Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Is it Time to Sell Your Vacation Home?

The travel industry is one of the major sectors that’s been hit extremely hard by the COVID-19 pandemic. Today, it’s hard to know how long it will take for summer travelers to be back in action and for the industry to fully recover. Homeowners who rent their secondary properties on their own or through programs like Airbnb, which has over 660,000 listings in the U.S. alone, have been impacted in this challenging time. Some of these homeowners are considering selling their vacation homes, and understandably so.

A recent CNN article indicated:

“With global travel screeching to a halt during the pandemic, a number of Airbnb hosts are planning to sell their properties…These desperate moves come as hosts face the possibility of losing thousands of dollars a month in canceled bookings while bills, maintenance costs, and mortgage payments pile up.”

If you’re one of the property owners in this position, you too may be feeling the pain of decreased travel, especially as we prepare for the typical busy summer vacation season. A recent survey notes that 48% of Americans have already canceled summer travel plans due to the current health crisis. In addition, 36% indicated they don’t have vacation plans, and only 16% said they did not cancel their summer travel.

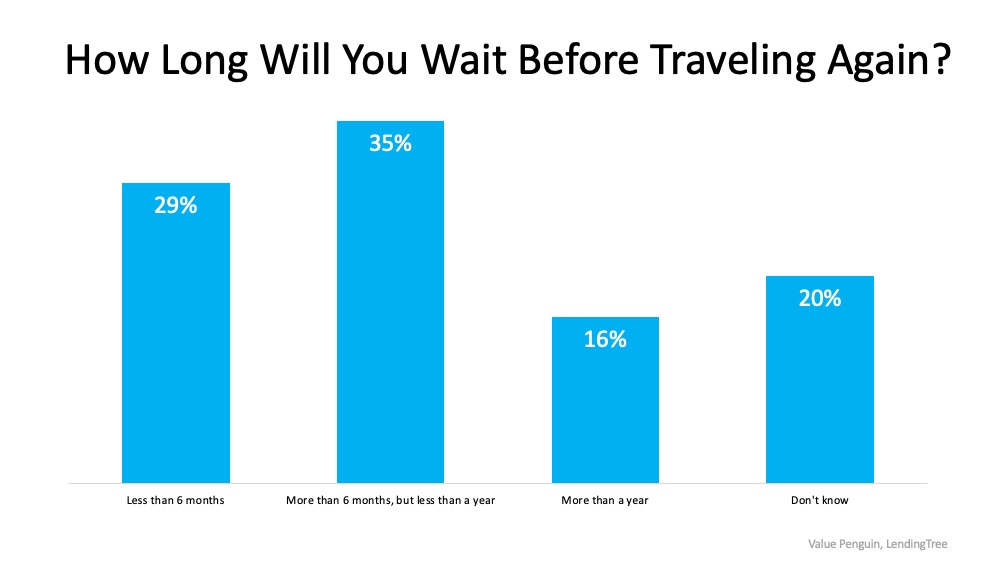

The same survey also asked, “How long will you wait before traveling again?” Not surprisingly, only 29% of respondents are planning to travel within the next 6 months. That means 71% are putting their plans on hold for at least 6 months, or are still unsure about future travel. That can continue to add to the significant income loss that many property renters felt this spring. If you’re considering selling your rental property, know that there are two key factors indicating that selling your vacation home now may be your best move as a homeowner.

If you’re considering selling your rental property, know that there are two key factors indicating that selling your vacation home now may be your best move as a homeowner.

1. Inventory Shortage

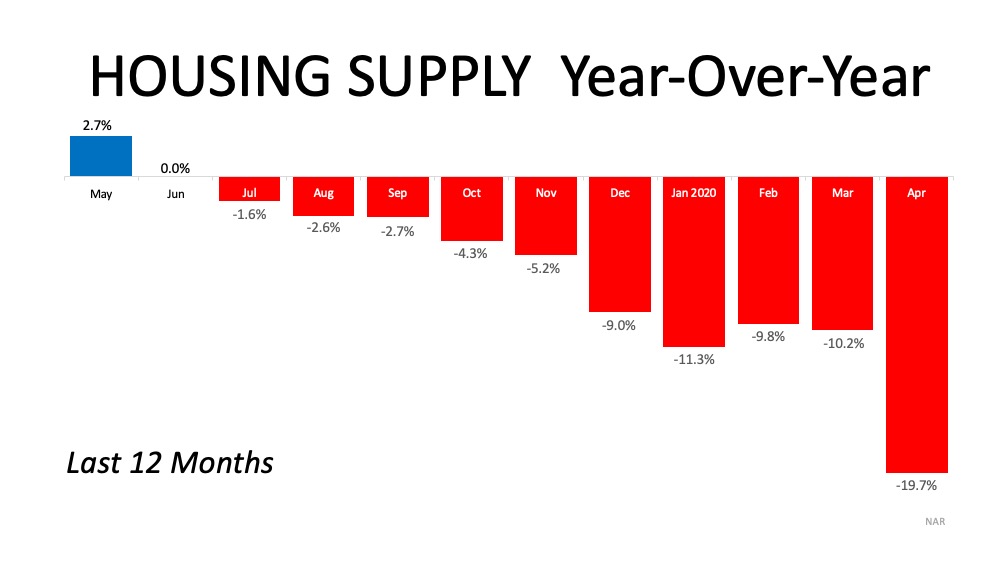

The inventory of overall homes for sale is well below the demand from potential buyers, so many eyes may be searching for a home like yours. According to the National Association of Realtors (NAR), total housing inventory, meaning homes available to purchase, is down 19.7% from one year ago (see graph below): Inventory across the country continues to be a challenge, with only a 4.1-month supply of listings available at the current sales pace. For a balanced market, where there are enough homes available for interested buyers to purchase, that number would need to bump up to a 6-month supply. This means we don’t have enough inventory for the number of buyers looking for homes, so selling in this scenario is ideal. Buyers are looking now, and some vacation homes make a great primary residence or second home for those eager to escape from more populated urban areas.

