Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Congratulations to the Kimiecik Team!

Congratulations to Chis and Megan Kimiecik for reaching not 1 but 2 new personal bests!

Teamwork makes the dream work and Chris and Megan are reaching impressive new milestones in 2022. In March alone this amazing team brought in a whopping $1,877,500 in sales volume. This brings their first-quarter sales volume to $2,474,500! Not only was this their best quarter yet but they have already surpassed their 2021 sales volume in only the first quarter of 2022!

Now that’s something to celebrate!

Congratulations to the Kimiecik Team!

Congratulations to Chis and Megan Kimiecik for reaching not 1 but 2 new personal bests!

Teamwork makes the dream work and Chris and Megan are reaching impressive new milestones in 2022. In March alone this amazing team brought in a whopping $1,877,500 in sales volume. This brings their first-quarter sales volume to $2,474,500! Not only was this their best quarter yet but they have already surpassed their 2021 sales volume in only the first quarter of 2022!

Now that’s something to celebrate!

The Dream of Homeownership Is Worth the Effort

If you’re in the market to buy a home this season, stick with it. Homebuyers face challenges in any market, and today’s is no exception. But if you persevere, your decision to purchase a home will be worth the effort in the end. In fact, a recent survey from Bankrate shows homeownership is so powerful that:

“Nearly three in four homeowners say they would still buy their current home if they had it to do [sic] all over again.”

That means the results – owning a home and the benefits that come with it – outweigh the effort needed to achieve their goal. If you’re a homebuyer, let that provide you with the confidence to know the work you’re putting in today will pay off for years to come. Here are a few reasons to stick with your search and focus on the outcome.

Homeownership Contributes Significantly to Your Financial Well-Being

The National Association of Realtors (NAR) lists several motivations to consider if you’re thinking about buying a home. One of the top financial reasons is the equity you build. As NAR says:

“Money paid for rent is money that you’ll never see again, but mortgage payments let you build equity . . . Building equity in your home is a ready-made savings plan.”

Your equity is a powerful tool you can leverage in a number of ways. And with recent home price appreciation, homeowners are seeing record levels of equity today. That may be one reason why so many people view owning a home as a great investment and a top indicator of financial well-being. As the survey from Bankrate mentioned above shows:

“. . . Americans place a higher value on homeownership than on any other indicator of economic stability, . . .”

Owning a home ranks above other major accomplishments like retirement, having a successful career, and getting a college degree. That indicates just how impactful the financial benefits of homeownership truly are.

The Emotional Benefits of Owning a Home Are Powerful

Of course, homeownership is more than an investment. In their list of top reasons to buy a home, NAR also highlights some of the powerful, non-financial aspects of homeownership. Among them is the opportunity to customize your home to reflect your personality and needs. As they say:

“The home is yours. You can decorate any way you want and choose the types of upgrades and new amenities that appeal to your lifestyle.”

Another benefit homeowners enjoy is the stability it provides. Homeowners typically stay put longer than renters. According to NAR, when you remain in one place longer than a few years, you can grow closer to your community. And that can enhance your sense of pride and lead to better relationships.

What Does That Mean for You?

The benefits of homeownership are powerful, as Leslie Rouda Smith, President of NAR, says:

“From building personal wealth and fostering communities, to strengthening social stability and driving the national economy, the value of homeownership is indisputable.”

Even if you face challenges in today’s market, the payoff when you succeed and purchase a home will be worth it.

Bottom Line

If you’re planning to buy a home this year, there are incredible benefits waiting for you at the end of your journey. Let’s connect to discuss everything homeownership has to offer.

