Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Real Estate Consistently Voted Best Investment [INFOGRAPHIC]

![Real Estate Consistently Voted Best Investment [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/06/30083243/20220701-MEM-1046x2020.png)

Some Highlights

- Based on a recent Gallup poll, real estate has been rated the best long-term investment for nine years in a row.

- Owning real estate is more than just a place to call home. It’s also an investment in your future. That’s because it’s typically a stable and secure asset that can grow in value over time.

- If you’re ready to buy a home and invest in your future, let’s connect.

Is the Housing Market Correcting?

If you’re following the news, all of the headlines about conditions in the current housing market may leave you with more questions than answers. Is the boom over? Is the market crashing or correcting? Here’s what you need to know.

The housing market is moderating compared to the last two years, but what everyone needs to remember is that the past two years were record-breaking in nearly every way. Record-low mortgage rates and millennials reaching peak homebuying years led to an influx of buyer demand. At the same time, there weren’t enough homes available to purchase thanks to many years of underbuilding and sellers who held off on listing their homes due to the health crisis.

This combination led to record-high demand and record-low supply, and that wasn’t going to be sustainable for the long term. The latest data shows early signs of a shift back to the market pace seen in the years leading up to the pandemic – not a crash nor a correction. As realtor.com says:

“The housing market is at a turning point. . . . We’re starting to see signs of a new direction, . . .”

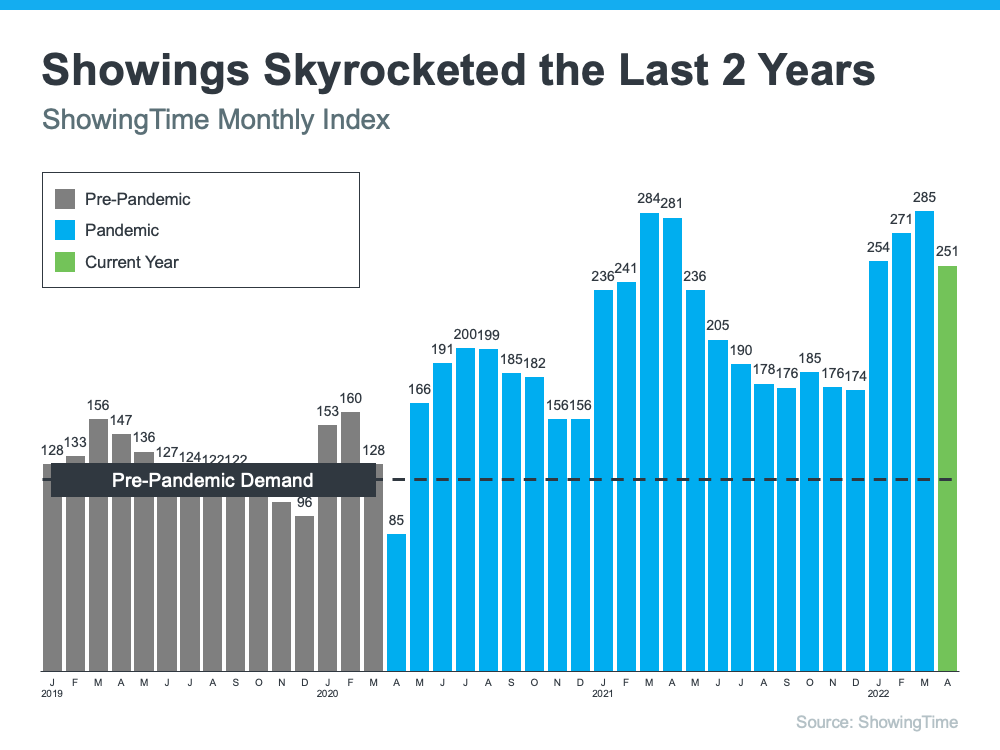

Home Showings Then and Now

The ShowingTime Showing Index tracks the traffic of home showings according to agents and brokers. It’s a good indication of buyer demand. Here’s a look at that data going back to 2019 (see graph below):

The 2019 numbers give a good baseline of pre-pandemic demand (shown in gray). As the graph indicates, home showings skyrocketed during the pandemic (shown in blue). And while current buyer demand has begun to moderate slightly based on the latest data (shown in green), showings are still above 2019 levels.

And since 2019 was such a strong year for the housing market, this helps show that the market isn’t crashing – it’s just at a turning point that’s moving back toward more pre-pandemic levels.

