accelerating at double last year’s pace.”

According to the National Association of Realtors, Existing Home Sales are up by 10.5%. However, listings are down 39%. Listings for New Homes are down by 31%. However, sales of new homes have increased by 43%.

This really shows the inventory story.

Local Stats

In Orange County, NY, there are increases in units sold and in average sales price. Sussex County, NJ is now showing strong increases in average sales price, as well as in units sold.

Learn More, Watch the Webinar

Watch Geoff’s full presentation on national and local economic and real estate trends. In addition, our expert panel discusses their experiences in this market, including new construction. Click here to view the webinar.

Furthermore, you can compare prior statistics and trends. Click here for the September 2020 Housing Market Update.

“Housekeeping” Items

Contact our Panelists

Join us on Tuesday, November 17 at 2 p.m.

Sign up for updates now at GreenTeamRealty.com/HMU

Do You Have Enough Money Saved for a Down Payment?

One of the biggest misconceptions for first-time homebuyers is how much you’ll need to save for a down payment. Contrary to popular belief, you don’t always have to put 20% down to buy a house. Here’s how it breaks down.

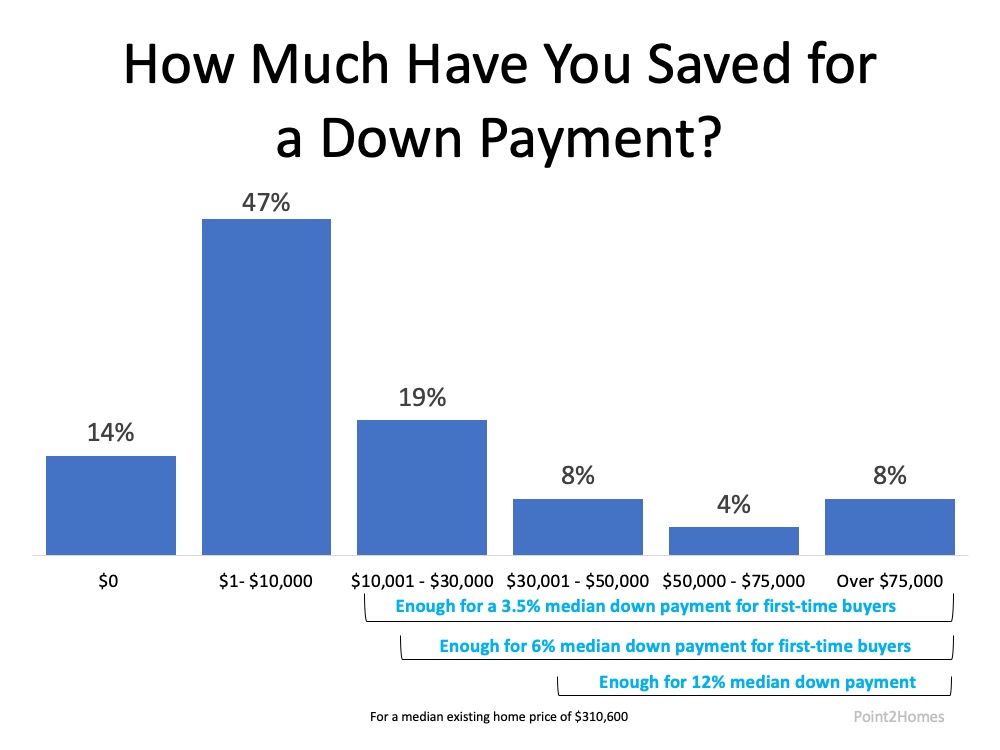

A recent survey by Point2Homes mentions that 74% of millennials (ages 25-40) say they’re interested in purchasing a home over the next 12 months. The study notes, “88% say they have significantly less savings than the average national down payment amount, which is $62,600.”

Thankfully, $62,600 is not the amount every buyer needs for a down payment in the United States. There are many different options available, especially for first-time homebuyers (millennial or not). That amount can also be significantly less, depending on the purchase price of the house.