Inventory across the country continues to be a challenge, with only a 4.1-month supply of listings available at the current sales pace. For a balanced market, where there are enough homes available for interested buyers to purchase, that number would need to bump up to a 6-month supply. This means we don’t have enough inventory for the number of buyers looking for homes, so selling in this scenario is ideal. Buyers are looking now, and some vacation homes make a great primary residence or second home for those eager to escape from more populated urban areas.

2. Home Prices

The lack of inventory is also keeping homes from depreciating in value. Today, prices are holding strong and experts forecast home price appreciation to continue throughout this year. Selling your home while prices are holding steady is a sound business move. You’ll likely have equity you’ve earned working for you as well. If your home has been vacant for the past few months, the forced savings you have built in your equity may help balance out possible rental income loss due to the slowdown in the travel industry.

Bottom Line

We don’t know exactly when heightened summer travel will return or what it will look like when it does. If you’re considering selling your vacation home, connect with one of our Sales Agents today to determine your options in the current market.

Are NYC residents moving to the suburbs?

Are people really leaving NYC for the suburbs?

Are NYC residents moving to the suburbs? Statistics show how Covid-19 has devastated New York City. The number of people with COVID-19 and the number of deaths is staggering. Social distancing is difficult. There is no doubt that crowded streets, elevators, and often apartments are not conducive to sheltering-in-place. So, are people really leaving NYC for the suburbs?

According to both local and national news sources, the answer is a resounding “YES!” The headlines tell the story.

National Media

USA Today‘s headline screams, “Get me out of here! Americans flee crowded cities amid Covid-19, consider permanent moves.” According to that article, nearly one-third of Americans are considering moving to less densely populated areas because of Covid-19. On May 8 the New York Times described this phenomenon in “Coronavirus Escape: To the Suburbs.” Then, on May 16 they published “Where New Yorkers Moved to Escape Coronavirus.” According to CNBC, Wealthy New Yorkers flee Manhattan for suburbs and beyond.

Local Media

Locally, radio station 101.5 WPDH posted two blogs on this subject. The first, “NYC Residents Expected to Move to Hudson Valley in Droves.” And “Sellers market driving Hudson Valley Home Prices Way Up.” Additionally, Straus News just published the following story in all its local papers for Orange County NY, and Sussex County NJ: “Pandemic-driven house frenzy hits local towns.”

Green Team Realty Sales Associates: Are they seeing NYC residents moving to the suburbs?

Current real estate market conditions and economic trends were major points of discussion during Green Team Realty’s monthly Housing Market Update. We asked several sales associates if they are seeing NYC residents moving to the suburbs as a result of COVID-19.

Green Team New York Realty – Warwick and Orange County, New York

Angela Murphy, Real Estate Salesperson, and Business Development Associate,

I have seen a rise of new buyers coming from all 5 boroughs of the city. Most of my clients want municipals verses septic, well or oil tanks, which has opened up many areas to view in Orange County. The pandemic has definitely pushed them to head north quicker than they might have, otherwise.

Nancy Sardo, Associate Real Estate Broker

I am seeing an influx of highly qualified tenants as well as an above-average amount of new buyers ready to move quicker than before. We are seeing many more cash buyers, many more full-price offers with less negotiation from a smart buyer. Experienced buyers to the area are more willing to do some elbow grease in order not to hiccup on the deal. Otherwise, they risk the seller moving onto the backup offer. Buyers and people, in general, are serious about the betterment of their surroundings. And, with what we are currently going through, they are now more apt to pay for it. We are in a seller’s market and here in Warwick NY and Orange County on a whole, there is an exaggerated upswing of interest in our beautiful Hudson Valley.

Jennifer DiCostanzo, Associate Broker

Interest is trending with buyers looking for a home that meets their needs both for lifestyle and working from home. They like the idea of self-sufficient living. Being just 60 miles from NYC makes the lower Hudson Valley, with its pricepoint, very attractive for primary and secondary homes. Everyone is coming to a realization that home has to meet both work and leisure needs. Also desired are adaptable living spaces. Living through this pandemic has redefined the concept of home for many people. Outdoor space has become a luxury, particularly for City dwellers. However, it’s not just City dwellers who are redefining what “home” means. There are local buyers who are also looking for that change in lifestyle, space and function.

Green Team New Jersey Realty – Vernon and Sussex County, New Jersey

Kristi Anderson, Realtor

I think that many buyers are coming to the Sussex area because we have had much fewer cases of COVID-19 up here. Most of my clients are buying second homes.

Keren Gonen, Real Estate Salesperson

I am seeing a LOT of NYC buyers. They are CASH mostly and looking to run away. Some are buying a second home, but plenty are moving in this direction to get away from the City completely and realizing the advantages of living in “The Country.” Those buyers have a much larger budget than our “usual” buyers and are looking for updated houses mostly. They are ready, willing, able and QUALIFIED buyers. They are all mesmerized by our charm here in Sussex county.

After months of sheltering in place, many people are reexamining their concept of the ideal home. This pandemic has shown us that we can’t take for granted life as usual. New York City has undergone a drastic transformation. That ideal City life is on pause. Broadway shows, restaurants, boutiques, department stores, museums, vibrant nightlife, closed, Families living in cramped apartments, worried about catching the virus, long for privacy, more room, areas to work, and space for the kids. Furthermore, they’re looking for outdoor living space. And approximately 60 miles away is the beautiful countryside of Orange and Sussex Counties.

NYC residents are looking for homes that provide lots of room for their family’s needs, including work from home space. Covid-19 has shown us the possibilities that exist in telecommuting. People and businesses are realizing that it may not be necessary for people to go to the office every day. As noted above, there are also people looking for second homes, so that they have someplace to “escape” to, should another shelter-in-place be required. Even in a seller’s market, they know they can get more house for their money here. Finally, there are unique hamlets, villages, and towns that offer lifestyles and qualities that people have decided are just what they need in this day and age.