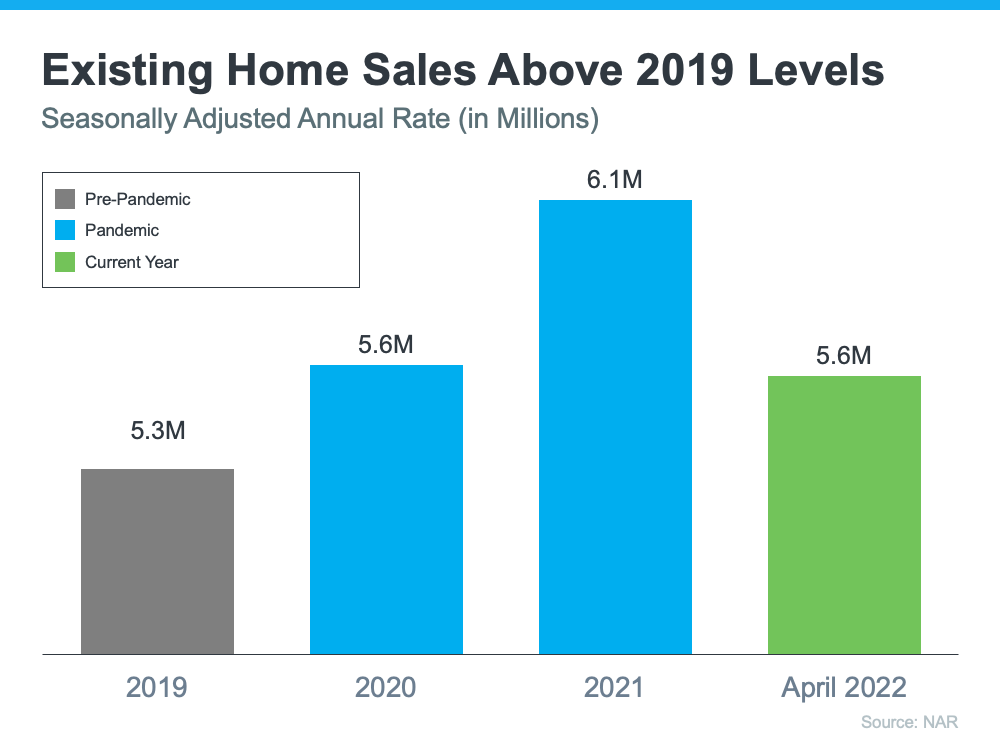

Existing Home Sales Then and Now

Headlines are also talking about how existing home sales are declining, but perspective matters. Here’s a look at existing home sales going all the way back to 2019 using data from the National Association of Realtors (NAR) (see graph below):

Again, a similar story emerges. The pandemic numbers (shown in blue) beat the more typical year of 2019 home sales (shown in gray). And according to the latest projections for 2022 (shown in green), the market is on pace to close this year with more home sales than 2019 as well.

It’s important to compare today not to the abnormal pandemic years, but to the most recent normal year to show the current housing market is still strong. First American sums it up like this:

“. . . today’s housing market looks a lot like the 2019 housing market, which was the strongest housing market in a decade at the time.”

Bottom Line

If recent headlines are generating any concerns, look at a more typical year for perspective. The current market is not a crash or correction. It’s just a turning point toward more typical, pre-pandemic levels. Let’s connect if you have any questions about our local market and what it means for you when you buy or sell this year.

