Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

March 2022 Housing Market Update

Welcome to the March 2022 Housing Market Update. Geoff Green, President of Green Team Realty and Co-Founder and CEO of NuOp, is the host of the March 15 webinar. If you missed it, the video of the webinar is available below.

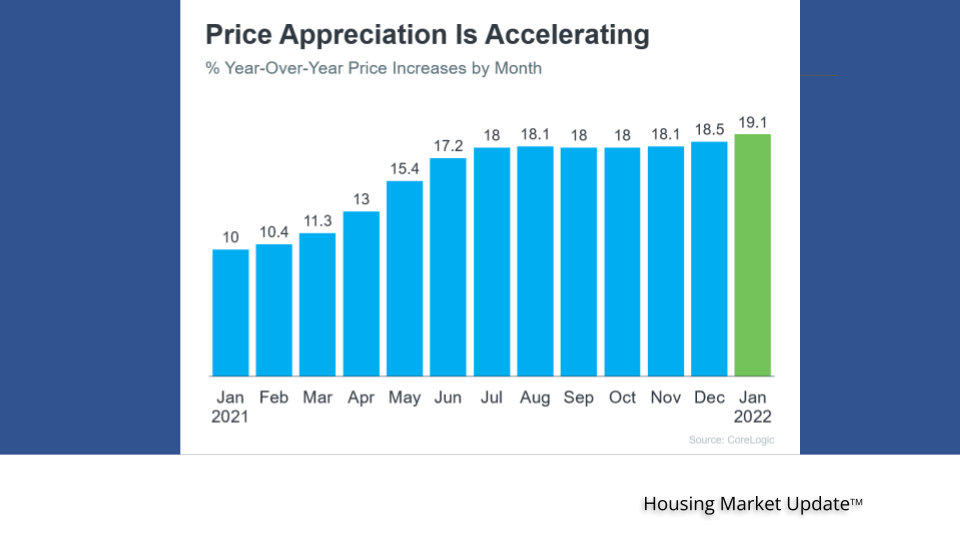

Price appreciation

As shown here, there is an acceleration again in price appreciation. For a while, we were talking about it decelerating (not depreciating). According to Geoff, inventory is just so low that pricing has nowhere to go but up.

In addition. the major forecasting agencies show an average of 6.1% increase for 2022. The average annual home price forecast has usually been around 4% per year.

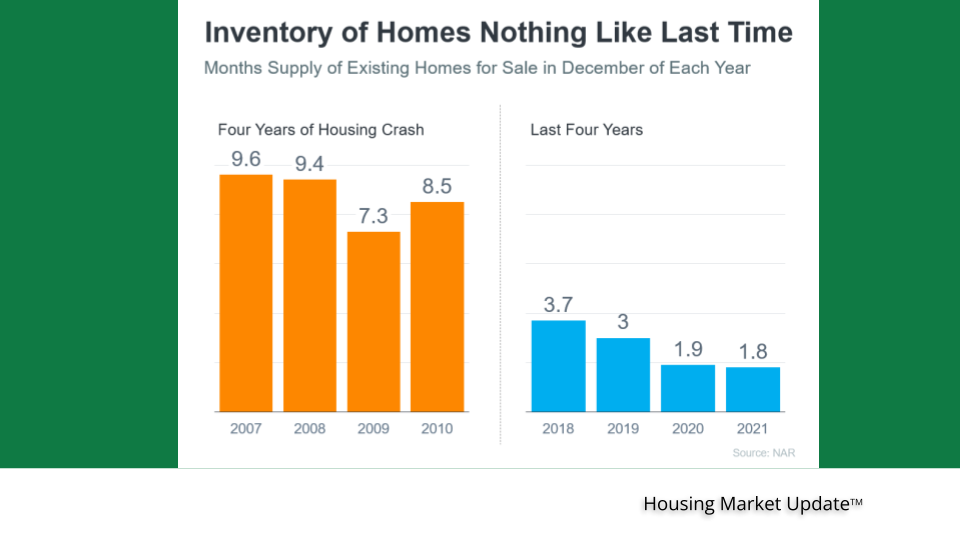

Supply and Demand

Basically, inventory is a subject that the Housing Market Update has discussed for several years. A Sellers’ Market is defined as having less than 6 months’ inventory. Home prices will appreciate. A neutral market, during which prices appreciate with inflation, is 6-7 months inventory. A Buyers’ Market, with over 7 months of inventory, will see home prices depreciating.

In addition, worries of a housing bubble persist among 77% of consumers and 44% of agents. However, there is a big difference in factors, including inventory supply as shown below.

Keeping an eye on other factors…

According to Mark Zandi, Moody’s Analytics Chief Economist,

“Recession risks later this year and into next are now uncomfortably high.” “The odds that the Fed missteps and tightens too aggressively are material and rising. Landing the economic plane on the tarmac was already going to be difficult for the Fed because of the pandemic and high inflation, but Russia’s invasion makes it more likely the economic plane hits the tarmac hard or even crashes.”

The Housing Market Update will continue to keep an eye on this. However, Geoff reminded viewers that a recession does not necessarily lead to a bad housing market.

Meet the Panel

Joining Geoff for this March 2022 Housing Market Update are Keren Gonen, Green Team New Jersey Realty, and Peter Mallon, Americana Mortgage Group, Inc. The panel discussed the issues and data presented by Geoff as it relates to what they are experiencing in their own businesses. To watch the webinar and view the panel discussion, click here. You’ll find contact information for the panelists below:

“Housekeeping” Items

The Top Indicator if You Want To Know Where Mortgage Rates Are Heading

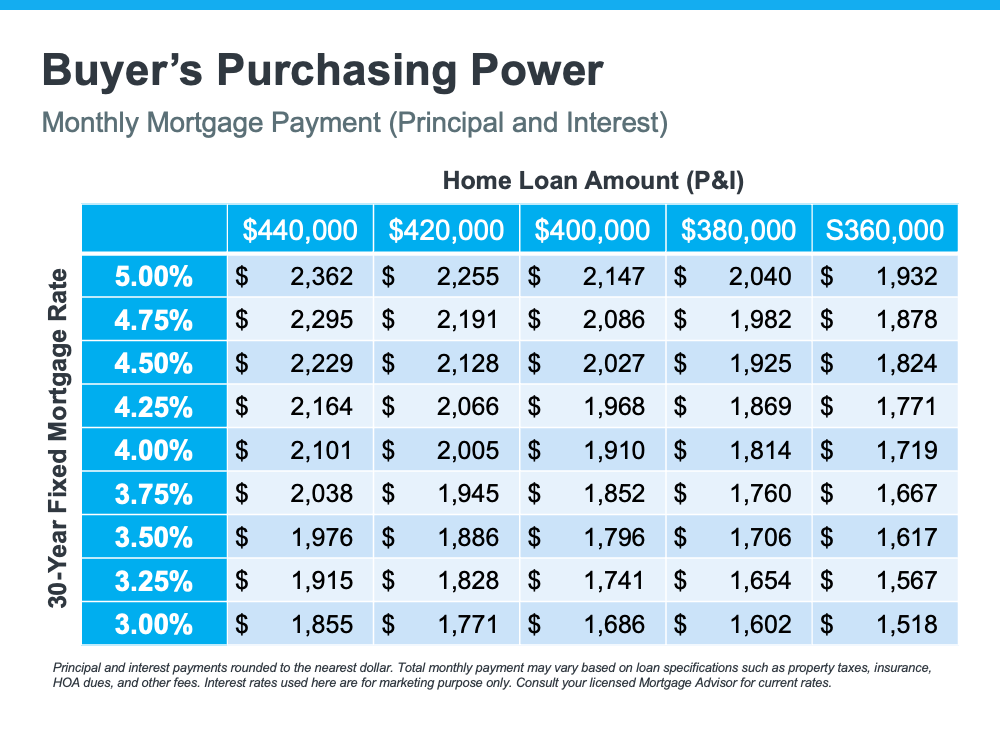

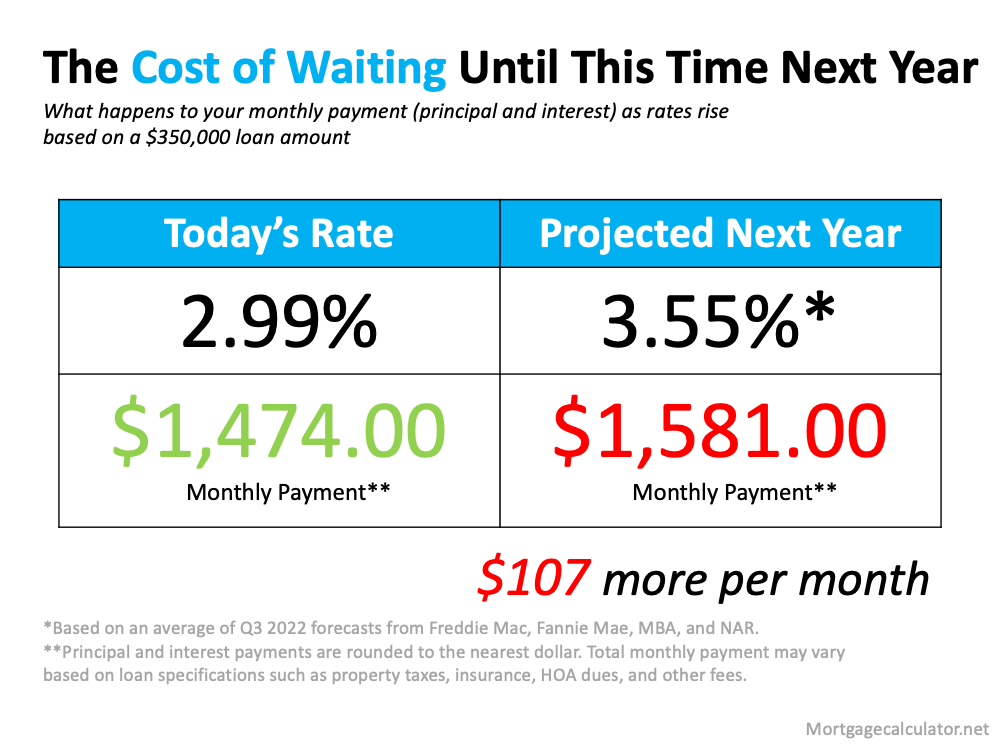

Mortgage rates have increased significantly since the beginning of the year. Each Thursday, Freddie Mac releases its Primary Mortgage Market Survey. According to the latest survey, the average 30-year fixed-rate mortgage has risen from 3.22% at the start of the year to 3.55% as of last week. This is important to note because any increase in mortgage rates changes what a purchaser can afford. To give you an idea of how rising mortgage rates impact your purchasing power, see the table below:

How Can You Know Where Mortgage Rates Are Headed?