Experts Predict Economic Recovery Should Begin in the Second Half of the Year

One of the biggest questions we all seem to be asking these days is: When are we going to start to see an economic recovery? As the country begins to slowly reopen, moving forward in strategic phases, business activity will help bring our nation back to life. Many economists indicate a recovery should begin to happen in the second half of this year. Here’s a look at what some of the experts have to say.

Jerome Powell, Federal Reserve Chairman

“I think there’s a good chance that there’ll be positive growth in the third quarter. And I think it’s a reasonable expectation that there’ll be growth in the second half of the year…

So, in the long run, I would say the U.S. economy will recover. We’ll get back to the place we were in February; we’ll get to an even better place than that. I’m highly confident of that. And it won’t take that long to get there.”

Nonpartisan Analysis for the U.S Congress

“The economy is expected to begin recovering during the second half of 2020 as concerns about the pandemic diminish and as state and local governments ease stay-at-home orders, bans on public gatherings, and other measures. The labor market is projected to materially improve after the third quarter; hiring will rebound and job losses will drop significantly as the degree of social distancing diminishes.”

Neel Kashkari, President, Minneapolis Federal Reserve Bank

“I think we need to prepare for a more gradual recovery while we hope for that quicker rebound.”

We’re certainly not out of the woods yet, but clearly many experts anticipate we’ll see a recovery starting this year. It may be a bumpy ride for the next few months, but most agree that a turnaround will begin sooner rather than later.

During the planned shutdown, as the economic slowdown pressed pause on the nation, many potential buyers and sellers put their real estate plans on hold. That time coincided with the traditionally busy spring real estate season. As we look ahead at this economic recovery and we begin to emerge back into our communities over the coming weeks and months, perhaps it’s time to think about putting your real estate plans back into play.

Bottom Line

The experts note a turnaround is on the horizon, starting as early as later this year. If you paused your 2020 real estate plans, connect with your Sales Agent today to determine how you can re-engage in the process as the country reopens and the economy begins a much-anticipated rebound.

May 2020 Housing Market Update

Geoff Green, President of Green Team Realty, welcomed everyone to the May 2020 Housing Market Update. The webinar was held on Tuesday, May 19 at 2 p.m. And, according to Green, “These are interesting times we live in,” to say the least. Geoff shares both national and local stats. Furthermore, he checks in with those who have “boots on the ground.” Sales Associates from Green Team New York Realty and Green Team New Jersey Realty share what’s happening in their respective states and communities. There are different regulations for the real estate industry in New York and New Jersey. Thus, there are differing impacts on what is happening in each state.

If you missed the webinar or would like to view it again, it’s available here:

Meet the Panel

The May 2020 Housing Market Update panel shared their observations, experiences, and expertise in this Covid-19 market. Keren Gonen and Kristi Anderson with Green Team New Jersey Realty talked about Vernon and the Sussex County NJ market. Nancy Sardo and Angela Murphy, with Green Team New York Realty, discussed Warwick and the Orange County NY market. Summer Mangels, Home Loan Consultant with Valley National Bank, shared her experiences with financing and refinancing in a Covid-19 market. Watch the above video to hear what the experts had to say.

Something everyone is talking about is:

When is the economy going to fully recover?

The Chairman of the Federal Reserve recently said that recovery is going to take longer than most people expect. However, several major financial institutions are calling for recovery in the second half of 2020. They include Goldman Sachs, JP Morgan, Morgan Stanley, and Wells Fargo. And, although unemployment numbers are historically high, they are trending down in terms of the number of new filings. As the country starts to reopen, we will hopefully see unemployment numbers go down.

The US Bureau of Labor Statistics provides data on the professions and categories most impacted by unemployment. In our April 2020 Housing Market Update we discussed those categories making up the largest majority of unemployed. Service and Bartending were the biggest category then. That number has come down a little as of May 8. Hopefully, as more and more businesses are able to reopen, people in these industries will be able to return to work.

Impact of Covid-19 to Real Estate Showings in North America

Data from ShowingTime provides analytics on the impact of Covid-19 on real estate showings. In March, showings plummeted. However, in mid-April, they started to shoot back up. When thrust into shut-down mode, there was panic and uncertainty. But as time has gone by, we’re learning how to more comfortably deal with the challenges with safety in mind. The reality is people still need homes. People still need to find homes when relocating. Life goes on. And we’re adapting to the rules and regulations as they change.

Homeowner Equity

Another important factor is the percentage of homeowner equity. If you have no mortgage, you will probably be calmer about current financial challenges and uncertainty and be more willing to spend. However, if you have a high debt to equity ratio, things will be tighter and you’ll probably have to hold back on spending. 42% of homeowners in the United States have no mortgage. 58% of all homes in America have at least 60% equity. And the average equity of mortgaged homes is $177,000. These stats show that homeownership offers many Americans some financial stability.

Years for the unemployment rate to return to the pre-crisis level

National and Local Stats on Units Sold & Average Sales Price

On the national level, the chart shows existing home sales for March (pre-COVID). At that point, home sales were a little lower than the previous few years. Prices were on an upward trend pre-COVID. The months’ supply of inventory is showing a seller’s market, with the lack of inventory available.

What is especially interesting is what is going on in Orange County, NY versus Sussex County, NJ. These are bordering counties in different states, with different COVID regulations. In New York, realtors cannot physically show homes to buyers. In New Jersey, they can. Sales in Orange County have plummeted. April numbers were substantially lower than in previous years. However, average sales price was not impacted. In Sussex, April was a good month. They held firm as far as units sold. And prices are continuing to rise.