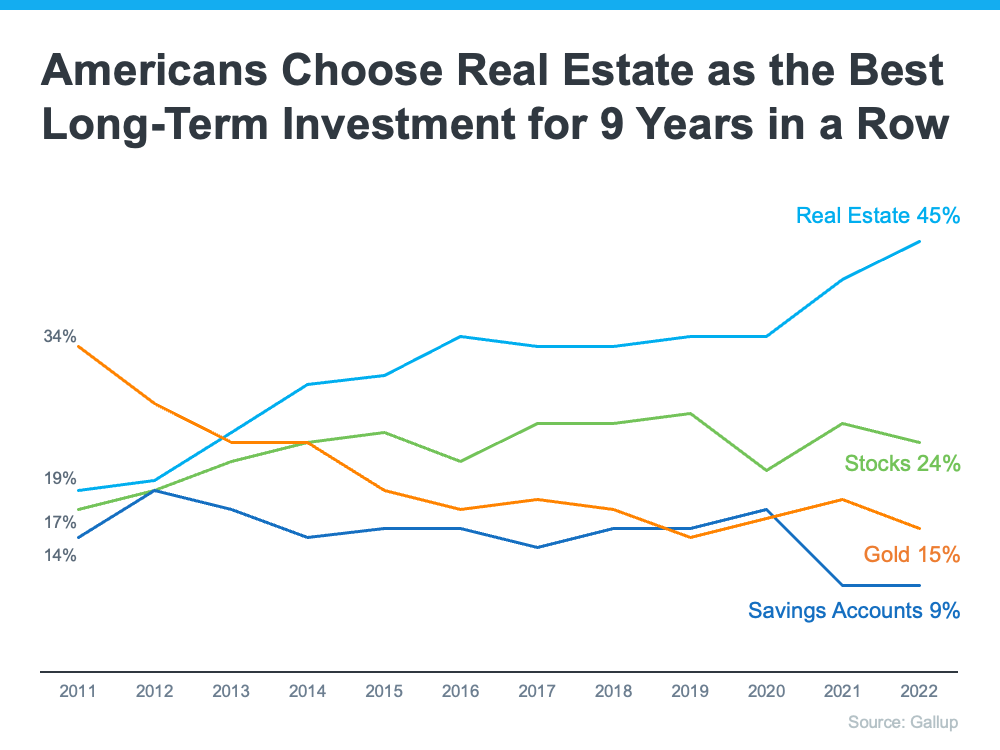

More Americans Choose Real Estate as the Best Investment Than Ever Before

Americans’ opinion on the value of real estate as an investment is climbing. That’s according to an annual survey from Gallup. Not only is real estate viewed as the best investment for the ninth year in a row, but more Americans selected it than ever before.

The graph below shows the results of the survey since Gallup began asking the question in 2011. As the trend lines indicate, real estate has been gaining ground as the clear favorite for almost a decade now:

If you’re thinking about purchasing a home, let this poll reassure you. Even when inflation is high like today, Americans recognize owning a home is a powerful financial decision.

How an Investment in Real Estate Can Benefit You During High Inflation

Because inflation reached its highest level in 40 years recently, it’s more important than ever to understand the financial benefits of homeownership. Rising inflation means prices are increasing across the board, and that includes goods, services, housing costs, and more. When you purchase your home, you lock in your monthly housing payments, effectively shielding yourself from increases on one of your biggest budgetary items each month.

If you’re a renter, you don’t have that same benefit, and you aren’t protected from these increases, especially as rents rise. As Danielle Hale, Chief Economist at realtor.com, notes:

“Rising rents, which continue to climb at double-digit pace . . . and the prospect of locking in a monthly housing cost in a market with widespread inflation are motivating today’s first-time homebuyers.”

When Inflation Has Risen in the Past, Home Prices Have Too

Your house is also an asset that typically increases in value over time, even during inflation. That‘s because as prices rise, the value of your home does too. Mark Cussen, Financial Writer for Investopedia, puts it like this:

“There are many advantages to investing in real estate. . . . It often acts as a good inflation hedge since there will always be a demand for homes, regardless of the economic climate, and because as inflation rises, so do property values. . . .”

And since rising home values help increase your equity, and by extension your net worth, homeownership is historically a good hedge against inflation.

Bottom Line

Buying a home is a powerful decision. It’s no wonder why so many people view it as the best long-term investment, even when inflation is high. When you buy, you help shield yourself from increases in your housing costs and you own an asset that typically gains value with time. If you want to better understand how buying a home could be a great investment for you, let’s connect today.

History Proves Recession Doesn’t Equal a Housing Crisis [INFOGRAPHIC]

![History Proves Recession Doesn’t Equal a Housing Crisis [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/06/02165354/20220603-MEM-2-1046x1949.png)

Some Highlights

- It’s important to understand history proves an economic slowdown does not equal a housing crisis.

- In 4 of the last 6 recessions, home prices actually appreciated. Home prices only fell twice – minimally in the early 90s and then by nearly 20% during the housing crash in 2008.

- If you have questions, let’s connect to discuss why today’s housing market is nothing like 2008.