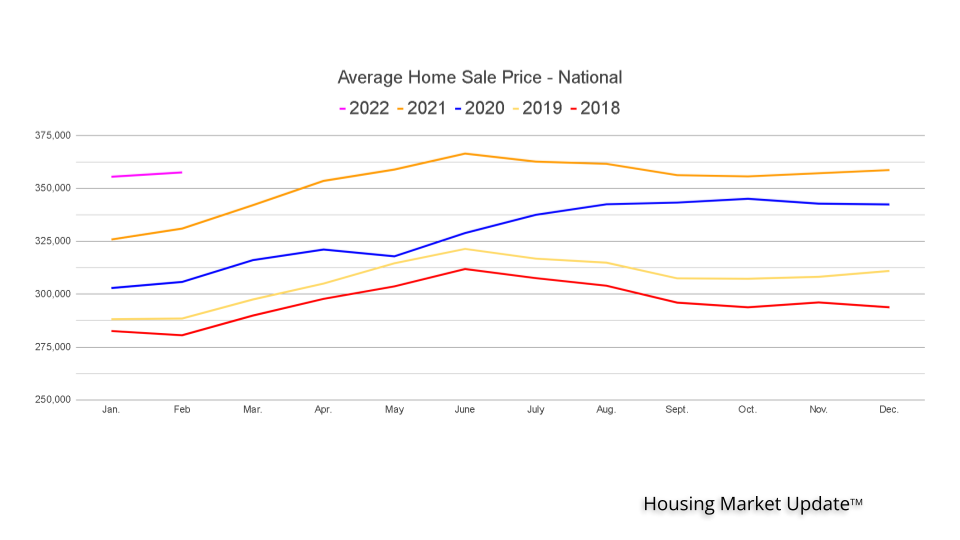

April 2022 Housing Market Update

Geoff Green is President of Green Team Realty and Co-founder and CEO of NuOp. In addition, he is the moderator of the monthly Housing Market Updates. With so many changes in the market, Geoff began the April 2022 Housing Market Update with information on rising mortgage rates.

If you haven’t yet seen the April 2022 Housing Market Update or would like to watch it again, it’s available below.

Geoff provided some historical perspectives on rising rates and their impact. With statistics going back to 1993, it appears that prices will continue to climb even as rates are climbing.

Spring Market

Buyer traffic is very strong. Inventory continues to be very low. However, there has been a slight bump in active listings for the first time in 6 months. According to Lance Lambert, Editorial Director, Fortune,

“…some experts say that 2022 spring housing market might go down as one of the most competitive on record.”

Home Sale Price

The year-over-year stats show that sales prices are not going backward.

Meet our Panel

Vikki Garby, of Green Team New York Realty and Michael Giannetto of CrossCountry Mortgage, joined Geoff for their take on the market. To watch the panel discussion, click here.

Thanks to our Sponsor

NuOp is the Business Opportunity Exchange. View a live feed of Real Estate and Mortgage Referrals on NuOp.com

Sign up for Housing Market Updates

Join us for our next Housing Market Update on May 15, 2022. To stay informed and sign up for our housing market updates, click here.

How Homeownership Can Help Shield You from Inflation

If you’re following along with the news today, you’ve likely heard about rising inflation. You’re also likely feeling the impact in your day-to-day life as prices go up for gas, groceries, and more. These rising consumer costs can put a pinch on your wallet and make you re-evaluate any big purchases you have planned to ensure they’re still worthwhile.

If you’ve been thinking about purchasing a home this year, you’re probably wondering if you should continue down that path or if it makes more sense to wait. While the answer depends on your situation, here’s how homeownership can help you combat the rising costs that come with inflation.

Homeownership Offers Stability and Security

Investopedia explains that during a period of high inflation, prices rise across the board. That’s true for things like food, entertainment, and other goods and services, even housing. Both rental prices and home prices are on the rise. So, as a buyer, how can you protect yourself from increasing costs? The answer lies in homeownership.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. If you get a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

So even if other prices rise, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

Use Home Price Appreciation to Your Benefit

While it’s true rising mortgage rates and home prices mean buying a house today costs more than it did a year ago, you still have an opportunity to set yourself up for a long-term win. Buying now lets you lock in at today’s rates and prices before both climb higher.