“Housekeeping” Details:

To reach any of the May 2020 Housing Market Update panelists,

A Surprising Shift to the ‘Burbs May Be on the Rise

While many people across the U.S. have traditionally enjoyed the perks of an urban lifestyle, some who live in more populated city limits today are beginning to rethink their current neighborhoods. Being in close proximity to everything from the grocery store to local entertainment is definitely a perk, especially if you can also walk to some of these hot spots and have a short commute to work. The trade-off, however, is that highly populated cities can lack access to open space, a yard, and other desirable features. These are the kinds of things you may miss when spending a lot of time at home. When it comes to social distancing, as we’ve experienced recently, the newest trend seems to be around re-evaluating a once-desired city lifestyle and trading it for suburban or rural living. George Ratiu, Senior Economist at realtor.com notes:

“With the re-opening of the economy scheduled to be cautious, the impact on consumer preferences will likely shift buying behavior…consumers are already looking for larger homes, bigger yards, access to the outdoors and more separation from neighbors. As we move into the recovery stage, these preferences will play an important role in the type of homes consumers will want to buy. They will also play a role in the coming discussions on zoning and urban planning. While higher density has been a hallmark of urban development over the past decade, the pandemic may lead to a re-thinking of space allocation.”

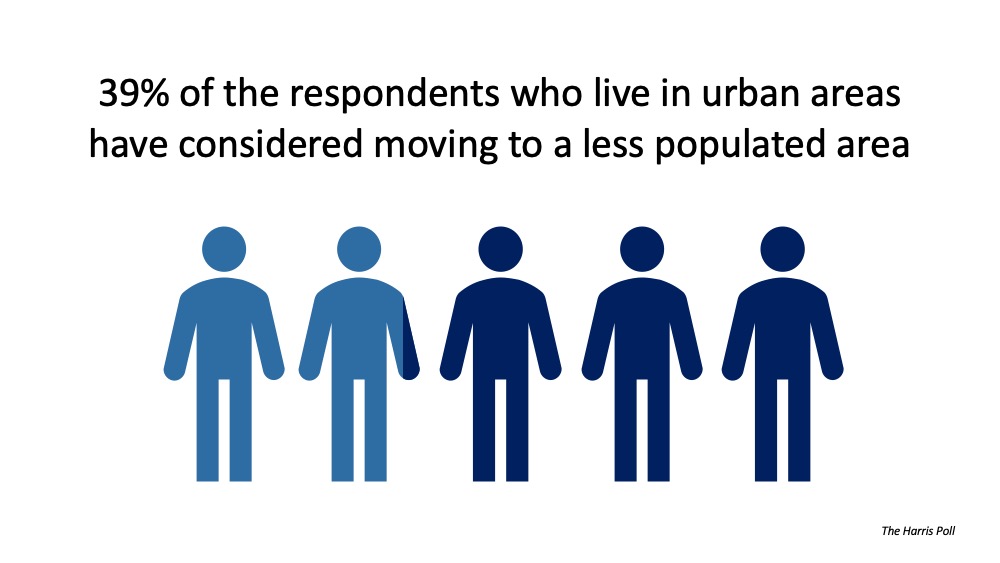

The Harris Poll recently surveyed 2,000 Americans, and 39% of the respondents who live in urban areas indicated the COVID-19 crisis has caused them to consider moving to a less populated area. Today, moving outside the city limits is also more feasible than ever, especially as Americans have quickly become more accustomed to – and more accepting of – remote work. According to the Pew Research Center, access to the Internet has increased significantly in rural and suburban areas, making working from home more accessible. The number of people working from home has also spiked considerably, even before the pandemic came into play this year.

Today, moving outside the city limits is also more feasible than ever, especially as Americans have quickly become more accustomed to – and more accepting of – remote work. According to the Pew Research Center, access to the Internet has increased significantly in rural and suburban areas, making working from home more accessible. The number of people working from home has also spiked considerably, even before the pandemic came into play this year.

Check out our listings here.

Bottom Line

If you have a home in the suburbs or a rural area, you may see an increasing number of buyers looking for a property like yours. If you’re thinking of buying and don’t mind a commute to work for the well-being of your family, you may want to consider looking at homes for sale outside the city. Connect with one of our Sales Agents today to discuss the options available in our area.

#1 Financial Benefit of Homeownership: Family Wealth

While growing up, we were taught by our parents and grandparents that owning a home is a financially savvy move. They explained how a mortgage is like a “forced savings plan.” When you pay rent, that money is lost forever. When you make a mortgage payment, much of that money accumulates as equity in the home. So, what exactly is equity? The equity in your home is the amount of money you can sell it for minus what you still owe on the mortgage. Every month you make a mortgage payment, and every month a portion of what you pay reduces the amount you owe. That reduction of your mortgage every month increases your equity. A recent study by CoreLogic explained that homeowners gained substantial equity over the last twelve months, and are essentially sitting on large sums of cash in their homes. In the study, Frank Nothaft, Chief Economist for CoreLogic explained:

“The CoreLogic Home Price Index recorded a quickening of home price gains during the fourth quarter of 2019, helping to boost home equity wealth. The average family with a mortgage had a $7,300 gain in home equity during the past year, and a total of $177,000 in home equity wealth.”

For most families, their home is their largest financial asset. This increase in equity drives the net worth, or family wealth, of the homeowner. Renters are not earning that benefit. Instead, they’re building the net worth of their landlord.

Bottom Line

Home price growth will moderate during the pandemic. But once a cure is available, most experts agree that home values will again begin to appreciate at levels similar to what we’ve seen over the last several years. In the long run, our family elders will be proven correct: owning a home is a savvy financial move and there are many benefits of homeownership. Check out our article on the impact Covid might have on Home Values here.

1st Quarter 2020 Sales Leaders

Congratulations From Geoff Green, President Of Green Team Realty, To Our 1st Quarter Sales Leaders

I am pleased to announce our 1st Quarter Sales Leaders for 2020. They are Jennifer DiCostanzo of our Warwick Office, and Barbara Tesa of our Vernon Office. 2020 started out strong, giving us all high hopes for a very successful year. Then towards the end of the 1st quarter, everything changed. Normally, I’d be photographed presenting an award to each quarterly sales leader. However, while I can’t congratulate them in person, I can do so here.

Once again Jennifer tops the production charts. Her work ethic is second to none and it shows. Jen is a tremendous Realtor who we are extremely grateful to call a Green Teamer!

Barbara is the consummate professional. Always responsive, always learning, and always producing. We are extremely fortunate to have Barbara as part of our team.