May 2022 Housing Market Update

Geoff Green, the moderator of the monthly Housing Market webinar, is a real estate expert and entrepreneur. And, he is joined for the May 2022 Housing Market Update by Keren Gonen, Green Team New Jersey Realty; Vikki Garby, Green Team New York Realty; Chad Barris, Family First Funding, and Ken Ford, Warwick Valley Financial Advisors.

If you haven’t seen the May 2022 Housing Market Update yet or would like to watch it again, it’s available below. In addition, the Housing Market News section of the Green Team Realty website includes prior HMU recap blogs.

Furthermore, you can sign up to receive updates at HMupdate.com.

The big question… Are we headed for a Housing Bubble?

Of course, it would be wonderful if the panel was able to provide a simple “Yes” or “No” answer. However, there are too many variables to predict whether or not we are headed toward a Housing Bubble.

At each monthly Housing Market Update, Geoff asks mortgage experts if they are seeing a return to the lending practices that contributed to the 2008 housing market crash. To date, there has been no such return to those lending standards.

Furthermore, Geoff shares stats that may impact the answer to the Housing Bubble question. This includes home price appreciation and performance. Also, foreclosure activity is now at an all-time low.

“Housekeeping” Items

The June Housing Market Update will take place on Friday, June 17. Sign up now at HMupdate.com. Again, thanks to NuOp, Sponsor of the Housing Market Update.

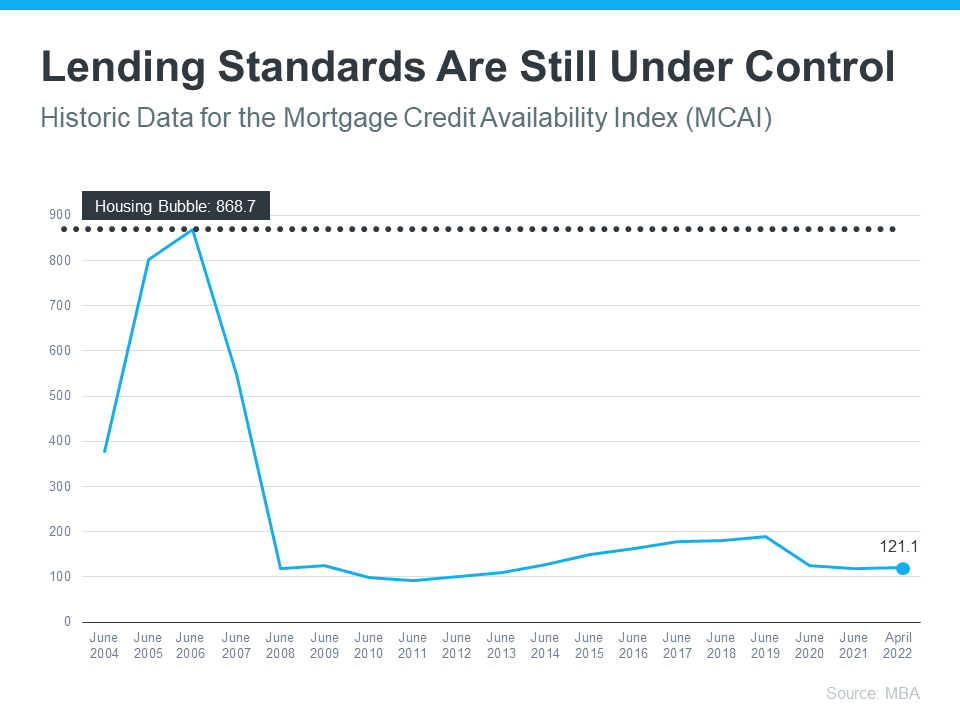

Why Home Loans Today Aren’t What They Were in the Past

In today’s housing market, many are beginning to wonder if we’re returning to the riskier lending habits and borrowing options that led to the housing crash 15 years ago. Let’s ease those concerns.

Several times a year, the Mortgage Bankers Association (MBA) releases an index titled the Mortgage Credit Availability Index (MCAI). According to their website:

“The MCAI provides the only standardized quantitative index that is solely focused on mortgage credit. The MCAI is . . . a summary measure which indicates the availability of mortgage credit at a point in time.”

Basically, the index determines how easy it is to get a mortgage. The higher the index, the more available mortgage credit becomes. Here’s a graph of the MCAI dating back to 2004, when the data first became available:

As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006.

As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006.

Why Did the Index Get out of Control During the Housing Bubble?