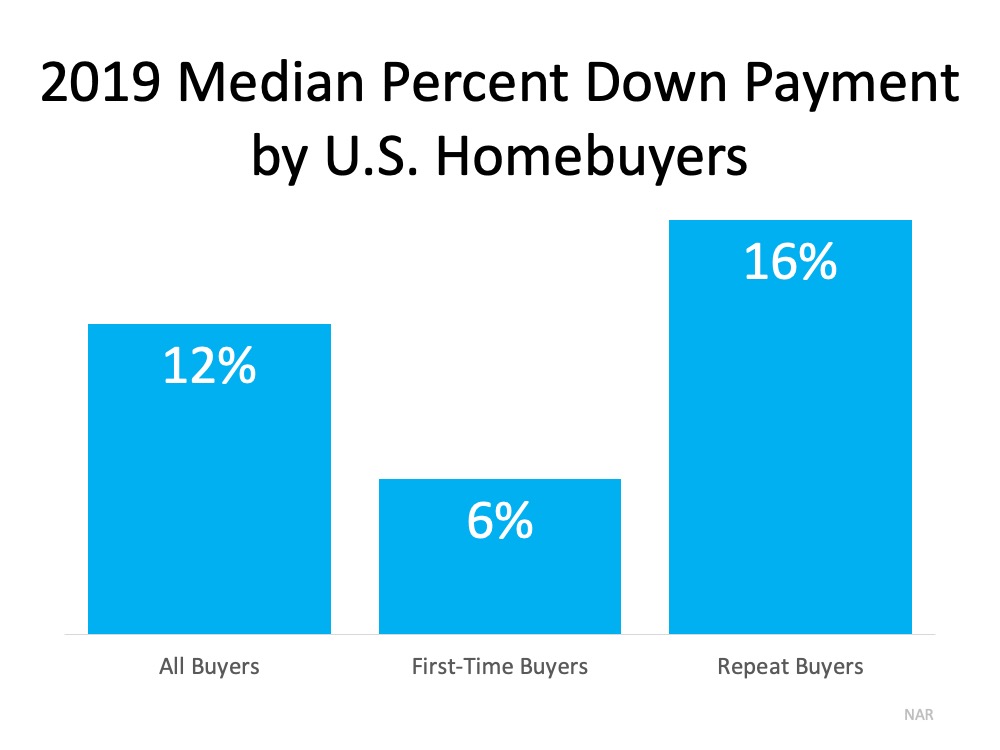

According to the National Association of Realtors (NAR), “The median existing-home price for all housing types in August was $310,600.” (These are the latest numbers available). NAR also indicates that:

“In 2019, the median down payment was 12 percent for all buyers, six percent for first-time buyers, and 16 percent for repeat buyers.” (See graph below):

That means if a qualified first-time buyer purchases a home at today’s median price, $310,600, with a 6% down payment, in reality, the down payment only amounts to $18,636. That’s nowhere near $62,600.

That means if a qualified first-time buyer purchases a home at today’s median price, $310,600, with a 6% down payment, in reality, the down payment only amounts to $18,636. That’s nowhere near $62,600.

Knowing there are also programs like FHA where the down payment can be as low as 3.5% of the purchase price for a first-time buyer, that up-front cost could be significantly less – as little as $10,871 for the same home noted above. There are also other programs like USDA and loans for Veterans that waive down payment requirements.

The Point2Homes study also shares how much millennials have indicated they’ve saved for a down payment. As we can see in the graph below, 39% have already saved enough for a down payment on a median-priced home. Another 47% are close to reaching that goal, depending on the purchase price of the home. Unfortunately, the lack of knowledge about the homebuying process is keeping many motivated first-time buyers on the sidelines. That’s why it’s important to contact a local real estate professional to understand the requirements in your local area if you want to buy a home. A trusted agent and your lender can guide you through the process.

Unfortunately, the lack of knowledge about the homebuying process is keeping many motivated first-time buyers on the sidelines. That’s why it’s important to contact a local real estate professional to understand the requirements in your local area if you want to buy a home. A trusted agent and your lender can guide you through the process.

Bottom Line

Be careful not to let big myths about homebuying keep you and your family out of the housing market. Let’s connect you with one of our Sales Agents to discuss your options today.

Mortgage Rates & Payments by Decade [INFOGRAPHIC]

[et_pb_section fb_built=”1″ _builder_version=”3.0.47″][et_pb_row _builder_version=”3.0.48″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.18.2″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]

![Mortgage Rates & Payments by Decade [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2020/08/13150648/20200814-MEM-1-1046x1306.jpg)

Some Highlights

- Sometimes it helps to see the dollars and cents you’ll save when you purchase a home while mortgage rates are low.

- It helps to get a rough idea of what your mortgage payment will be at different rates.

- Today’s low rates mean it’s less expensive to borrow money, so the savings over the life of your loan is significant.

- Connect with one of our Real Estate Sales Agents to determine the best way to position your family for a financially-savvy move in today’s market.