Jennifer DiCostanzo and Barbara Tesa at Green Team 2019 Awards Ceremony

Jennifer DiCostanzo, Green Team New York Realty

Jennifer DiCostanzo is no stranger to the Sales Leader Award. She has received the Yearly Sales Award each year since joining Green Team in 2015. Jen received the MVP Award in 2017 for more than $10 Million in Sales. Then again, in 2019, for more than $12 Million in Sales. Jen attributes her success to caring about her clients, working hard, and constantly learning. By keeping informed, she is best able to serve her clients to the best of her ability. Even in the midst of a pandemic.

With the challenges presented by COVID19, Jen has shared relevant information and resources with the community. She has written columns published in local newspapers. Jen feels it is important for people to understand their options. And that can range from mortgage forbearance to understanding current restrictions. Further, she has advocated on behalf of local organizations needing help and support as they give help and support to the community.

Jen’s thoughts on Covid19’s impact on real estate transactions

We began the first quarter off with a very strong market. Then suddenly overnight COVID changed every aspect of our lives. We had to immediately customize business practices and protocols. However, even though we are in a climate of social distancing, real estate needs are very much a priority and at the forefront of keeping the economy stable and on track. And by implementing cutting edge technologies, we are able to handle complex real estate market operations.

Stepping off of 2020 1st quarter has fueled stronger client relationships. We have had to seamlessly accelerate to virtual and remote platforms. And by doing so have transitioned both home buyers and sellers safely during a COVID market.

This is truly an essential time for both buyers and sellers to evaluate options and their own financial stability. It’s also an essential time to work with experts who understand the changing requirements and regulations that impact the decision to buy or sell a home. Now, more than ever, it is vital to work with real estate professionals, from your agent, lenders, attorneys and home inspectors, who are familiar with local regulations, safety concerns, etc. to make sure that your transaction proceeds on track and safely, with as little stress as possible. However, setting a level of expectation is vital so you can easily adapt to COVID timing factors. They have also been adjusted with remote and limited staff in all business platforms, from local, municipal and state agencies, and may indeed require more patience. It’s important to remember they are also working through COVID conditions as well.

Barbara Tesa, Green Team New Jersey Realty

Barbara Tesa is also no stranger to the Sales Leader Award, She received the award for the 3rd and 4th Quarters of 2017. Barbara also received the Captain’s Club Award for 2019, with between $3 and 5 Million in sales. Further, she received the New Jersey Realtors Circle of Excellence Award for 2017, 2018, and 2019. When Barbara joined Green Team New Jersey Realty, she brought with her an extensive resume. She has 20+ years of experience in residential and commercial real estate management. And she has been a successful, licensed real estate agent in New Jersey for 11 years now. Barbara’s motto is, “YOUR Property… MY Priority!” Which is fitting, because it’s important to her that her clients feel confident their interests are top priority throughout a transition.

Barbara’s thoughts on Covid19’s impact on real estate transactions

The beginning of the quarter started off strong with a very active January/February and early March. It felt like buyers and sellers had a lot of confidence in the market on both sides. Then, the uncertainty of real estate in COVID-19 times gave buyers and sellers a pause in mid-March. However, it seems to have been only temporary because buyers have remained active with their searches, their desire to see homes in person, and their desire to move. And sellers still want to sell.

We are just doing things a little differently now, taking every precaution with clients under social distancing guidelines when entering properties, meeting for home inspections, and right through to closing a transaction. People are still on the move and we will keep them moving as smoothly as possible. Despite COVID-19, based on the activity I’ve been seeing in the last 3-4 weeks, I’m looking forward to a robust remainder of the year. I am finding that people still want to move on with their plans, so the determination is there in the market.

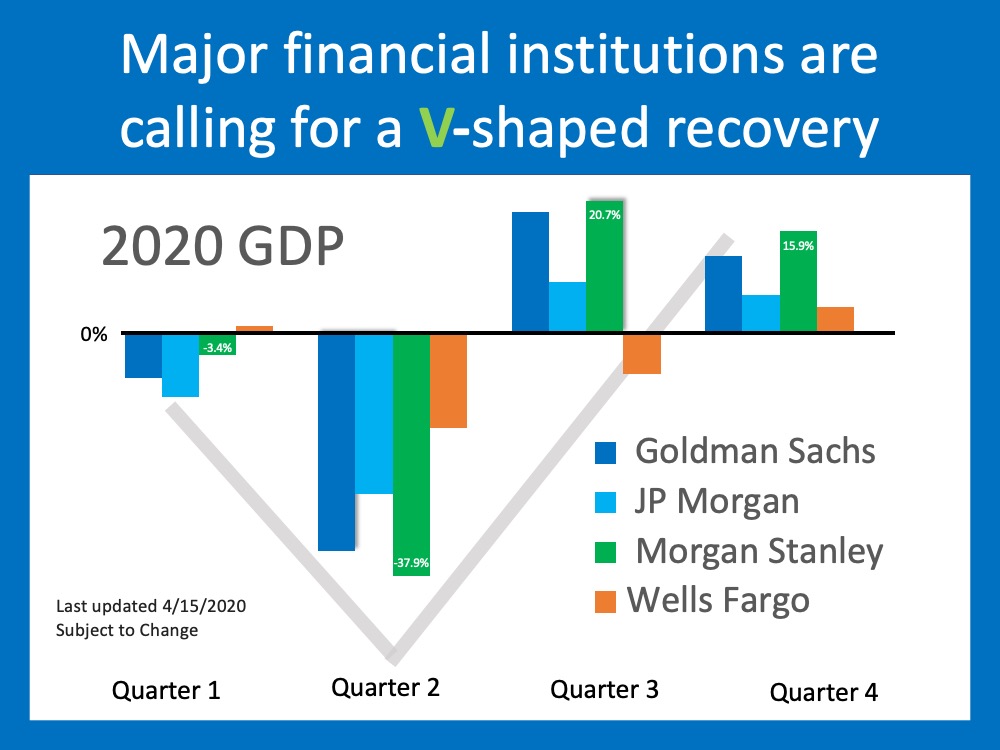

Will this Economic Crisis Have a V, U, or L-Shaped Recovery?