The main reason was the availability of loans with extremely weak lending standards. To keep up with demand in 2006, many mortgage lenders offered loans that put little emphasis on the eligibility of the borrower. Lenders were approving loans without always going through a verification process to confirm if the borrower would likely be able to repay the loan.

An example of the relaxed lending standards leading up to the housing crash is the FICO® credit score associated with a loan. What’s a FICO® score? The website myFICO explains:

“A credit score tells lenders about your creditworthiness (how likely you are to pay back a loan based on your credit history). It is calculated using the information in your credit reports. FICO® Scores are the standard for credit scores—used by 90% of top lenders.”

During the housing boom, many mortgages were written for borrowers with a FICO score under 620. While there are still some loan programs that allow for a 620 score, today’s lending standards are much tighter. Lending institutions overall are much more attentive about measuring risk when approving loans. According to the latest Household Debt and Credit Report from the New York Federal Reserve, the median credit score on all mortgage loans originated in the first quarter of 2022 was 776.

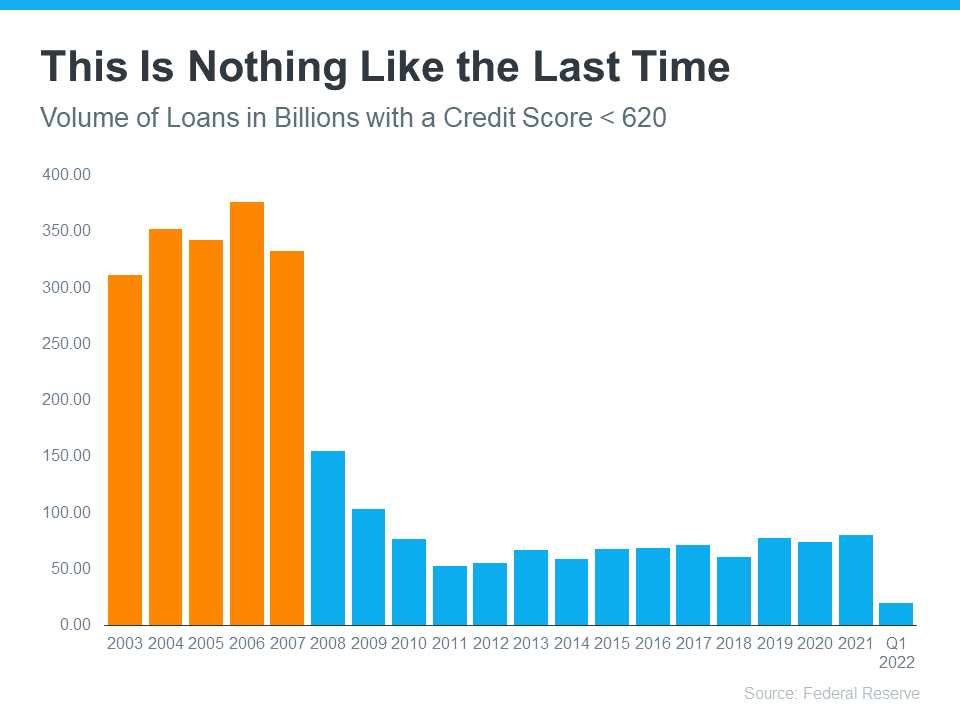

The graph below shows the billions of dollars in mortgage money given annually to borrowers with a credit score under 620.

In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

Bottom Line

In 2006, lending standards were much more relaxed with little evaluation done to measure a borrower’s potential to repay their loan. Today, standards are tighter, and the risk is reduced for both lenders and borrowers. These are two very different housing markets, and today is nothing like the last time.

Don’t Let Rising Inflation Delay Your Homeownership Plans [INFOGRAPHIC]

![Don’t Let Rising Inflation Delay Your Homeownership Plans INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/05/18153723/20220520-MEM-1046x2334.png)

Some Highlights

- If recent headlines about rising inflation are making you wonder if it’s still a good time to buy, here’s what experts have to say.

- Housing is an asset that typically grows in value. Plus, your mortgage helps stabilize your monthly housing costs, and buying protects you from rising rents.

- Experts say owning a home is historically a good hedge against inflation. Let’s connect if you’re ready to start the homebuying process today.

The One Thing Every Homeowner Needs To Know About a Recession

A recession does not equal a housing crisis. That’s the one thing that every homeowner today needs to know. Everywhere you look, experts are warning we could be heading toward a recession, and if true, an economic slowdown doesn’t mean homes will lose value.