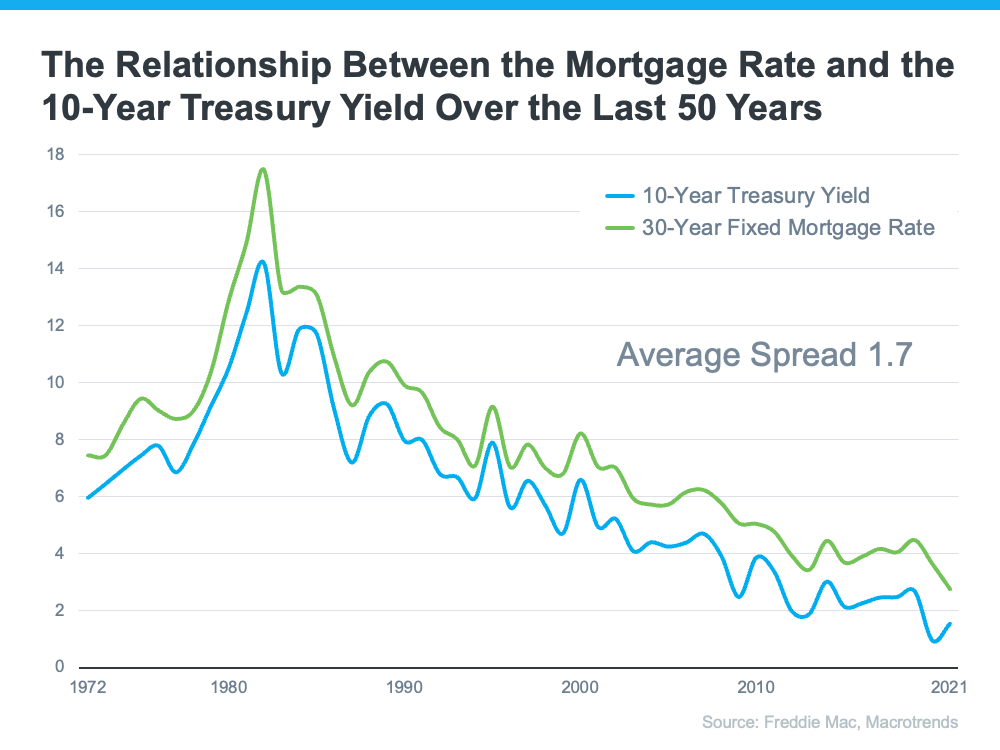

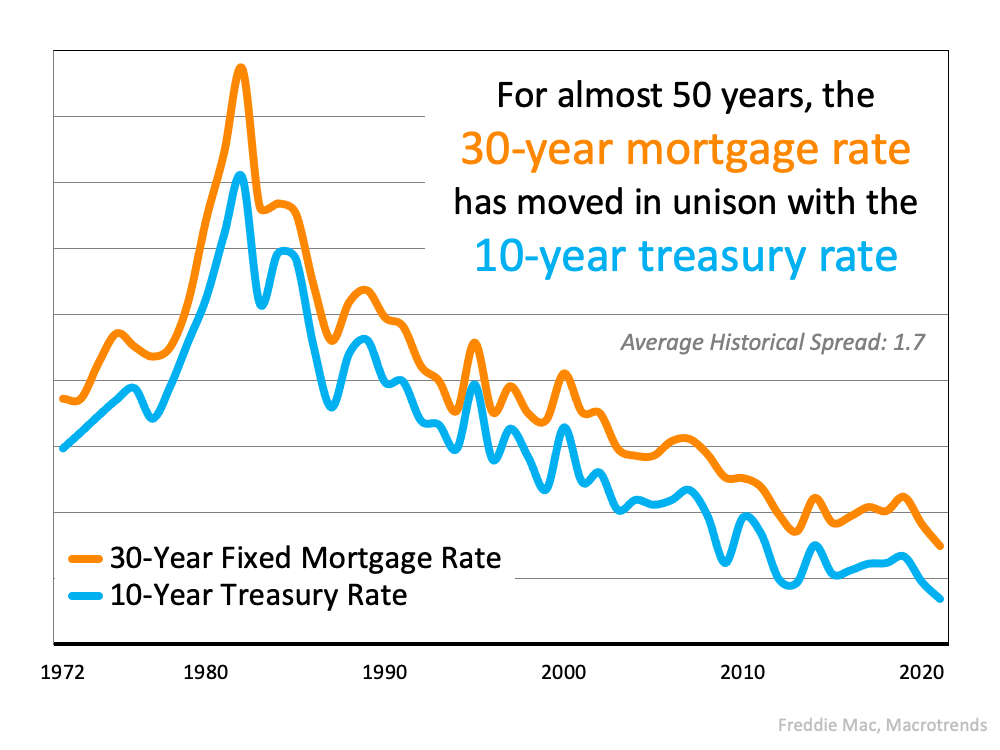

While it’s always difficult to know exactly where mortgage rates will go, a great indicator of where they may head is by looking at the 50-year history of the 10-year treasury yield, and then following its path. Understanding the mechanics of the treasury yield isn’t as important as knowing that there’s a correlation between how it moves and how mortgage rates follow. Here’s a graph showing that relationship over the last 50 years:

This correlation has continued into the new year. The treasury yield has started to climb, and that’s driven rates up. As of last Thursday, the treasury yield was 1.81%. That’s 1.74% below the mortgage rate reported the same day (3.55%) and is very close to the average spread we see between the two numbers (average spread is 1.7).

Where Will the Treasury Yield Head in the Future?

With this information in mind, a 10-year treasury-yield forecast would be a good indicator of where mortgage rates may be headed. The Wall Street Journal just surveyed a panel of over 75 academic, business, and financial economists asking them to forecast the treasury yield over the next few years. The consensus was that experts project the treasury yield will climb to 2.84% by the end of 2024. Based on the 50-year history of following this yield, that would likely put mortgage rates at about 4.5% in three years.

While the correlation between the 30-year fixed mortgage rate and the 10-year treasury yield is clear in the data shown above for the past 50 years, it shouldn’t be used as an exact indicator. They’re both hard to forecast, especially in this unprecedented economic time driven by a global pandemic. Yet understanding the relationship can help you get an idea of where rates may be going. It appears, based on the information we have now, that mortgage rates will continue to rise over the next few years. If that’s the case, your best bet may be to purchase a home sooner rather than later, if you’re able.

Bottom Line

Forecasting mortgage rates is very difficult. As Mark Fleming, Chief Economist at First American, once said:

“You know, the fallacy of economic forecasting is don’t ever try and forecast interest rates and or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

However, if you’re either a first-time homebuyer or a current homeowner thinking of moving into a home that better fits your changing needs, understanding what’s happening with the 10-year treasury yield and mortgage rates can help you make an informed decision on the timing of your purchase.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of.

Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams.

What’s your home’s value?

Contact one of Our Agents today!

