Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

With each quarter of a percent increase in interest rate, the value of the home you can afford decreases by 2.5% (in this example, $10,000). Experts predict that mortgage rates will be closer to 5% by this time next year.

Buying a home • Mortgage and Home Loans •

February 28, 2021

The Reason Mortgage Rates Are Projected to Increase and What It Means for You

We’re currently experiencing historically low mortgage rates. Over the last fifty years, the average on a Freddie Mac 30-year fixed-rate mortgage has been 7.76%. Today, that rate is 2.81%. Flocks of homebuyers have been taking advantage of these remarkably low rates over the last twelve months. However, there’s no guarantee rates will remain this low much longer.

Whenever we try to forecast mortgage rates, we should consider the advice of Mark Fleming, Chief Economist at First American:

“You know, the fallacy of economic forecasting is don’t ever try and forecast interest rates and/or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

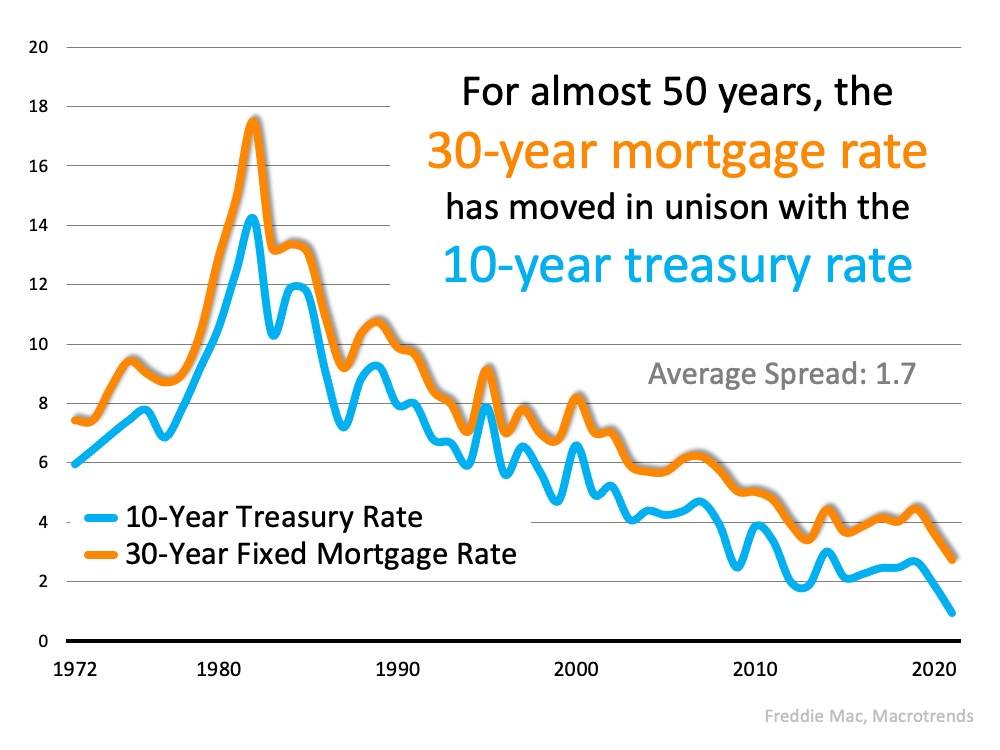

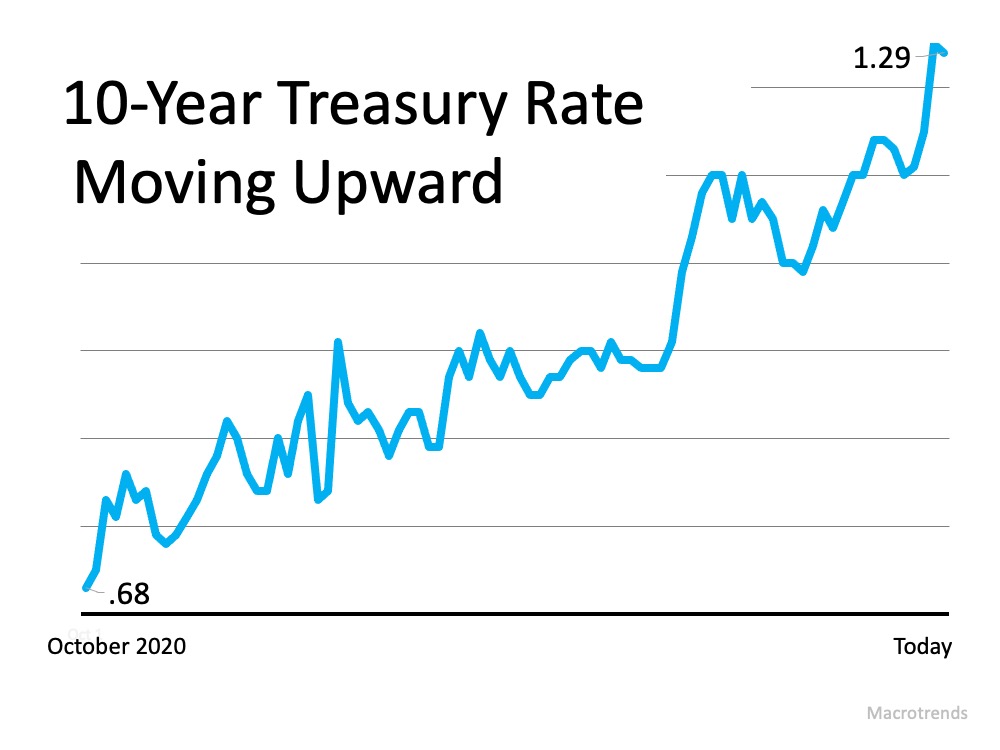

Many things impact mortgage rates. The economy, inflation, and Fed policy, just to name a few. That makes forecasting rates difficult. However, there’s one metric that has held up over the last fifty years – the relationship between mortgage rates and the 10-year treasury rate. Here’s a graph detailing this relationship since Freddie Mac started keeping mortgage rate records in 1972: There’s no denying the close relationship between the two. Over the last five decades, there’s been an average 1.7-point spread between these two rates. It’s this long-term relationship that has some forecasters projecting an increase in mortgage rates as we move throughout the year. This is based on the recent surge in the 10-year treasury rate shown here:

There’s no denying the close relationship between the two. Over the last five decades, there’s been an average 1.7-point spread between these two rates. It’s this long-term relationship that has some forecasters projecting an increase in mortgage rates as we move throughout the year. This is based on the recent surge in the 10-year treasury rate shown here: The spread between the two is now 1.53, indicating mortgage rates could rise. Actually, a bump-up in rate has already begun. As Joel Kan, Associate VP of Economic Forecasting for the Mortgage Bankers Association, reveals:

The spread between the two is now 1.53, indicating mortgage rates could rise. Actually, a bump-up in rate has already begun. As Joel Kan, Associate VP of Economic Forecasting for the Mortgage Bankers Association, reveals:

“Expectations of faster economic growth and inflation continue to push Treasury yields & mortgage rates higher. Since hitting a survey low in December, the 30-year fixed rate has slowly risen, & last week climbed to its highest level since Nov 2020.”

How high might they go in 2021?

No one knows for sure. Sam Khater, Chief Economist for Freddie Mac, recently suggested:

“While there are multiple temporary factors driving up rates, the underlying economic fundamentals point to rates remaining in the low 3% range for the year.”

What does this mean for you?

Whether you’re a first-time buyer or you’ve purchased a home before, even an increase of half a point in mortgage rate (2.81 to 3.31%) makes a big difference. On a $300,000 mortgage, that difference (including principal and interest) is $82 a month, $984 a year, or a total of $29,520 over the life of the home loan.

Bottom Line

Based on the 50-year symbiotic relationship between treasury rates and mortgage rates, it appears mortgage rates could be headed up this year. It may make sense to buy now rather than wait.

Contact one of Our Agents today!

Buying a home •

February 25, 2021

The Luxury Market Is Attracting Buyers in 2021

[et_pb_section fb_built=”1″ _builder_version=”3.0.47″ custom_padding=”16px|0px|0px|0px|false|false”][et_pb_row custom_padding=”22px|0px|32px|0px|false|false” _builder_version=”3.0.48″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.0.74″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]As more people continue to identify their changing needs this year, some are turning to the upscale housing sector for more space or finer features. In their most recent Luxury Market Report, the Institute for Luxury Home Marketing (ILHM) shares:

“In a snapshot of 2020, despite the devasting effects of the coronavirus pandemic, the luxury real estate market has seen one of its strongest years since 2008. In comparison to experts’ predictions in early 2020, it is remarkable how significant demands for property type, location, and amenity preferences have changed amid the pandemic.”