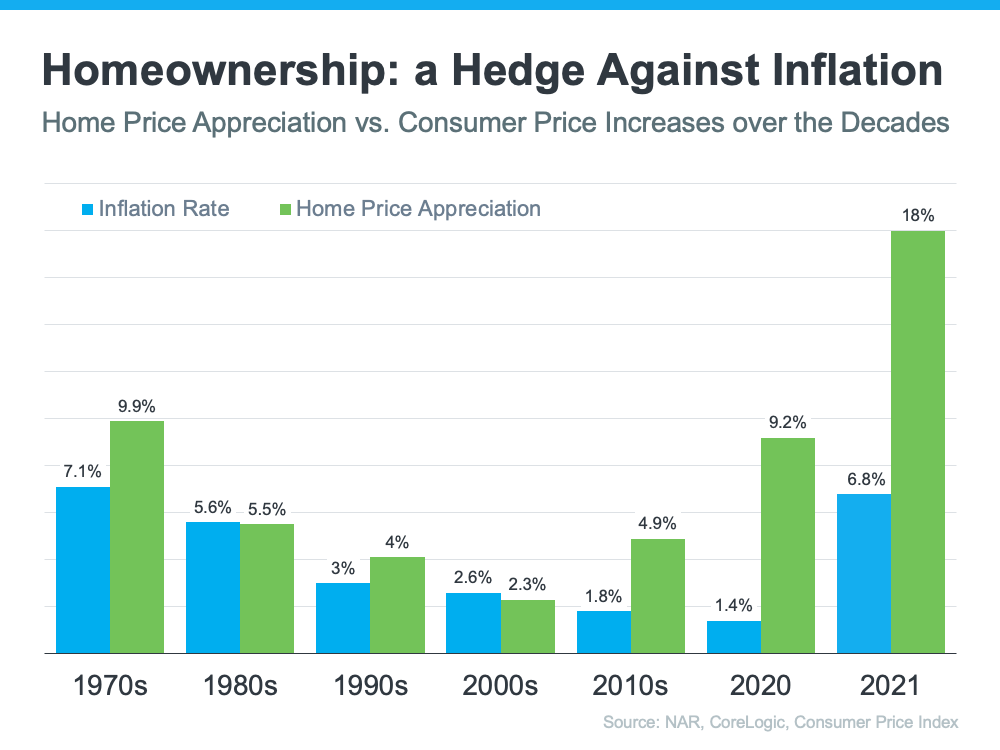

In inflationary times, it’s especially important to invest your money in an asset that traditionally holds or grows in value. The graph below shows how home price appreciation outperformed inflation in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

So, what does that mean for you? Today, experts say home prices will only go up from here thanks to the ongoing imbalance in supply and demand. Once you buy a house, any home price appreciation that does occur will be good for your equity and your net worth. And since homes are typically assets that grow in value (even in inflationary times), you have peace of mind that history shows your investment is a strong one.

Bottom Line

If you’re ready to buy a home, it may make sense to move forward with your plans despite rising inflation. If you want expert advice on your specific situation and how to time your purchase, let’s connect.

Is It Enough To Offer Asking Price in Today’s Housing Market?

If you’re planning to buy a home this season, you’re probably thinking about what you’ll need to do to get your offer accepted. In previous years, it was common for buyers to try and determine how much less than the asking price they could offer to still get the home. The buyer and seller would then negotiate and typically agree on a revised price that was somewhere between the buyer’s bid and the home’s initial asking price.

In today’s real estate market, buyers shouldn’t shop for a home with the same expectations.

Things Are Different Today

Today’s housing market is anything but normal. According to the National Association of Realtors (NAR), the average home that’s sold today:

- Receives 4.8 offers

- Sells in just 17 days

Homes selling quickly and receiving multiple offers shows how competitive the housing market is for buyers right now. This is because there are more buyers on the market than homes for sale. When the number of homes available can’t keep up with demand, homes often sell for more than the asking price.

How Does This Impact You When It’s Time To Submit an Offer?

Market conditions should help guide your decisions throughout the process. Today, the asking price of a home is often the floor of the negotiation rather than the ceiling. Knowing this is important when it’s time to submit an offer, but you should also use that information as you’re searching for homes too. After all, you don’t want to fall in love with a home that ultimately sells for a price higher than what you’ve budgeted for.

The Mortgage Reports has advice if you’re looking to purchase a home in a competitive market. The article encourages you to be realistic with your housing search, saying:

“The best thing to do is set your budget and expectations ahead of time so you know how much you can afford to offer — and when to walk away. This will make negotiations a lot easier.”

Of course, when you’ve found your dream home, you’ll want to do everything you can to submit your best offer up front and win a potential bidding war. Knowing the current market is key to crafting a winning offer. That’s where working with an expert real estate advisor becomes critical.

A real estate professional will draw from their experience and expert-level knowledge of today’s housing market throughout the process. They’ll also balance conditions in your area to make sure your offer stands out above the rest.

Bottom Line

Understanding how to approach the asking price of a home and what’s happening in today’s real estate market are critical for buyers. Let’s connect so we can work together to create a winning plan for you.