With Mortgage Rates Climbing, Now’s the Time To Act

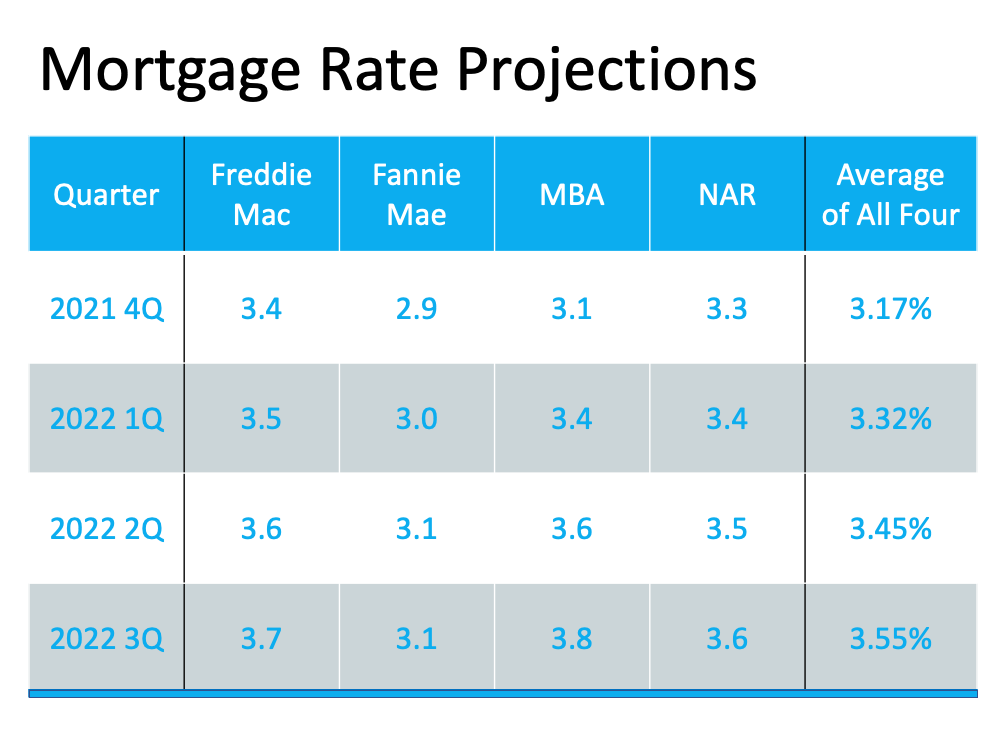

Last week, the average 30-year fixed mortgage rate from Freddie Mac jumped from 3.22% to 3.45%. That’s the highest point it’s been in almost two years. If you’re thinking about buying a home, this news may have come as a bit of a shock. But the truth is, it wasn’t entirely unexpected. Experts have been calling for rates to rise in their 2022 projections, and the forecast is now becoming a reality. Here’s a look at the projections from Freddie Mac for this year:

- Q1 2022: 3.4%

- Q2 2022: 3.5%

- Q3 2022: 3.6%

- Q4 2022: 3.7%

As the numbers show, this jump in rates is in line with the expectations from Freddie Mac. And what they also indicate is that mortgage rates are projected to continue climbing throughout the year. But should you be worried about rising mortgage rates? What does that really mean for you?

As rates increase even modestly, they impact your monthly mortgage payment and overall affordability. If you’re looking to buy a home, rising mortgage rates should be an incentive to act sooner rather than later.

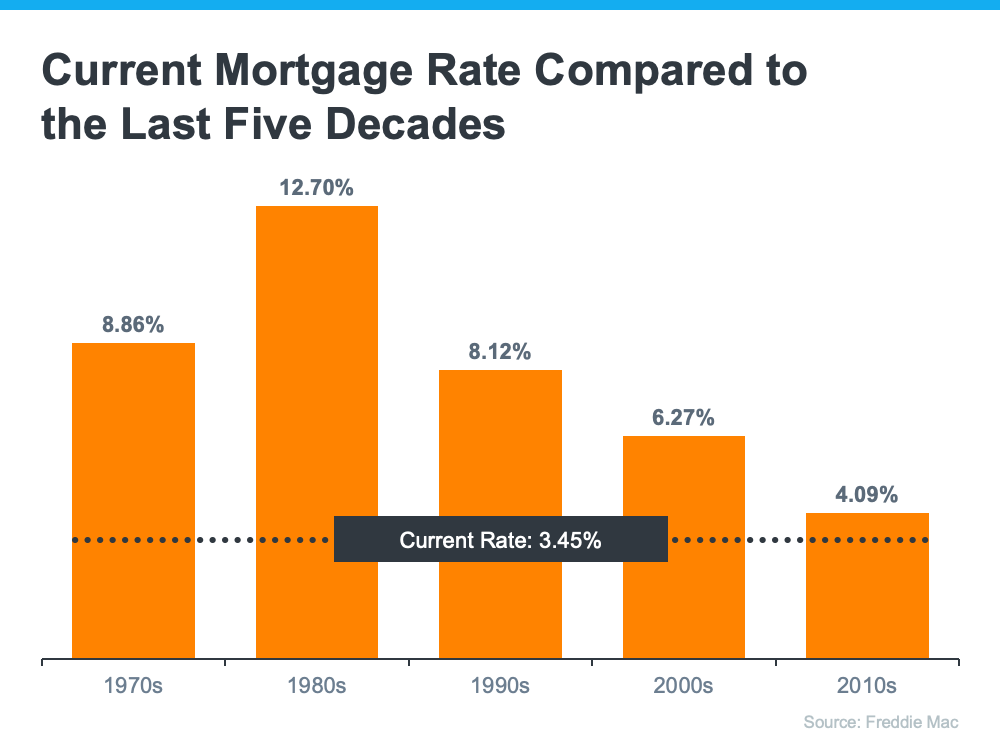

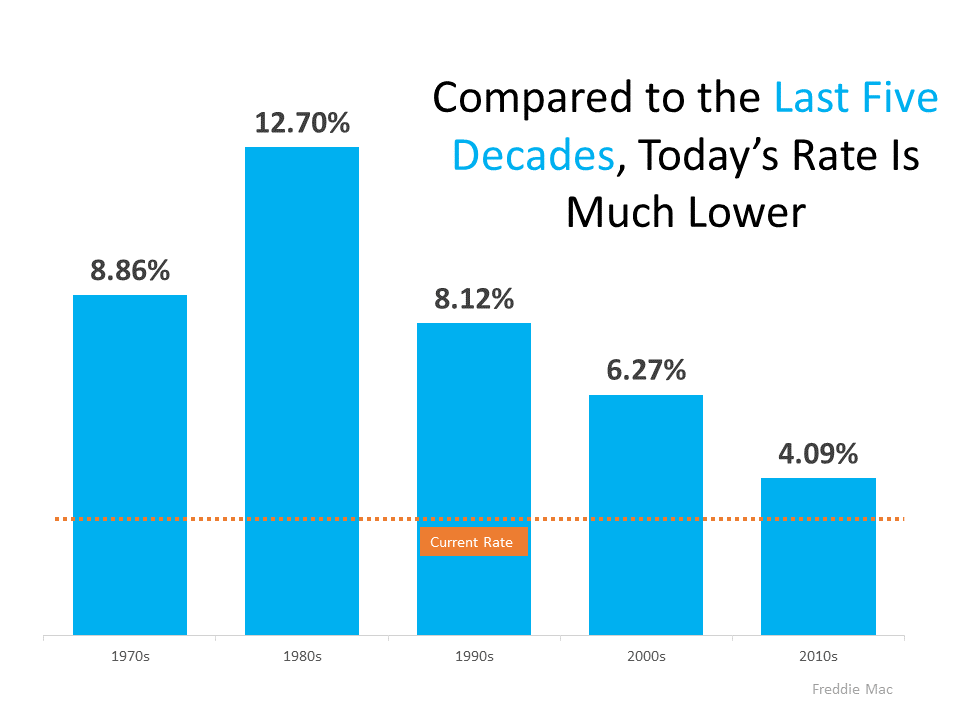

The good news is, even though rates are climbing, they’re still worth taking advantage of. Historical data shows that today’s rate, even at 3.45%, is still well below the average for each of the last five decades (see chart below):

That means you still have a great opportunity to buy now with a rate that’s better than what your loved ones may have paid in decades past. If you buy a home while rates are in the mid-3s, your monthly mortgage payment will be locked in at that rate for the life of your loan. As you can see from the chart above, a lot can change in that time frame. Buying now is a great way to protect yourself from rising costs and future rate increases while also securing your payment amount for the long term.

Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), says:

“Mortgage rates surged in the second week of the new year. The 30-year fixed mortgage rate rose to 3.45% from 3.22% the previous week. If inflation continues to grow at the current pace, rates will move up even faster in the following months.”

Bottom Line

Mortgage rates are increasing, and they’re forecast to be even higher by the end of 2022. If you’re planning to buy this year, acting soon may be your most affordable option. Let’s connect to start the homebuying process today.

Contact one of Our Agents today!

See out Complete Inventory of Available Properties!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams.

What’s your home’s value?

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of.

Start Here!

How Smart Buyers Are Approaching Rising Mortgage Rates

Last week, the average 30-year fixed mortgage rate from Freddie Mac inched up to 3.1%, and experts project rates will continue rising through 2022:

“The 30-year fixed-rate mortgage was 2.9% in the third quarter of 2021. We forecast mortgage rates to increase slightly through the remainder of the year and reach 3.0%, rising to 3.5% for full year 2022.”

If you’re thinking of buying a home, here are a few things to keep in mind so you can succeed even as mortgage rates rise.

Taking Time Off Can Be Costly

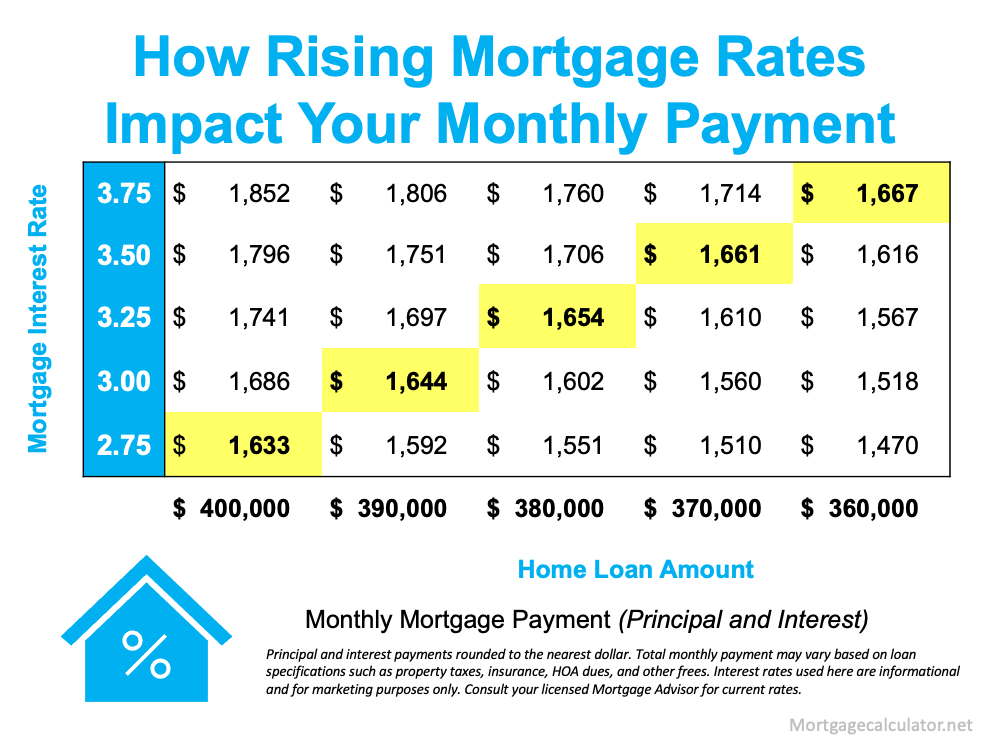

Mortgage rates play a significant role in your home search. As rates go up, your monthly mortgage payment increases if you’re buying a home, directly affecting how much you can afford. And even the smallest increase can have a large impact on your monthly payment (see chart below): With mortgage rates on the rise, you’ve likely seen your purchasing power impacted already. Instead of waiting and hoping rates will fall, today’s rates should motivate you to purchase now before rates increase more.

With mortgage rates on the rise, you’ve likely seen your purchasing power impacted already. Instead of waiting and hoping rates will fall, today’s rates should motivate you to purchase now before rates increase more.

Smart Buyers Can Succeed by Planning Ahead

You can use your newfound motivation to energize your search and plan your next steps accordingly so you’re prepared to act no matter what happens with mortgage rates. One way to do that: take rising rates into consideration as part of your budget.

Danielle Hale, Chief Economist at realtor.com, puts it best, saying:

“Smart buyers should consider calculating a monthly payment not only at today’s rates, but also at rates that are a bit higher so that they won’t be derailed by a sudden upward move. . . .”

You should also be ready to act when you find the home that meets your needs. That means getting pre-approved with a lender so there won’t be any delays when the time arrives.

The best way to prepare is to work with a trusted real estate advisor now. An agent can connect you with a lender, help you adjust your search based on your budget, and be ready to act quickly when it’s time to make an offer.

Bottom Line

Serious buyers should approach rising rates as a motivating factor to buy sooner, not a reason to wait. Waiting will cost you more in the long run. Let’s connect today so you can better understand your budget and be prepared to buy your home even before rates climb higher.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of.

Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams.

What’s your home’s value?

Contact one of Our Agents today!

Two Graphs That Show Why You Shouldn’t Be Upset About 3% Mortgage Rates

With the average 30-year fixed mortgage rate from Freddie Mac climbing above 3%, rising rates are one of the topics dominating the discussion in the housing market today. And since experts project rates will rise further in the coming months, that conversation isn’t going away any time soon.

But as a homebuyer, what do rates above 3% really mean?