[et_pb_section fb_built=”1″ _builder_version=”3.0.47″][et_pb_row _builder_version=”3.0.48″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.0.74″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]Many American businesses have been put on hold as the country deals with the worst pandemic in over one hundred years. As the states are deciding on the best strategy to slowly and safely reopen, the big question is: how long will it take the economy to fully recover? Let’s look at the possibilities. Here are the three types of recoveries that follow most economic slowdowns (the definitions are from the financial glossary at Market Business News):

- V-shaped recovery: an economic period in which the economy experiences a sharp decline. However, it is also a brief period of decline. There is a clear bottom (called a trough by economists) which does not last long. Then there is a strong recovery.

- U-shaped recovery: when the decline is more gradual, i.e., less severe. The recovery that follows starts off moderately and then picks up speed. The recovery could last 12-24 months.

- L-shaped recovery: a steep economic decline followed by a long period with no growth. When an economy is in an L-shaped recovery, getting back to where it was before the decline will take years.

What type of recovery will we see this time?

No one can answer this question with one hundred percent certainty. However, most top financial services firms are calling for a V-shaped recovery. Goldman Sachs, Morgan Stanley, Wells Fargo Securities, and JP Morgan have all recently come out with projections that call for GDP to take a deep dive in the first half of the year but have a strong comeback in the second half.

Is there any research on recovery following a pandemic?

There have been two extensive studies done that look at how an economy has recovered from a pandemic in the past. Here are the conclusions they reached: 1. John Burns Consulting:

“Historical analysis showed us that pandemics are usually V-shaped (sharp recessions that recover quickly enough to provide little damage to home prices), and some very cutting-edge search engine analysis by our Information Management team showed the current slowdown is playing out similarly thus far.”

2. Harvard Business Review:

“It’s worth looking back at history to place the potential impact path of Covid-19 empirically. In fact, V-shapes monopolize the empirical landscape of prior shocks, including epidemics such as SARS, the 1968 H3N2 (“Hong Kong”) flu, 1958 H2N2 (“Asian”) flu, and 1918 Spanish flu.”

The research says we should experience a V-shaped recovery.

Does everyone agree it will be a ‘V’?

No. Some are concerned that, even when businesses are fully operational, the American public may be reluctant to jump right back in. As Market Business News explains:

“In a typical V-shaped recovery, there is a huge shift in economic activity after the downturn and the trough. Growing consumer demand and spending drive the massive shift in economic activity.”

If consumer demand and spending do not come back as quickly as most expect it will, we may be heading for a U-shaped recovery. In a message last Thursday, Chris Hyzy, Chief Investment Officer for Merrill and Bank of America Private Bank, agrees with other analysts who are expecting a resurgence in the economy later this year:

“We’re forecasting real economic growth of 30% for the U.S. in the 4th quarter of this year and 6.1% in 2021.”

His projection, however, calls for a U-shaped recovery based on concerns that consumers may not rush back in:

“After the steep plunge and bottoming out, a ‘U-shaped’ recovery should begin as consumer confidence slowly returns.”

Bottom Line

The research indicates the recovery will be V-shaped, and most analysts agree. However, no one knows for sure how quickly Americans will get back to “normal” life. We will have to wait and see as the situation unfolds.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section fb_built=”1″ _builder_version=”3.18.2″][et_pb_row _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_post_nav in_same_term=”on” _builder_version=”3.18.2″ title_font=”|800|||||||” title_text_color=”#ffffff” title_font_size=”15px” background_color=”#007a42″ border_radii=”on|2px|2px|2px|2px” border_width_all=”2px” border_color_all=”#007a42″ custom_padding=”1px|4px|1px|4px”][/et_pb_post_nav][/et_pb_column][/et_pb_row][/et_pb_section]

April 2020 Housing Market Update

[et_pb_section fb_built=”1″ admin_label=”section” _builder_version=”3.0.47″][et_pb_row admin_label=”row” _builder_version=”3.0.48″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text admin_label=”Text” _builder_version=”3.0.74″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]

Covid19 has caused economic turmoil, health crises and uncertainty. However, a historical perspective may help us manage emotions and enable us to see what is happening in the housing market and navigate it accordingly. Below is a recording of the Housing Market Update as well as a summary of the most important discussion points.

National – Historical Perspective

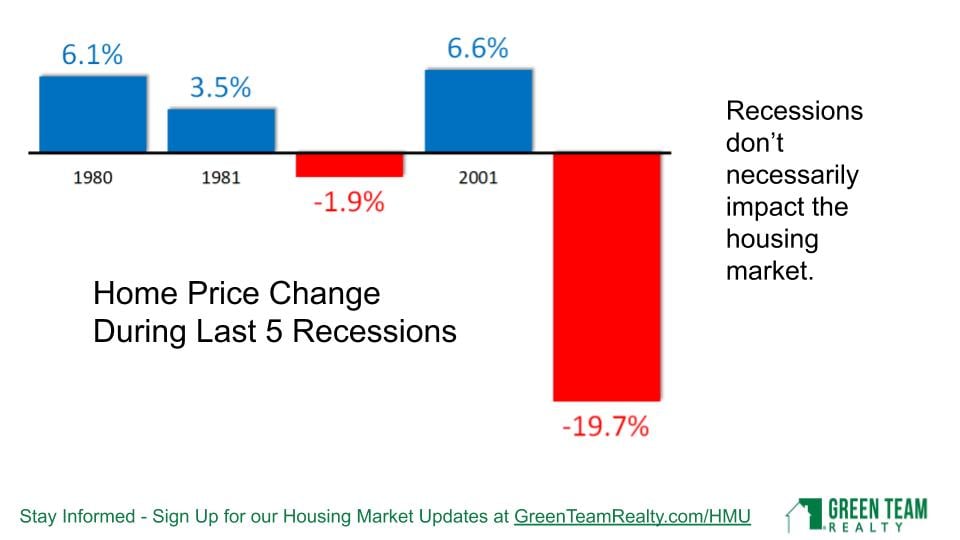

Will this be like 2008, the start of the great recession?