Why This Housing Market Is Not a Bubble Ready To Pop

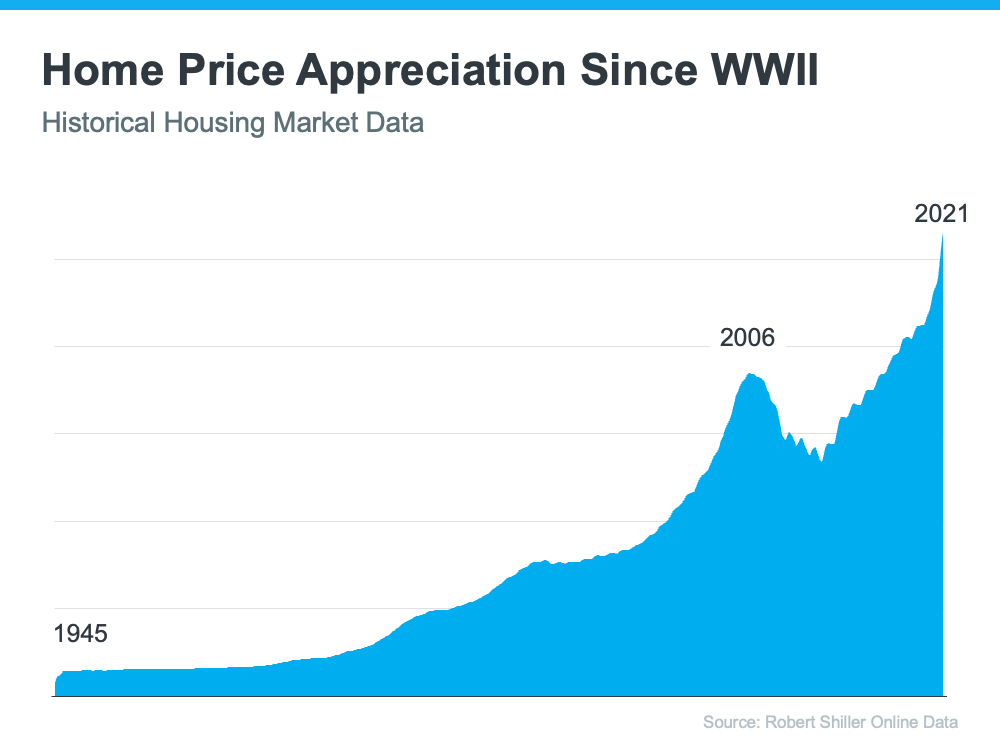

Homeownership has become a major element in achieving the American Dream. A recent report from the National Association of Realtors (NAR) finds that over 86% of buyers agree homeownership is still the American Dream.

Prior to the 1950s, less than half of the country owned their own home. However, after World War II, many returning veterans used the benefits afforded by the GI Bill to purchase a home. Since then, the percentage of homeowners throughout the country has increased to the current rate of 65.5%. That strong desire for homeownership has kept home values appreciating ever since. The graph below tracks home price appreciation since the end of World War II:

The graph shows the only time home values dropped significantly was during the housing boom and bust of 2006-2008. If you look at how prices spiked prior to 2006, it looks a bit like the current spike in prices over the past two years. That may lead some people to be concerned we’re about to see a similar fall in home values as we did when the bubble burst. To help alleviate those worries, let’s look at what happened last time and what’s happening today.

What Caused the Housing Crash 15 Years Ago?

Back in 2006, foreclosures flooded the market. That drove down home values dramatically. The two main reasons for the flood of foreclosures were:

- Many purchasers were not truly qualified for the mortgage they obtained, which led to more homes turning into foreclosures.

- A number of homeowners cashed in the equity on their homes. When prices dropped, they found themselves in an underwater situation (where the home was worth less than the mortgage on the house). Many of these homeowners walked away from their homes, leading to more foreclosures. This lowered neighboring home values even more.

This cycle continued for years.

Why Today’s Real Estate Market Is Different

Here are two reasons today’s market is nothing like the one we experienced 15 years ago.