Today’s Average Mortgage Rate Still Presents Buyers with a Great Opportunity

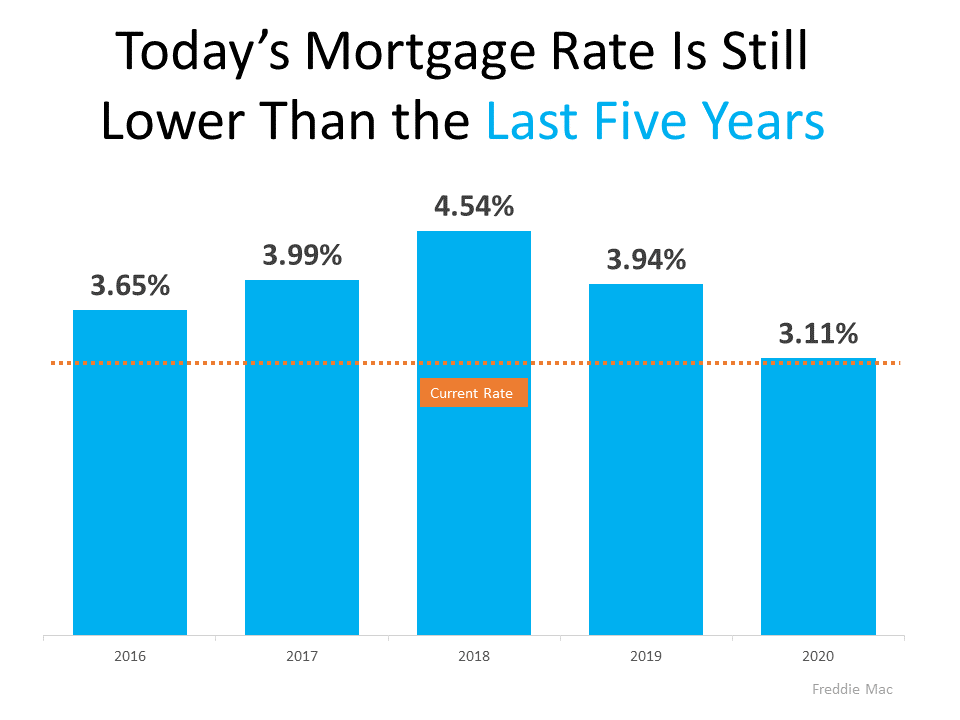

Buyers don’t want mortgage rates to rise, as any upward movement increases your monthly mortgage payment. But it’s important to put today’s average mortgage rate into perspective. The graph below shows today’s rate in comparison to average rates over the last five years: As the graph shows, even though today’s rate is above 3%, it’s still incredibly competitive.

As the graph shows, even though today’s rate is above 3%, it’s still incredibly competitive.

But today’s rate isn’t just low when compared to the most recent years. To truly put today into perspective, let’s look at the last 50 years (see graph below): When we look back even further, we can see that today’s rate is truly outstanding by comparison.

When we look back even further, we can see that today’s rate is truly outstanding by comparison.

What Does That Mean for You?

Being upset that you missed out on sub-3% mortgage rates is understandable. But it’s important to realize, buying now still makes sense as experts project rates will continue to rise. And as rates rise, it will cost more to purchase a home.

As Mark Fleming, Chief Economist at First American, explains:

“Rising mortgage rates, all else equal, will diminish house-buying power, meaning it will cost more per month for a borrower to buy ‘their same home.’”

In other words, the longer you wait, the more it will cost you.

Bottom Line

While it’s true today’s average mortgage rate is higher than just a few months ago, 3% mortgage rates shouldn’t deter you from your homebuying goals. Historically, today’s rate is still low. And since rates are expected to continue rising, buying now could save you money in the long run. Let’s connect so you can lock in a great rate now.

Experts Project Mortgage Rates Will Continue To Rise in 2022

Mortgage rates are one of several factors that impact how much you can afford if you’re buying a home. When rates are low, they help you get more house for your money. Within the last year, mortgage rates have hit the lowest point ever recorded, and they’ve hovered in the historic-low territory. But even over the past few weeks, rates have started to rise. This past week, the average 30-year fixed rate was 3.14%.

What does this mean if you’re thinking about making a move? Waiting until next year will cost you more in the long run. Here’s a look at what several experts project for mortgage rates going into 2022.

Freddie Mac:

“The average 30-year fixed-rate mortgage (FRM) is expected to be 3.0 percent in 2021 and 3.5 percent in 2022.”

Doug Duncan, Senior VP & Chief Economist, Fannie Mae:

“Right now, we forecast mortgage rates to average 3.3 percent in 2022, which, though slightly higher than 2020 and 2021, by historical standards remains extremely low and supportive of mortgage demand and affordability.”

First American:

“Consensus forecasts predict that mortgage rates will hit 3.2 percent by the end of the year, and 3.7 percent by the end of 2022.”

If rates rise even a half-point percentage over the next year, it will impact what you pay each month over the life of your loan – and that can really add up. So, the reality is, as prices and mortgage rates rise, it will cost more to purchase a home.

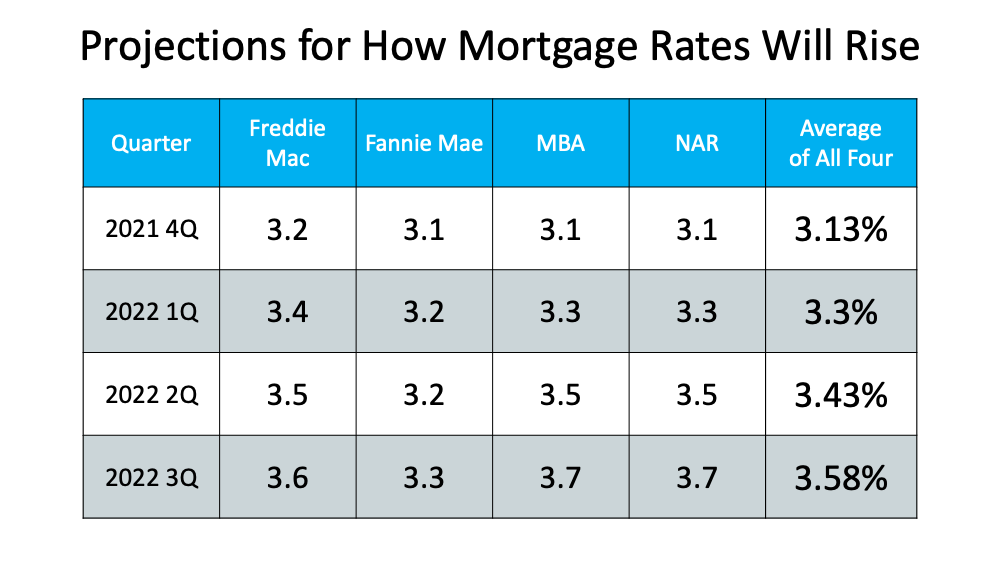

As you can see from the quotes above, industry experts project rates will rise in the months ahead. Here’s a table that compares other expert views and gives an average of those projections: Whether you’re thinking about buying your first home, moving up to your dream home, or downsizing because your needs have changed, purchasing before mortgage rates rise even higher will help you take advantage of today’s homebuying affordability. That could be just the game-changer you need to achieve your homeownership goals.