The Housing Market was greatly impacted at that time because it was the catalyst that caused the Great Recession. Home price changes during last 5 recessions indicate that recessions do not necessarily impact the housing market. In 3 of the last 5 recessions, housing markets actually increased.

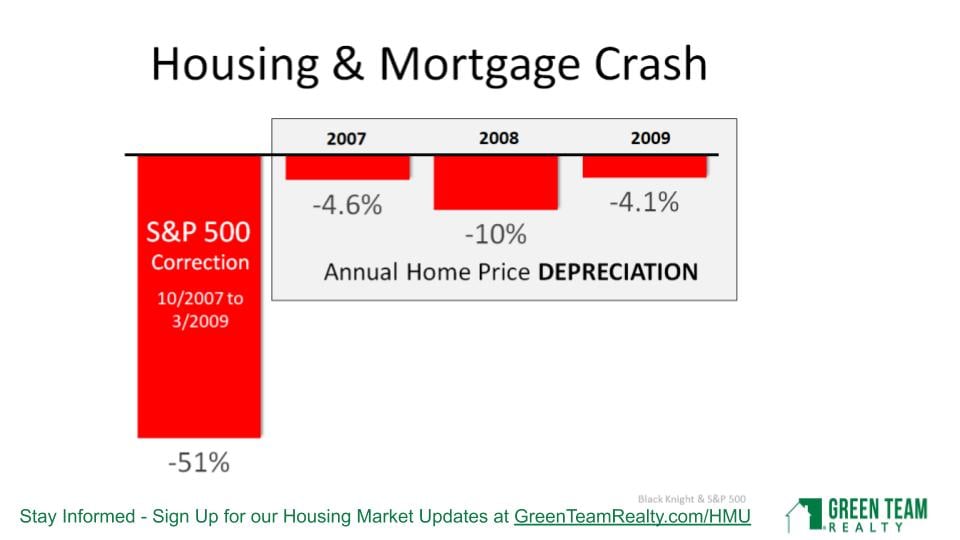

Housing and Mortgage Crash

In 2007, 2008 and 2009, the annual home price depreciation was significant. However, at the time we were dealing with sub-prime lending, etc. However, looking further back, to the Dot.com crash and 9/11 market crash, there was a significant S&P 500 stock market correction. Yet prices in the housing market continued to increase. There were good fundamentals in place.

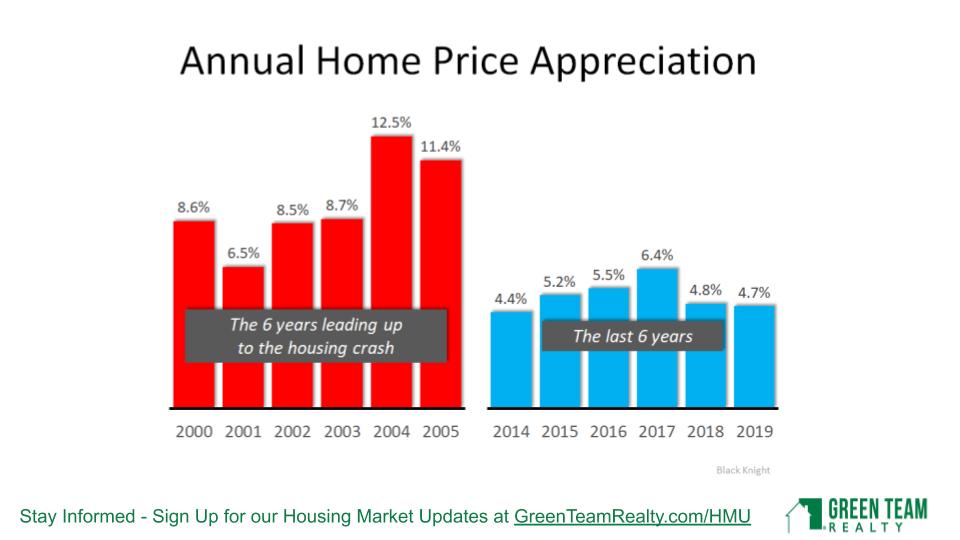

Annual Home Price Appreciation

In any marketplace, you have to look at overall values. Are assets undervalued or overvalued? With the run-up to 2008, from 2000 to 2005, there were major price increases year over year. 6.5% was the lowest increase, with the highest being 12.5%. However, since 2014, 6.4% has been the highest increase. We haven’t gone back to those major subprime lending issues that happened before.

Mortgage Credit Availability and Affordability

The Great Recession required mortgage industry restructuring. That, in turn, led to qualified buyers not being able to borrow. This time around, it’s a different landscape. We don’t have a subprime lending bubble in the residential housing market. Loans will be processed for good buyers with good credit. Mortgage requirements are tightening a bit, but not to an unreasonable level. Another analytic compares total home equity cashed out in the years 2005-2007 and 2017-2019. People were using their homes “like ATMs” during the former period. The leverage people are putting on their homes has dropped from $824 Billion during 2005-2007 to $232 Billion during 2017-2019. 53.8% of all homes in America have at least 50% equity.

The percentage of median income needed to purchase a median-priced home has dropped from 25.4% in 2006 to 14.8% today. Affordability is in much better shape, largely due to mortgage rates being very low.

The Impact of Unemployment

Concerns about job losses are very real. A breakdown of the April 3 Unemployment Report shows the different sectors affected. 59.5% are from restaurant services and drinking places. The accommodation industry, retail trade, temporary help services, child daycare workers, health care office workers and construction workers make up most of the balance. In other words, these are jobs that should be coming back as soon as these businesses can operate again. It may take some time until people are confident and comfortable enough to get back out there. The next numbers come out on May 8, 2020 and will be discussed during the May HMU.