1. Today, Demand for Homeownership Is Real (Not Artificially Generated)

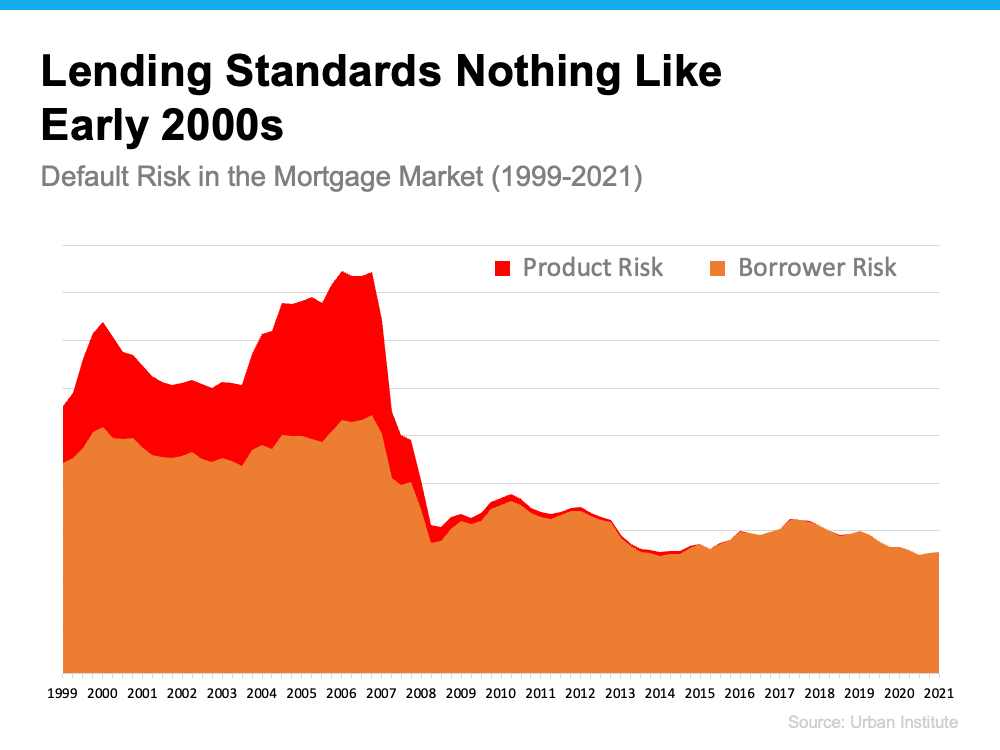

Running up to 2006, banks were creating artificial demand by lowering lending standards and making it easy for just about anyone to qualify for a home loan or refinance their current home. Today, purchasers and those refinancing a home face much higher standards from mortgage companies.

Data from the Urban Institute shows the amount of risk banks were willing to take on then as compared to now.

There’s always risk when a bank loans money. However, leading up to the housing crash 15 years ago, lending institutions took on much greater risks in both the person and the mortgage product offered. That led to mass defaults, foreclosures, and falling prices.

Today, the demand for homeownership is real. It’s generated by a re-evaluation of the importance of home due to a worldwide pandemic. Additionally, lending standards are much stricter in the current lending environment. Purchasers can afford the mortgage they’re taking on, so there’s little concern about possible defaults.

And if you’re worried about the number of people still in forbearance, you should know there’s no risk of that causing an upheaval in the housing market today. There won’t be a flood of foreclosures.

2. People Are Not Using Their Homes as ATMs Like They Did in the Early 2000s

As mentioned above, when prices were rapidly escalating in the early 2000s, many thought it would never end. They started to borrow against the equity in their homes to finance new cars, boats, and vacations. When prices started to fall, many of these homeowners were underwater, leading some to abandon their homes. This increased the number of foreclosures.

Homeowners didn’t forget the lessons of the crash as prices skyrocketed over the last few years. Black Knight reports that tappable equity (the amount of equity available for homeowners to access before hitting a maximum 80% loan-to-value ratio, or LTV) has more than doubled compared to 2006 ($4.6 trillion to $9.9 trillion).

The latest Homeowner Equity Insights report from CoreLogic reveals that the average homeowner gained $55,300 in home equity over the past year alone. Odeta Kushi, Deputy Chief Economist at First American, reports:

“Homeowners in Q4 2021 had an average of $307,000 in equity – a historic high.”

ATTOM Data Services also reveals that 41.9% of all mortgaged homes have at least 50% equity. These homeowners will not face an underwater situation even if prices dip slightly. Today, homeowners are much more cautious.

Bottom Line

The major reason for the housing crash 15 years ago was a tsunami of foreclosures. With much stricter mortgage standards and a historic level of homeowner equity, the fear of massive foreclosures impacting today’s market is not realistic.