Whether you’re thinking about buying your first home, moving up to your dream home, or downsizing because your needs have changed, purchasing before mortgage rates rise even higher will help you take advantage of today’s homebuying affordability. That could be just the game-changer you need to achieve your homeownership goals.

Bottom Line

If you’re thinking of buying or selling over the next year, it may be wise to make your move sooner rather than later – before mortgage rates climb higher.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of.

Start Here!

Contact one of Our Agents today!

See out Complete Inventory of Available Properties!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams.

What’s your home’s value?

October 2021 Housing Market Update

The October 2021 Housing Market Update was held on October 19 at 12 p.m. If you missed the live webinar or would like to watch it again, it is available below.

Home Price Appreciation

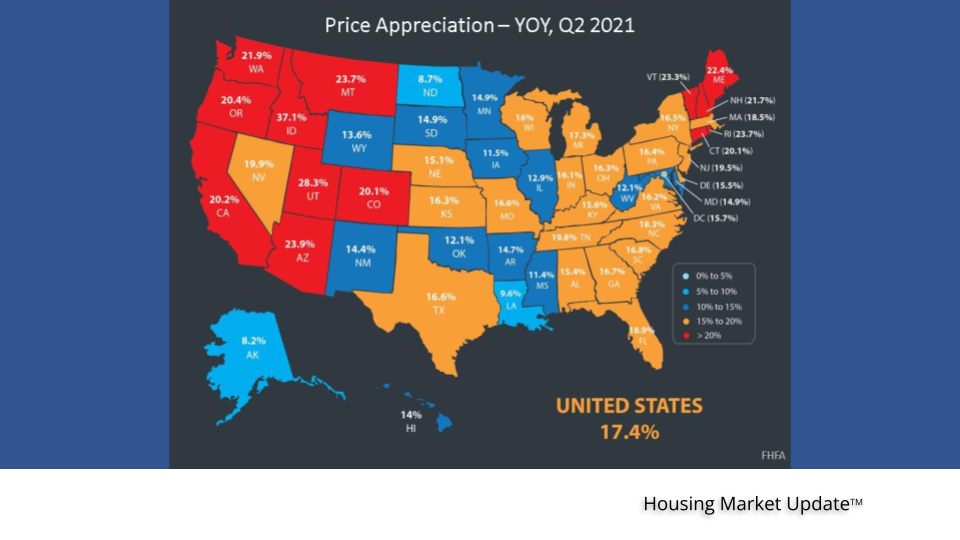

Geoff Green, the host of the event, jumped right into the stats. First, there has been an amazing amount of appreciation taking place in the U.S. housing market. For example, the year-over-year average appreciation as of July 2021 was +19.2%. Of course, the pandemic has greatly impacted the market. In other words, many people decided to leave metropolitan areas and move to suburban and rural areas. Consequently, the lack of inventory, low mortgage rates, and a robust economy created a “feeding frenzy” of potential buyers.

The map below shows price appreciation by states and regions.

However, according to Ivy Zelman of Zelman & Associates,

“Closings are set to decline roughly 10% year over year in the 2nd half of 2021 and home price appreciation is on the cusp of flipping to a decelerating trend.”

Geoff stressed that decelerating means a slower amount of appreciation, and not a depreciation of value.

Mortgage rates and the impact on purchasing power

From January of 2020, rates plummeted down and bottomed out at beginning of 2021. They have been rising since. Mortgage rates have now jumped above 3%. Historically, these rates are still very low.

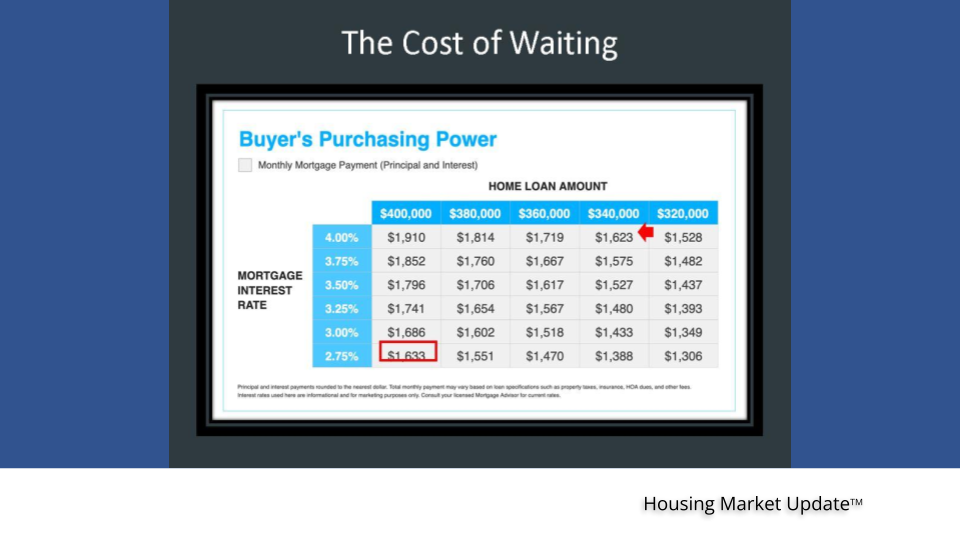

However, the chart below demonstrates how rising rates can impact your buying power.

More factors discussed

Geoff presented data on factors impacting the economy and the housing market. For instance, the rate of inflation, the high price of food, supply chain issues, oil prices, and more may impact the decision to buy or sell a home.

National Housing Market Stats

Existing home sales are starting to come down after last year’s numbers, but they are coming down softly. Average home sale price is appreciating at a lower rate. The months’ supply of inventory is actually starting to come up, but nowhere near the levels it has been or needs to be to meet demand.

Meet our Panel

Panelists for the October 2021 Housing Market Update are Tiffany Megna, Green Team New York Realty, Keren Gonen, Green Team New Jersey Realty, and Jessica Imparato, Cardinal Financial.

They discussed what they are seeing from their perspective, with “boots on the ground,” Despite stats showing the market softening, they have not seen a decline in their businesses. Jessica discussed how prospective buyers can be impacted by an increase in mortgage rates.

To see the entire presentation and panel discussion, click here To sign up for Housing Market Updates, click here.

“Housekeeping” Details

Don’t Wait for a Lower Mortgage Rate – It Could Cost You

Today’s housing market is truly one for the record books. Over the past year, we’ve seen the lowest mortgage rates in history. And while those rates seemed to bottom out in January of this year, the golden window of opportunity for buyers isn’t over just yet. If you’re one of the buyers who worry they’ve missed out, rest assured today’s mortgage rates are still worth taking advantage of.