With more opportunities to work from home and a growing interest in having extra space for things like virtual school, working out, and cooking more meals, the desire to own a home that can meet these needs continues to increase. Additionally, record-low mortgage rates are creating opportunities for homebuyers to stretch their legs into higher price points or even expand their real estate portfolios. The ILHM report continues to say:

“Experts believe that the demand for exclusive residential properties outside the metropolitan areas will continue well into 2021; even with the introduction of vaccines, the pandemic is far from over.

For those who have moved to the suburbs and beyond, moving back to the city full time is unlikely while the work from home trend remains. Many of these affluent homeowners are now making their secondary properties their primary residences for the foreseeable future.”

If you’re interested in buying a home this year, it appears that some higher-priced markets may have more homes to choose from than those at lower price points. Javier Vivas, Director of Economic Research at realtor.com, notes:

“Interestingly, markets, where new supply is improving the fastest, tend to be higher priced than those that have yet to see improvement, suggesting sellers are more active in the more expensive markets.”

Bottom Line

If you’re hoping to buy the home of your dreams, this could be the year to achieve that goal. Let’s connect today to explore your possibilities.

Contact one of Our Agents today!

See our Complete Inventory of Available Properties!

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section fb_built=”1″ _builder_version=”3.18.2″][et_pb_row _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_blog fullwidth=”off” posts_number=”3″ include_categories=”43″ show_author=”off” show_date=”off” show_categories=”off” _builder_version=”3.18.2″ header_level=”h5″ header_font=”||||||||” body_font=”||||||||” border_radii=”on|12px|12px|12px|12px” text_orientation=”center”][/et_pb_blog][/et_pb_column][/et_pb_row][/et_pb_section]

Housing Market News •

May 7, 2020

Buying a Home Right Now: Easy? No. Smart? Yes.

[et_pb_section fb_built=”1″ _builder_version=”3.0.47″][et_pb_row _builder_version=”3.0.48″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.0.74″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]Through all the volatility in the economy right now, some have put their search for a home on hold, yet others have not. According to ShowingTime, the real estate industry’s leading showing management technology provider, buyers have started to reappear over the last several weeks. In the latest report, they revealed:

“The March ShowingTime Showing Index® recorded the first nationwide drop in showing traffic in eight months as communities responded to COVID-19. Early April data show signs of an upswing, however.”

Why would people be setting appointments to look at prospective homes when the process of purchasing a home has become more difficult with shelter-in-place orders throughout the country? Here are three reasons for this uptick in activity: 1. Some people need to move. Whether because of a death in the family, a new birth, divorce, financial hardship, or a job transfer, some families need to make a move as quickly as possible. 2. Real estate agents across the country have become very innovative, utilizing technology that allows purchasers to virtually:

- View homes

- Meet with mortgage professionals

- Consult with their agent throughout the process

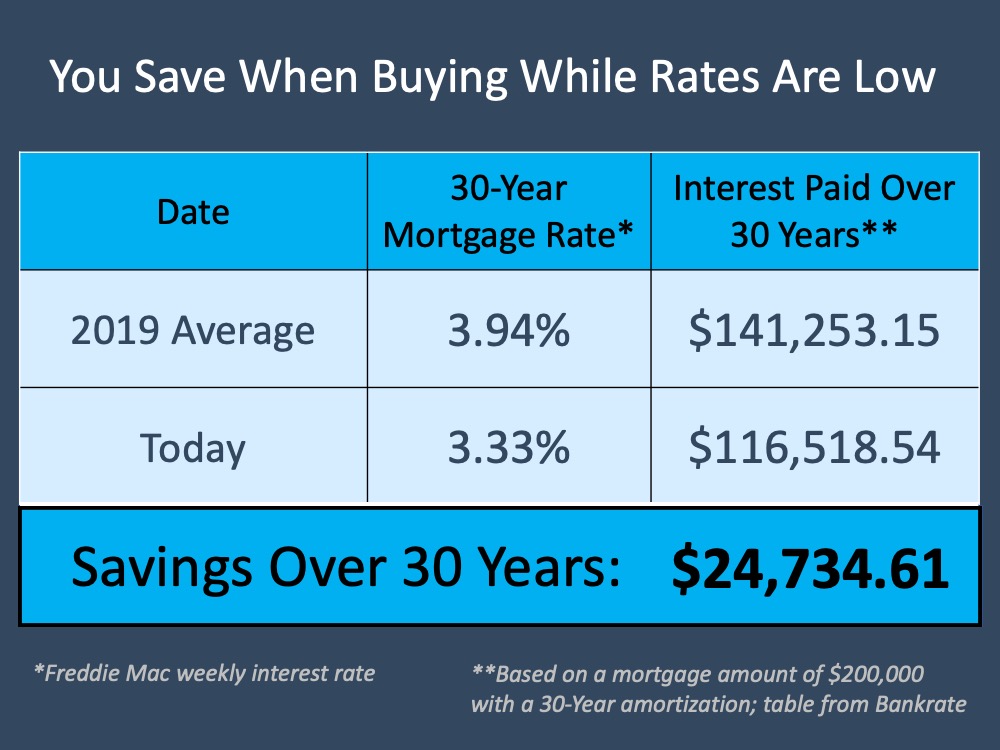

All of this can happen within the required safety protocols, so real estate professionals are continuing to help families make important moves. 3. Buyers understand that mortgage rates are a key component when determining their monthly mortgage payments. Mortgage interest rates are very close to all-time lows and afford today’s purchaser the opportunity to save tens of thousands of dollars over the lifetime of the loan. Looking closely at the third reason, we can see that there’s a big difference between purchasing a house last year and purchasing one now (see chart below):

Bottom Line

Many families have decided not to postpone their plans to purchase a home, even in these difficult times. If you need to make a move, let’s connect today so you have a trusted advisor to safely and professionally guide you through the process.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section fb_built=”1″ _builder_version=”3.18.2″][et_pb_row _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_post_nav in_same_term=”on” _builder_version=”3.18.2″ title_font=”|800|||||||” title_text_color=”#ffffff” title_font_size=”15px” background_color=”#007a42″ border_radii=”on|2px|2px|2px|2px” border_width_all=”2px” border_color_all=”#007a42″ custom_padding=”1px|4px|1px|4px”][/et_pb_post_nav][/et_pb_column][/et_pb_row][/et_pb_section]