The National Bureau of Economic Research (NBER) defines a recession this way:

“A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.”

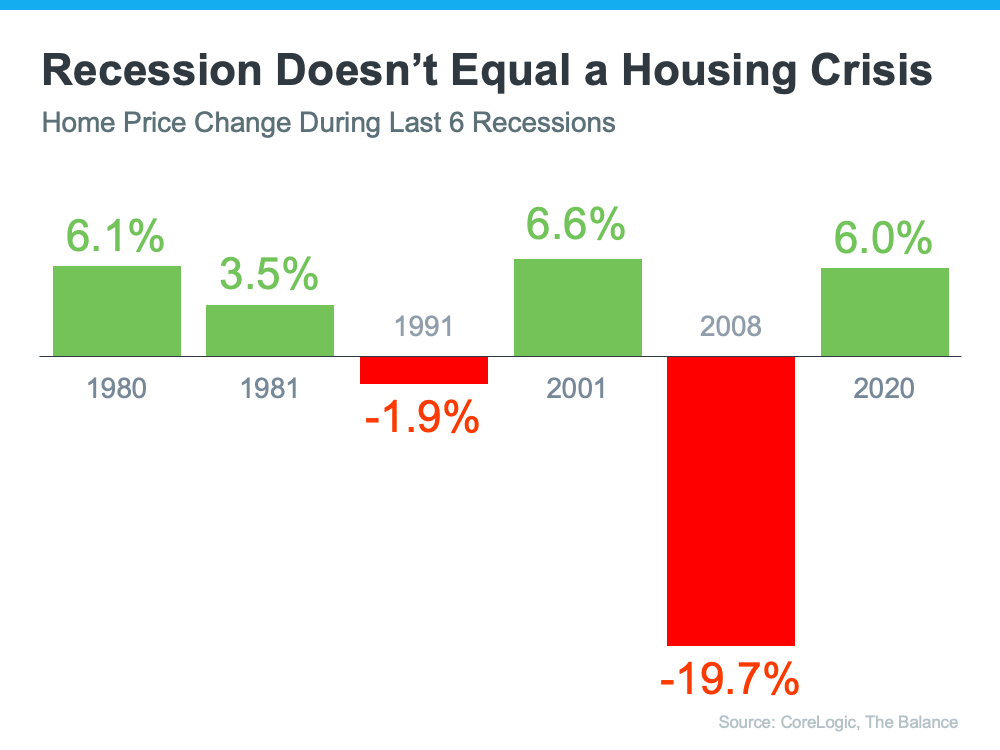

To help show that home prices don’t fall every time there’s a recession, take a look at the historical data. There have been six recessions in this country over the past four decades. As the graph below shows, looking at the recessions going all the way back to the 1980s, home prices appreciated four times and depreciated only two times. So, historically, there’s proof that when the economy slows down, it doesn’t mean home values will fall or depreciate.

The first occasion on the graph when home values depreciated was in the early 1990s when home prices dropped by less than 2%. It happened again during the housing crisis in 2008 when home values declined by almost 20%. Most people vividly remember the housing crisis in 2008 and think if we were to fall into a recession that we’d repeat what happened then. But this housing market isn’t a bubble that’s about to burst. The fundamentals are very different today than they were in 2008. So, we shouldn’t assume we’re heading down the same path.

Bottom Line

We’re not in a recession in this country, but if one is coming, it doesn’t mean homes will lose value. History proves a recession doesn’t equal a housing crisis.

Three Tips for First-Time Homebuyers

Buying your first home is a major decision and an exciting milestone. Even though it can feel daunting at times, it has the power to change your life for the better. If you’re looking to purchase your first home, you may be wondering what’s happening in the housing market today, how much you need to save, and where to start.

Here are three things that can help give you the information you need to confidently pursue your dream of homeownership.

1. Consider All Options When the Number of Homes for Sale Is Low

Today, there are far more buyers in the market than there are homes available for sale. When that happens, it’s a good idea to do what you can to increase your pool of options. That could mean expanding your search to include additional housing types. For first-time buyers, considering condominiums (condos) and townhomes can be an excellent way to increase your choices. According to Bankrate:

“Townhomes often cost less than single-family homes of a similar size in the same location.”

In another article, Bankrate also says:

“Buying a condo can be a great way to dive into homeownership without worrying about the upkeep that comes with single-family homes and townhouses.”