[/et_pb_text][/et_pb_column][/et_pb_row][et_pb_row custom_padding=”12px|0px|17.5781px|0px|false|false” _builder_version=”3.18.2″ locked=”off”][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_blog fullwidth=”off” posts_number=”3″ include_categories=”38″ show_author=”off” show_date=”off” show_categories=”off” _builder_version=”3.18.2″ header_level=”h5″ header_font=”||||||||” body_font=”||||||||” border_radii=”on|12px|12px|12px|12px” text_orientation=”center”][/et_pb_blog][/et_pb_column][/et_pb_row][/et_pb_section]

The Latest Unemployment Report: Slow and Steady Improvement

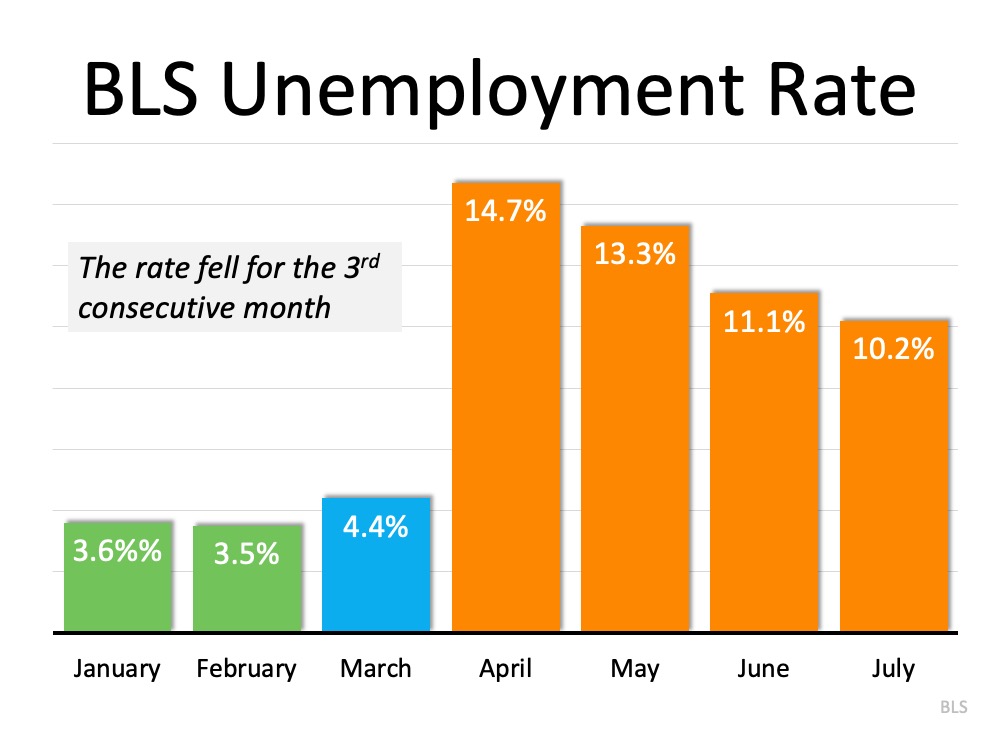

[et_pb_section fb_built=”1″ _builder_version=”3.0.47″][et_pb_row _builder_version=”3.0.48″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.0.74″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]Last Friday, the Bureau of Labor Statistics (BLS) released its latest Employment Situation Summary. Going into the release, the expert consensus was for 1.58 million jobs to be added in July, and for the unemployment rate to fall to 10.5%.

When the official report came out, it revealed that 1.8 million jobs were added, and the unemployment rate fell to 10.2% (from 11.1% last month). Once again, this is excellent news as this was the third consecutive month the unemployment rate decreased. There is, however, still a long way to go before the job market fully recovers. The Wall Street Journal (WSJ) put a potential date on that recovery:

There is, however, still a long way to go before the job market fully recovers. The Wall Street Journal (WSJ) put a potential date on that recovery:

“July’s payroll growth, at 1.8 million, still leaves total payrolls 12.9 million lower than in February. And yet if job gains continued at July’s pace, that deficit will be erased by March 2021. If payrolls reclaim their last peak in 13 months, that would be remarkably fast. It took more than six years after the last recession.”

Permanent vs. Temporary Unemployment

During a pandemic, it’s important to differentiate those who have lost their jobs on a temporary basis from those who have lost them on a permanent basis. Morgan Stanley economists noted in the same WSJ article:

“The rate of churn in the labor market remains incredibly high, but a notable positive detail in this month’s report was the downtick in the rate of new permanent layoffs.”

To address this, the core unemployment rate becomes increasingly important. It identifies the number of people who have permanently lost their jobs. This measure subtracts temporary layoffs and adds unemployed who did not search for a job recently. Jed Kolko, Chief Economist at Indeed and the founder of the index reported:

“Core unemployment fell in July for the first time in the pandemic. That’s the good news I was hoping for.”