Myths About Today’s Housing Market [INFOGRAPHIC]

![Myths About Today’s Housing Market [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/04/21104919/20220422-MEM-1046x1690.png)

Some Highlights

- If you’re planning to buy or sell a home today, it’s important to be aware of common misconceptions.

- Whether it’s timing your purchase as a buyer based on home prices and mortgage rates or knowing what to upgrade or repair before listing your house as a seller, it takes a professional to guide you through those decisions.

- Let’s connect so you have an expert to help separate fact from fiction in today’s housing market.

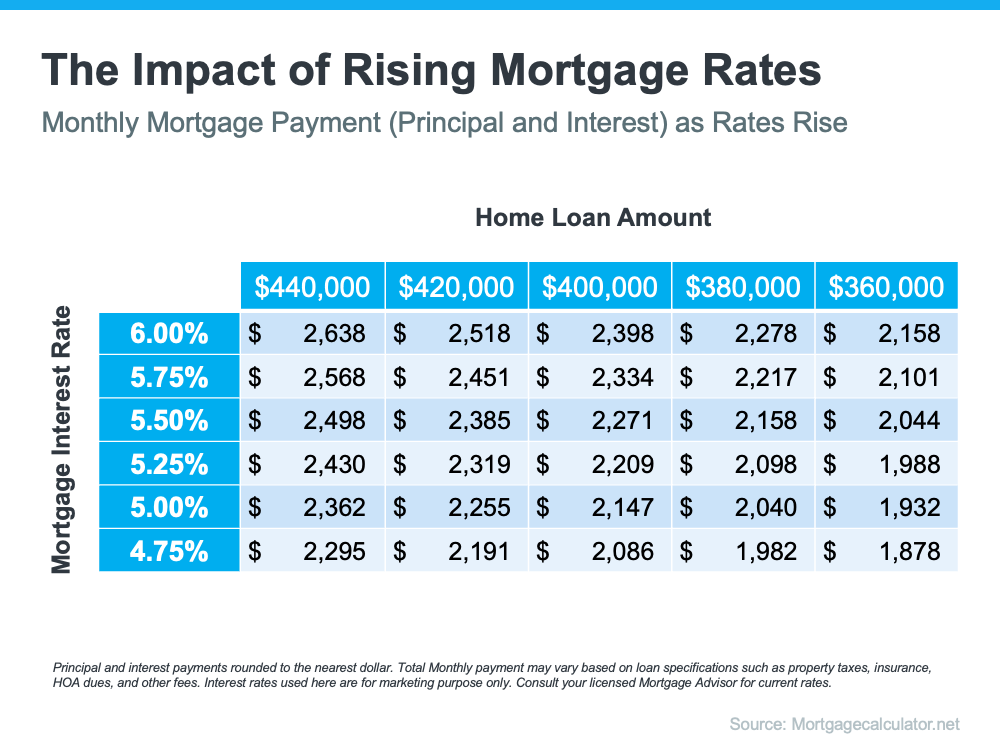

How To Approach Rising Mortgage Rates as a Buyer

In the last few weeks, the average 30-year fixed mortgage rate from Freddie Mac inched up to 5%. While that news may have you questioning the timing of your home search, the truth is, timing has never been more important. Even though you may be tempted to put your plans on hold in hopes that rates will fall, waiting will only cost you more. Mortgage rates are forecast to continue rising in the year ahead.

If you’re thinking of buying a home, here are a few things to keep in mind so you can succeed even as mortgage rates rise.

How Rising Mortgage Rates Impact You

Mortgage rates play a significant role in your home search. As rates go up, they impact how much you’ll pay in your monthly mortgage payment, which directly affects how much you can comfortably afford. Here’s an example of how even a quarter-point increase can have a big impact on your monthly payment (see chart below):

With mortgage rates on the rise, you’ve likely seen your purchasing power impacted already. Instead of delaying your plans, today’s rates should motivate you to purchase now before rates increase more. Use that motivation to energize your search and plan your next steps accordingly.

The best way to prepare is to work with a trusted real estate advisor now. An agent can connect you with a trusted lender, help you adjust your search based on your budget, and make sure you’re ready to act quickly when it’s time to make an offer.

Bottom Line

Serious buyers should approach rising rates as a motivating factor to buy sooner, not a reason to wait. Waiting will cost you more in the long run. Let’s connect today so you can better understand your budget and be prepared to buy your home even before rates climb higher.