Even today, our mortgage rates are below what they’ve been in recent decades. So, while you may not be able to lock in the rate your friend got recently, you’re still in a great position to secure a rate well below what your parents and even grandparents got in years past. The key will be acting sooner rather than later.

In late September, mortgage rates ticked above 3% for the first time in months. And according to experts throughout the industry, mortgage rates are projected to continue rising in the months ahead. Here’s where experts say rates are headed: While a projected half percentage point increase may not seem substantial, it does have an impact when you’re buying a home. When rates rise even slightly, it affects how much you’ll pay month-to-month on your home loan. The chart below shows how it works:

While a projected half percentage point increase may not seem substantial, it does have an impact when you’re buying a home. When rates rise even slightly, it affects how much you’ll pay month-to-month on your home loan. The chart below shows how it works: In this example, if rates rise to 3.55%, you’ll pay an extra $100 each month on your monthly mortgage payment if you purchase a home around this time next year. That extra money can really add up over the life of a 15 or 30-year loan.

In this example, if rates rise to 3.55%, you’ll pay an extra $100 each month on your monthly mortgage payment if you purchase a home around this time next year. That extra money can really add up over the life of a 15 or 30-year loan.

Clearly, today’s mortgage rates are worth taking advantage of before they climb further. The rates we’re seeing right now give you a unique opportunity to afford more home for your money while keeping your monthly payment down.

Bottom Line

Waiting for a lower mortgage rate could cost you. Experts project rates will continue to rise in the months ahead. Let’s connect so you can seize this opportunity before they increase further.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of.

Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams.

What’s your home’s value?

Contact one of Our Agents today!

The Main Key To Understanding the Rise in Mortgage Rates

Every Thursday, Freddie Mac releases the results of their Primary Mortgage Market Survey which reveals the most recent movement in the 30-year fixed mortgage rate. Last week, the rate was announced as 3.01%. It was the first time in three months that the mortgage rate surpassed 3%. In a press release accompanying the survey, Sam Khater, Chief Economist at Freddie Mac, explains:

“Mortgage rates rose across all loan types this week as the 10-year U.S. Treasury yield reached its highest point since June.”

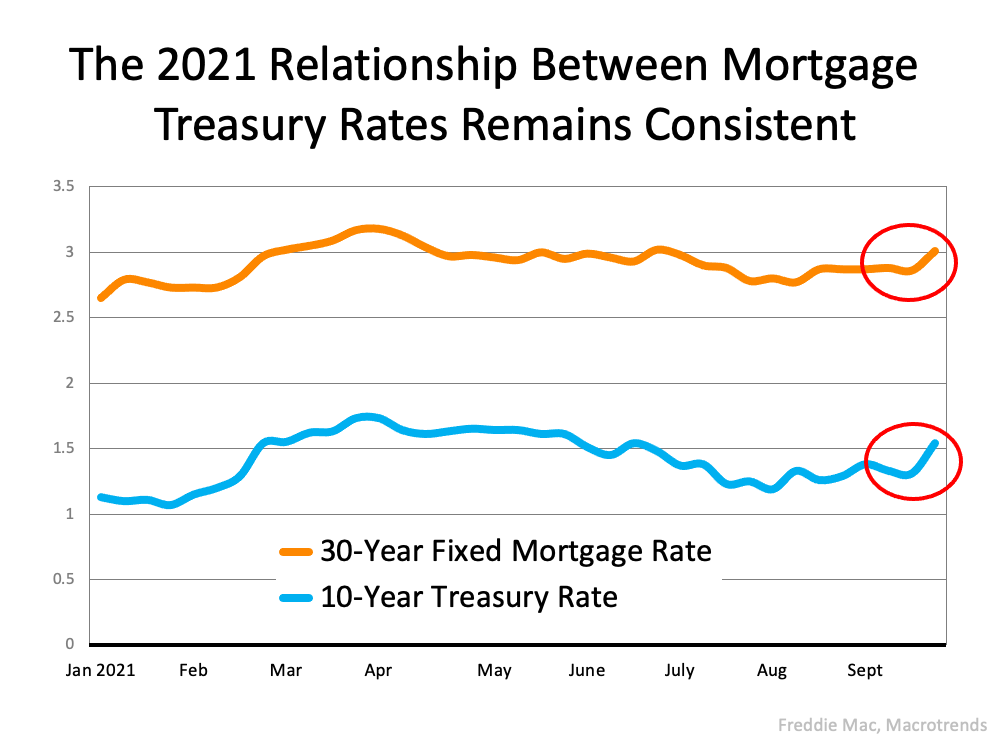

The reason Khater mentions the 10-year U.S. Treasury yield is because there has been a very strong relationship between the yield and the 30-year mortgage rate over the last five decades. Here’s a graph showing that relationship: The relationship has also been consistent throughout 2021 as evidenced by this graph:

The relationship has also been consistent throughout 2021 as evidenced by this graph: The graph also reveals the most recent jump in mortgage rates was preceded by a jump in the 10-year Treasury rate (called out by the red circles).

The graph also reveals the most recent jump in mortgage rates was preceded by a jump in the 10-year Treasury rate (called out by the red circles).

So, What Impacts the Yield Rate?

According to Investopedia:

“There are a number of economic factors that impact Treasury yields, such as interest rates, inflation, and economic growth.”

Since there are currently concerns about inflation and economic growth due to the pandemic, the Treasury yield spiked last week. That spike impacted mortgage rates.

What Does This Mean for You?

Khater, in the Freddie Mac release mentioned above, says:

“We expect mortgage rates to continue to rise modestly which will likely have an impact on home prices, causing them to moderate slightly after increasing over the last year.”

Nadia Evangelou, Senior Economist and Director of Forecasting for the National Association of Realtors (NAR), also addresses the issue:

“Consumers shouldn’t panic. Keep in mind that even though rates will increase in the following months, these rates will still be historically low. The National Association of REALTORS forecasts the 30-year fixed mortgage rate to reach 3.5% by mid-2022.”

Bottom Line

Forecasting mortgage rates is very difficult. As Mark Fleming, Chief Economist at First American, once quipped:

“You know, the fallacy of economic forecasting is don’t ever try and forecast interest rates and or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

That being said, if you’re either a first-time homebuyer or a current homeowner thinking of moving into a home that better fits your current needs, keep abreast of what’s happening with mortgage rates. It may very well impact your decision.

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams.

What’s your home’s value?

Contact one of Our Agents today!

See out Complete Inventory of Available Properties!