What about the housing market?

The housing market has continued to show tremendous resilience during the pandemic. Commenting on the labor report, Robert Dietz, Chief Economist for the National Association of Home Builders (NAHB), tweeted:

“Housing continues to rebound in another positive labor market report. Home builder and remodeler job gains of 24K for July. Residential construction employment down just 56.4K compared to a year ago. Total residential construction employment at 2.85 million.”

Bottom Line

We should remain cautious in our optimism, as the recovery is ultimately tied to our future success in mitigating the ongoing health crisis. However, as Mike Fratantoni, Chief Economist for the Mortgage Bankers Association, reminds us: “The pace of job growth slowed in July, but the gains over the past three months represent an impressive rebound during the ongoing economic challenges brought forth by the pandemic.”

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section fb_built=”1″ _builder_version=”3.18.2″ custom_padding=”0px|0px|0|0px|false|false”][et_pb_row custom_padding=”66px|0px|17.5781px|0px|false|false” _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.18.2″]

You might also enjoy reading…

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section fb_built=”1″ _builder_version=”3.18.2″ custom_padding=”4px|0px|35.1719px|0px|false|false”][et_pb_row custom_padding=”5px|0px|17.5781px|0px|false|false” _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_blog fullwidth=”off” posts_number=”3″ include_categories=”38,234″ show_author=”off” show_date=”off” show_categories=”off” _builder_version=”3.18.2″ header_level=”h5″ header_font=”||||||||” body_font=”||||||||” border_radii=”on|12px|12px|12px|12px” text_orientation=”center”][/et_pb_blog][/et_pb_column][/et_pb_row][/et_pb_section]

Today’s Buyers Are Serious about Purchasing a Home

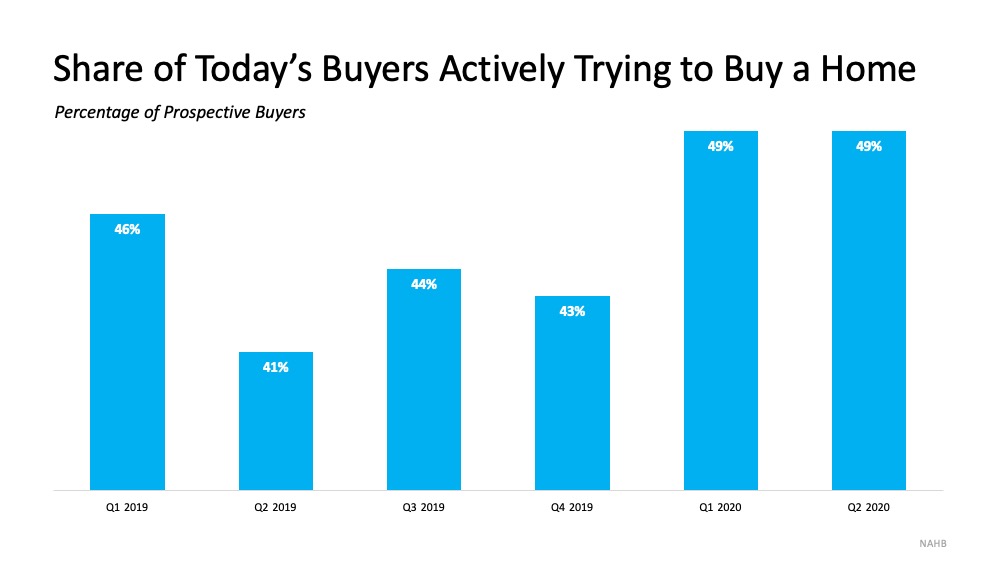

Today’s homebuyers are not just talking about their plans, they’re actively engaged in the buying process – and they’re serious about it. A recent report by the National Association of Home Builders (NAHB) indicates:

“…. Of American adults considering a future home purchase in the second quarter of 2020, about half (49%) are not simply planning it, they are actively engaged in the process to find a home. That is a significantly higher share than the comparable figure a year ago (41%), which suggests that the COVID-19 crisis and its accompanying record-low mortgage rates have converted some prospective buyers into active buyers.”

It’s no surprise that buyers are out in full force today. Many Americans now need more space to work from home, and the current low mortgage rates are providing an extra boost of motivation to enter the housing market.

It’s no surprise that buyers are out in full force today. Many Americans now need more space to work from home, and the current low mortgage rates are providing an extra boost of motivation to enter the housing market.