Housing Market News •

July 9, 2018

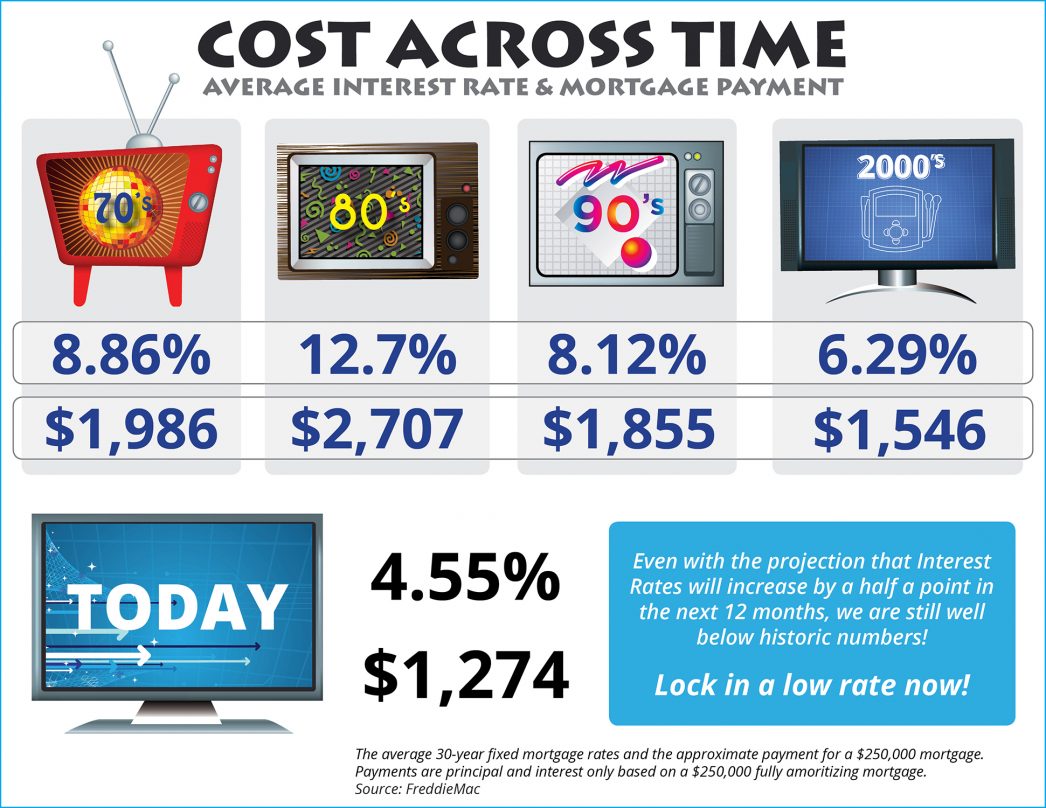

Cost Across Time [INFOGRAPHIC]

Some Highlights:

- With interest rates still around 4.5%, now is a great time to look back at where rates have been over the last 40 years.

- Rates are projected to climb to 5.1% by this time next year according to Freddie Mac.

- The impact your interest rate makes on your monthly mortgage cost is significant!

- Lock in a low rate now while you can!

Want to learn more?

Register for our July Housing Market Update with the CEO of Annie Mac Home Mortgage

It’s Free – Click Here

Housing Market News •

May 22, 2018

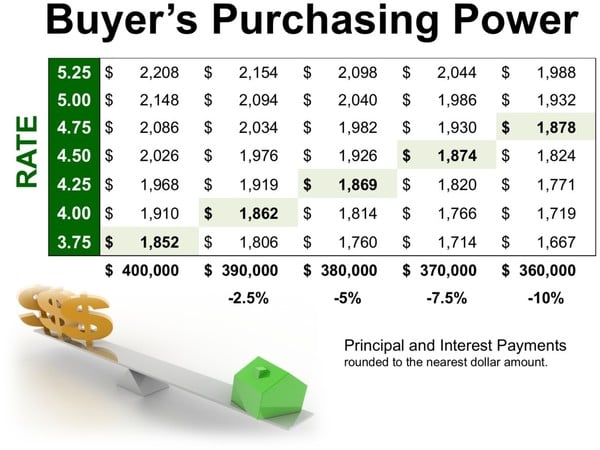

How Current Interest Rates Can Have a High Impact on Your Purchasing Power

According to Freddie Mac’s latest Primary Mortgage Market Survey, interest rates for a 30-year fixed rate mortgage are currently at 4.61%, which is still near record lows in comparison to recent history!

The interest rate you secure when buying a home not only greatly impacts your monthly housing costs, but also impacts your purchasing power.

Purchasing power, simply put, is the amount of home you can afford to buy for the budget you have available to spend. As rates increase, the price of the house you can afford to buy will decrease if you plan to stay within a certain monthly housing budget.

The chart below shows the impact that rising interest rates would have if you planned to purchase a home within the national median price range while keeping your principal and interest payments between $1,850-$1,900 a month.

Housing Market News • Mortgage and Home Loans •

February 5, 2018

Whether You Rent or Buy, Either Way You’re Paying a Mortgage!

There are some people who have not purchased homes because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize, however, that unless you are living with your parents rent-free, you are paying a mortgage – either yours or your landlord’s.

As Entrepreneur Magazine, a premier source for small business explained in their article, “12 Practical Steps to Getting Rich”:

“While renting on a temporary basis isn’t terrible, you should most certainly own the roof over your head if you’re serious about your finances. It won’t make you rich overnight, but by renting, you’re paying someone else’s mortgage. In effect, you’re making someone else rich.”

Christina Boyle, Senior Vice President and head of the Single-Family Sales & Relationship Management organization at Freddie Mac, explains another benefit of securing a mortgage as opposed to paying rent:

“With a 30-year fixed rate mortgage, you’ll have the certainty & stability of knowing what your mortgage payment will be for the next 30 years – unlike rents which will continue to rise over the next three decades.”

As an owner, your mortgage payment is a form of ‘forced savings’ which allows you to build equity in your home that you can tap into later in life. As a renter, you guarantee the landlord is the person building that equity.