Condos and townhomes are both great entryways into homeownership. When you buy either one, you can start building equity which increases your net worth and can fuel a future move.

2. Know Your Down Payment Could Be More Within Reach Than You Think

Saving for a down payment can feel like one of the biggest obstacles for homebuyers, but that doesn’t have to be the case. As the National Association of Realtors (NAR) says:

“One of the biggest misconceptions among housing consumers is what the typical down payment is and what amount is needed to enter homeownership.”

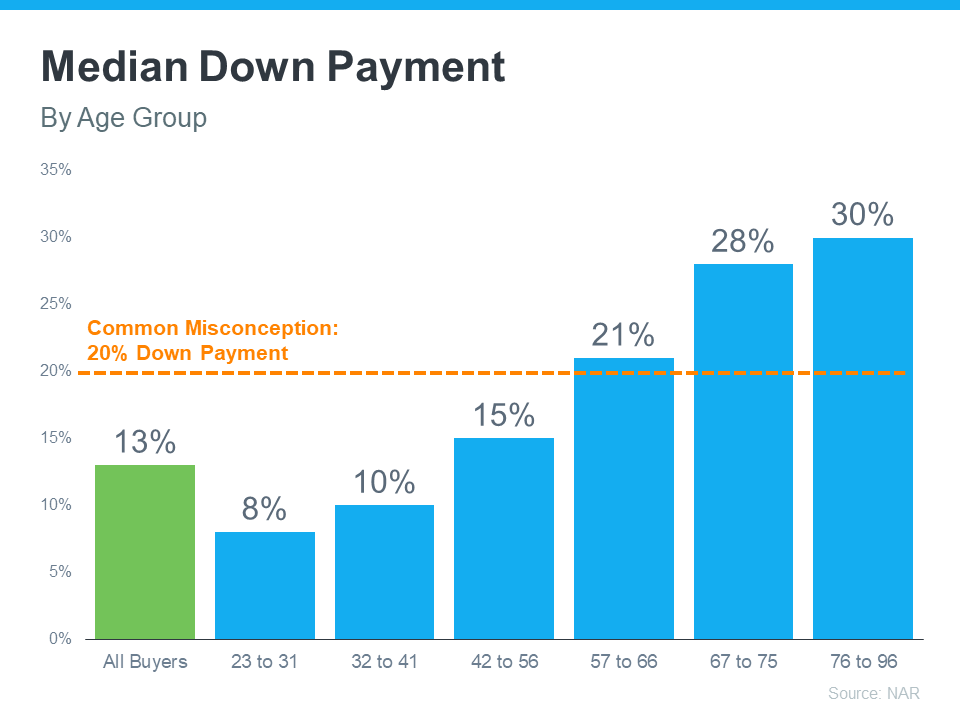

Data from NAR shows the median down payment hasn’t been over 20% since 2005. The graph below breaks down the median down payment by age group for recent homebuyers according to the 2022 Home Buyers and Sellers Generational Trends Report from NAR (see graph below):

Based on the data above, the median down payment for all homebuyers is only 13%. That’s well below the common misconception of 20%, and it’s even lower for younger buyers. This could mean you may not need to save as much for a down payment as you initially thought.

There are also down payment assistance programs available for many buyers. Not to mention, some loan options require as little as 3.5% (or even 0%) down for buyers who qualify. While there are advantages to putting 20% down, especially in today’s competitive market, know that you have options. To get more information on how much you may need to save and the help that’s available, talk with a professional.

3. Work with a Trusted Real Estate Advisor Throughout the Process

Finally, no matter where you’re at in your homeownership journey, the best way to make sure you’re set up for success is to work with a real estate professional.

If you’re just starting out, they can help you with the initial steps, like educating you on the process and connecting you with a trusted lender to get pre-approved. Once you’re ready to begin your search, a real estate professional can help you understand your local market and search for available homes. And when it’s time to make an offer, they’ll be an expert advisor and negotiator to help your offer stand out above the rest.

Bottom Line

Knowledge is key to succeeding on your homebuying journey. Knowing market trends, what you need for a down payment, and what options you have as a buyer today can give you the confidence you need to buy a home. Let’s connect so you have an expert on your side who can help you navigate the homebuying process.

Today’s Home Price Appreciation Is Great News for Existing Homeowners

If you’re planning to sell your home this season, rising prices are great news for you. But it’s important to understand why prices are rising to begin with. One major factor is supply and demand.