If you’re considering selling your house, know that today’s buyers are serious about making a move. Your opportunity to sell your house in a market with high demand is growing, especially as more millennials enter the housing market too. The same report also notes:

“Of Millennials planning a home purchase in the next year, 57% are already actively searching for a home.”

Odeta Kushi, Deputy Chief Economist at First American, explains:

“When breaking down house-buying power by educational attainment for millennials in 2019, we find that the higher the education, the higher the household income, and the higher the house-buying power. In 2019, median house-buying power for millennials increased 16 percent relative to 2018.”

As demand for homes to buy grows and more millennials enter the market with growing buying power, the opportunity to sell your house grows too.

Bottom Line

Today’s buyers are serious ones and more millennials are helping to fuel that charge. So, if you’re considering selling your home, let’s connect you with one of our Real Estate Sales Associates today to determine your next steps in the process while buyers are actively looking.

Taking Advantage of Homebuying Affordability in Today’s Market

Everyone is ready to buy a home at different times in their lives, and despite the health crisis, today is no exception. Understanding how affordability works and the main market factors that impact it may help those who are ready to buy a home narrow down their optimal window of time to make a purchase.

There are three main factors that go into determining how affordable homes are for buyers:

- Mortgage Rates

- Mortgage Payments as a Percentage of Income

- Home Prices

The National Association of Realtors (NAR), produces a Housing Affordability Index, which takes these three factors into account and determines an overall affordability score for housing. According to NAR, the index:

“…measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national and regional levels based on the most recent price and income data.”

Their methodology states:

“To interpret the indices, a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment.”

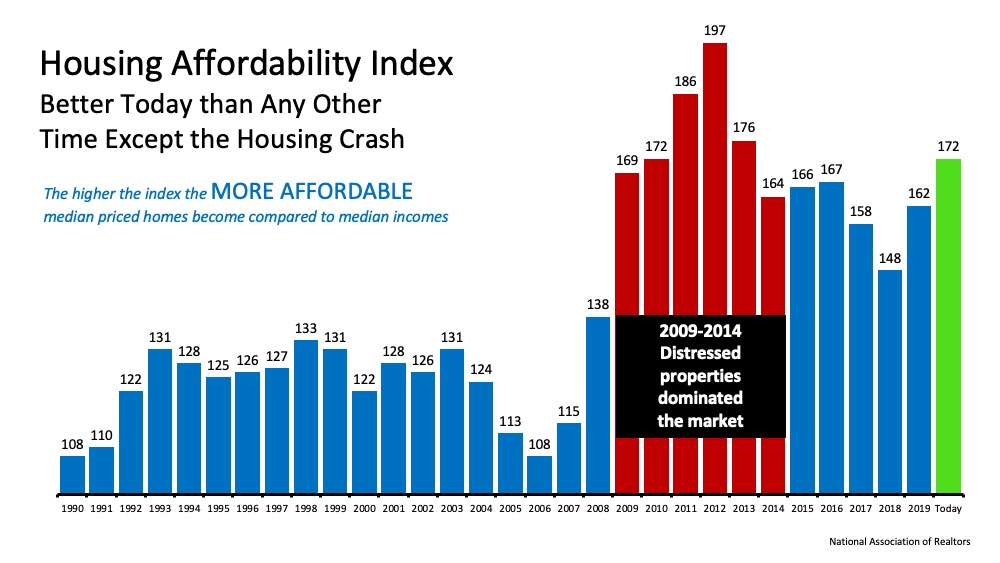

So, the higher the index, the more affordable it is to purchase a home. Here’s a graph of the index going back to 1990: The green bar represents today’s affordability. We can see that homes are more affordable now than they have been at any point since the housing crash when distressed properties (foreclosures and short sales) dominated the market. Those properties were sold at large discounts not seen before in the housing market.

The green bar represents today’s affordability. We can see that homes are more affordable now than they have been at any point since the housing crash when distressed properties (foreclosures and short sales) dominated the market. Those properties were sold at large discounts not seen before in the housing market.

Why are homes so affordable today?

Although there are three factors that drive the overall equation, the one that’s playing the largest part in today’s homebuying affordability is historically low mortgage rates. Based on this primary factor, we can see that it is more affordable to buy a home today than at any time in the last seven years.

If you’re considering purchasing your first home or moving up to the one you’ve always hoped for, it’s important to understand how affordability plays into the overall cost of your home. With that in mind, buying while mortgage rates are as low as they are now may save you quite a bit of money over the life of your home loan.

Bottom Line

If you feel ready to buy, purchasing a home this season may save you significantly over time based on historic affordability trends. Connect with one of our Sales Agents today to determine if now is the right time for you to make your move.