Unemployment rates and home sales do not seem to have a direct relationship. Current Unemployment Rates were compared to past financial crises. In 1933, during the Great Depression, unemployment rates were at a high of 24.9%. Goldman Sachs is predicting unemployment to be 15% in 2020. They are also predicting that number to go down to 6-8% in 2021, 5% in 2022 and 4% in 2023.

Based on data from the US Department of Labor accessed by Haver Analysis, the current employment situation is more like a natural disaster than a recession. The problem is how long this natural disaster, Covid19, is going to last. There are many unknowns, and no answers. We’ll be tracking what happens as parts of the economy reopen.

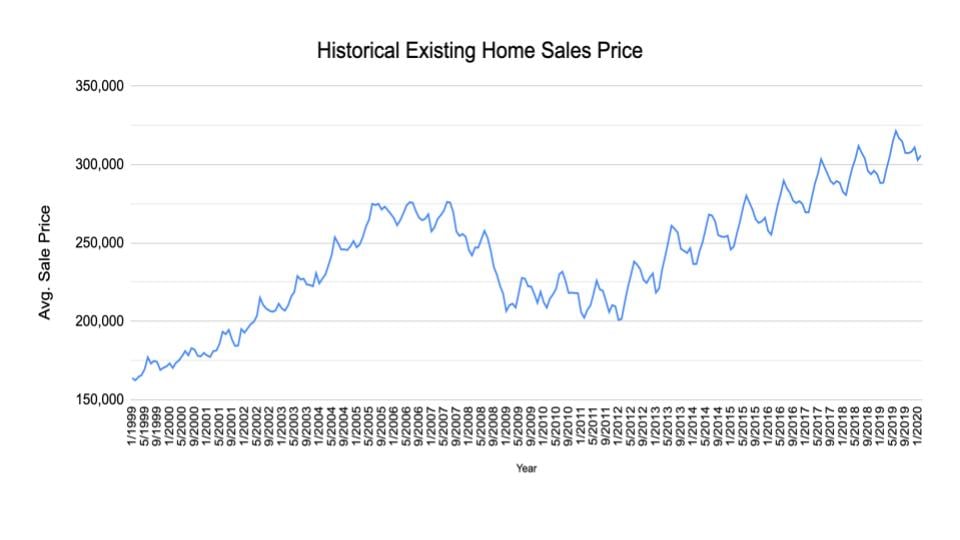

Historical look at Existing Home Sales Price

The market was hot the first two months of 2020, with average home sale price higher in January and February than those months in the preceding four years. It will be interesting to see what the numbers show over the next several months.

The above analytic shows Existing Home Sales Prices from January 1999 to January 2020. Even if you bought at the peak of 2007 or 2008, as Geoff did, just before the housing market plunged, it took 8 years for the market to recover. Historically speaking, people moved after an average of 6 years. That number is now inching up to 9 years. The average homeowner generally doesn’t buy or sell during a period of up or down. They want to wait and gain equity in their home. However, if you are not going to buy, what will you do? Rent? If so, you’re not building equity, you’re not getting tax write-offs, and other benefits of home ownership.

Inventory

In 2007, there were 8.2 months of inventory. Right now there are 3.1 months of inventory available. The market is much hotter now than in 2007 (leading into the Great Recession). Geoff believes that now is a very good time to buy, and not a bad time to sell, either, as inventory levels are so low. Historically, 6 months of supply is an average market. We are now down to 3 months of inventory. He does not see this number climbing anytime soon. Many sellers are not putting their homes on the market now, wanting to wait and see what will be happening. And, while people have to weigh their options, the low inventory can benefit those putting their home on the market.

April 2020 Local Stats

Orange & Sussex Counties

In Orange County, Units Sold were actually better in March than in February. Average Sales Price was way up. In Sussex County, Units Sold and Average Sales Price both coming out at a good solid pace. It will be interesting to see what the stats reflect when we take a look at our next Housing Market Update. At that time we’ll see the impact of Covid closures and stay-at-home regulations.

Housekeeping Items

Panel Discussion

Geoff Green was joined by Ken Flood of Quest Financial Services and Ken Aulicino of Family First Funding LLC. Vikki Garby and Carol Buchanan of Green Team New York Realty and Keren Gonen of Green Team New Jersey Realty represented the real estate agents’ points of view. Discussion ranged from the current state of commercial and residential real estate markets. There was positive feedback on how agents are adapting to the Covid19 regulations and are still able to assist clients and close deals. All three agents spoke of strong, serious buyer interest. Ken Flood discussed the financial market and Ken Aucilino the mortgage industry. Because of the wealth of information and graphics as well as the fascinating panel discussion, it is highly recommended that you watch the webinar. Click here to view the April 2020 Housing Market Update.

Remember to sign up below for the next Housing Market Update

[/et_pb_text][et_pb_agentfire_lead_form form=”contact” _builder_version=”3.18.2″][/et_pb_agentfire_lead_form][/et_pb_column][/et_pb_row][/et_pb_section]

How Technology is Helping Buyers Navigate the Home Search Process [INFOGRAPHIC]

[et_pb_section fb_built=”1″ _builder_version=”3.0.47″][et_pb_row _builder_version=”3.0.48″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.0.74″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]

![How Technology is Helping Buyers Navigate the Home Search Process [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2020/04/16133213/20200417-MEM-Eng-1046x1308.png)

Some Highlights:

- A recent realtor.com survey revealed that buyers are still considering moving forward with the homebuying process, even if they can’t see the home in-person.

- While they still prefer to physically see a home, virtual home tours and accurate listing information top the list of tech specs buyers find most helpful in today’s process.

- Connect today with one of our agents to determine how technology can help power your home search.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section fb_built=”1″ _builder_version=”3.18.2″][et_pb_row _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_post_nav title_font_size=”15px” border_radii=”on|2px|2px|2px|2px” _builder_version=”3.18.2″ title_font=”|800|||||||” border_color_all=”#007a42″ custom_padding=”1px|4px|1px|4px” title_text_color=”#ffffff” border_width_all=”2px” background_color=”#007a42″ in_same_term=”on”][/et_pb_post_nav][/et_pb_column][/et_pb_row][/et_pb_section]