In any industry, when there are more buyers for an item than there are of that item available, prices naturally rise. In those situations, buyers are willing to pay more to get the product or service they’re looking for when options are scarce. And that’s exactly what’s happening in the current real estate market.

Selma Hepp, Executive, Research & Insights and Deputy Chief Economist at CoreLogic, puts it like this:

“With so few homes, buyers are once again left with fierce competition that’s driving the share of homes that sold over the listing price up to 66% . . . With the continued imbalance between supply and demand, home prices are likely to have another year of strong gains and are expected to average about 10% growth for the year.”

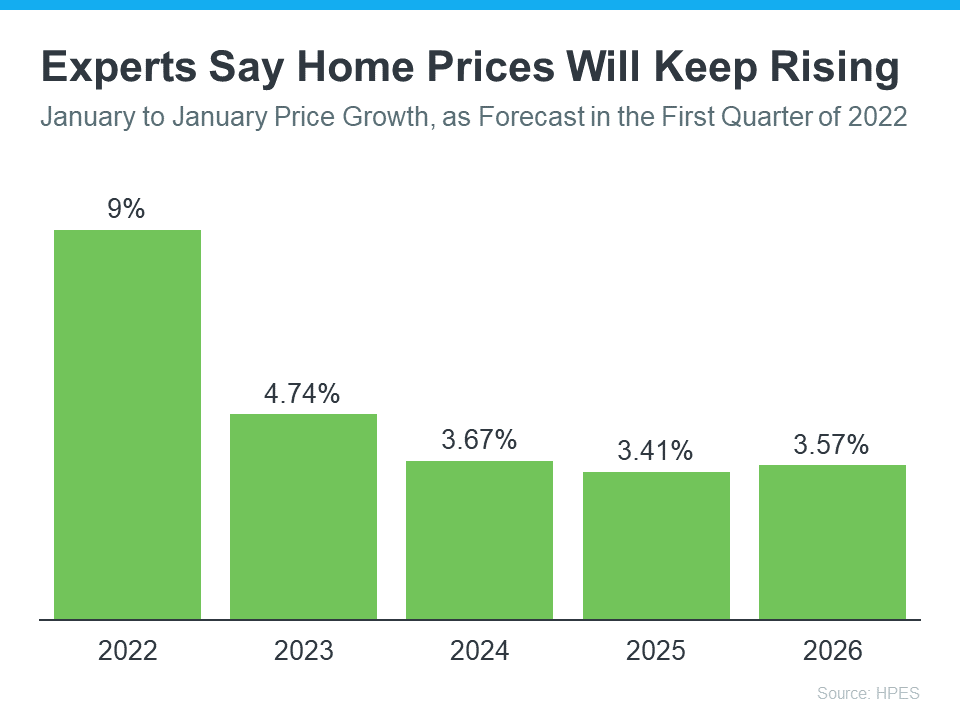

Because it will take some time for housing supply to increase, experts believe prices will continue rising. The latest Home Price Expectations Survey forecasts what will happen with home prices over the next 5 years. As the graph below shows, while the rate of appreciation will moderate over the next few years, prices will continue rising through 2026:

What This Means When You Sell Your House

If you’re a homeowner, the projection for continued price appreciation this year opens up an opportunity to move. That’s because it may give your equity a major boost. Equity is the difference between what you owe on your house and its market value. The amount of equity you have increases as you make your monthly payments and as rising home prices drive up the market value for your home.

Growing equity is a powerful tool for homeowners. When you sell your house, the equity you’ve built comes back to you in the sale. That money could be enough to cover some (if not all) of your down payment on your next home.

Of course, if you want to know how much equity you have in your current house, it’s crucial to work with a real estate professional. They follow current market trends and can help you understand your home’s value when you’re ready to sell.

What This Means for Your Next Purchase

But today’s rising home values aren’t just good news if you’re ready to sell. Because price appreciation is forecast to continue in the years ahead, you can rest assured your next home will be an investment that should grow in value with time. That’s one of several reasons why real estate has been rated the best investment in a recent Gallup poll.

Bottom Line

If you’re weighing whether or not you should sell your house this season, know rising home values may be opening up an opportunity to use equity to fuel your move. Let’s connect so you can find out how much your home is worth and to learn more about all the benefits you have in today’s market.