How much house can you afford?

Interest rates are still at historic lows, making it one of the best times to secure a mortgage and make a move into your dream home. Freddie Mac’s latest report shows that rates across the country were at 4.22% last week.

Bottom Line

Whether you are looking for a primary residence for the first time or are considering a vacation home on the shore, now may be the time to buy.

News and Advice

[frontpage_news widget=”6588″ name=”Housing Market News & Updates”]

Buying a home •

May 5, 2017

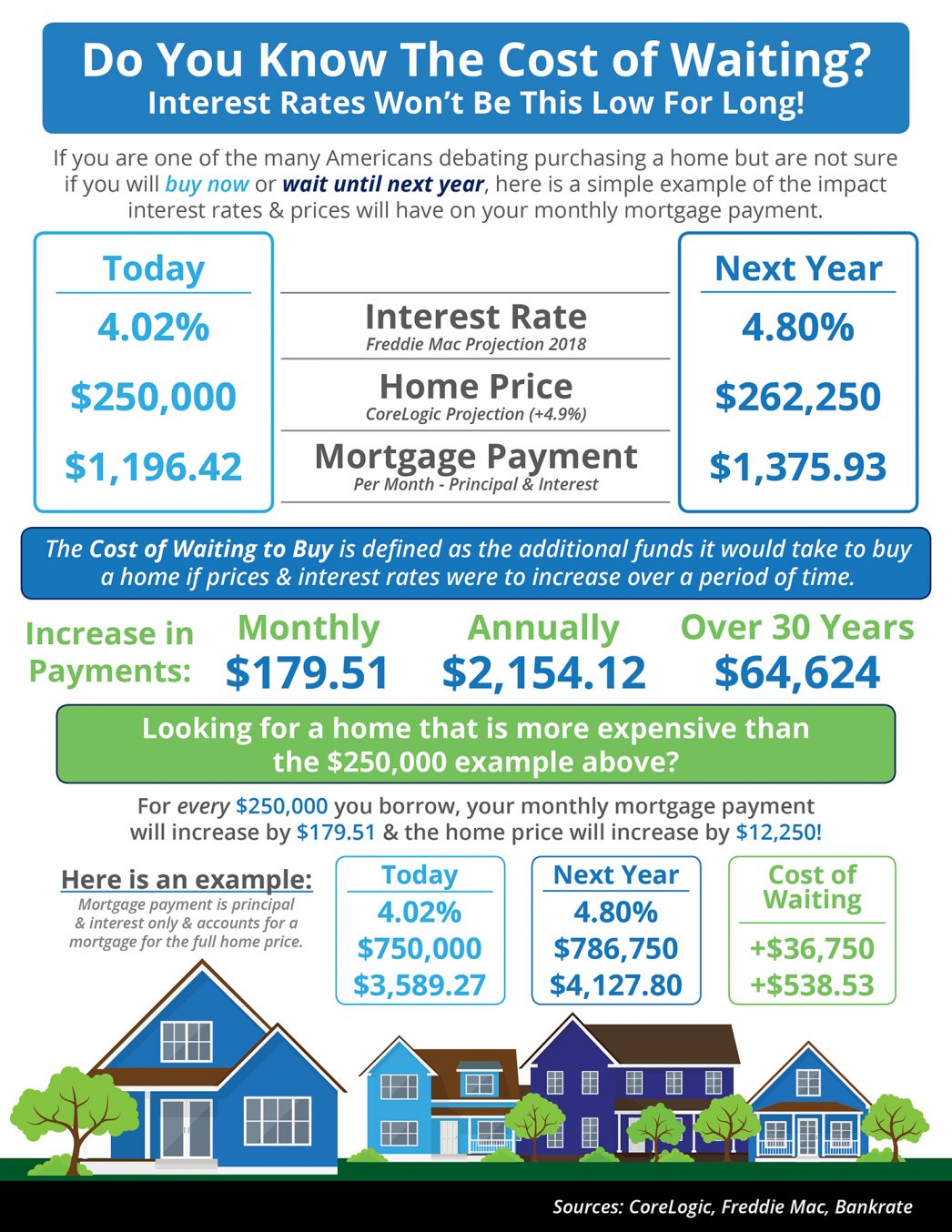

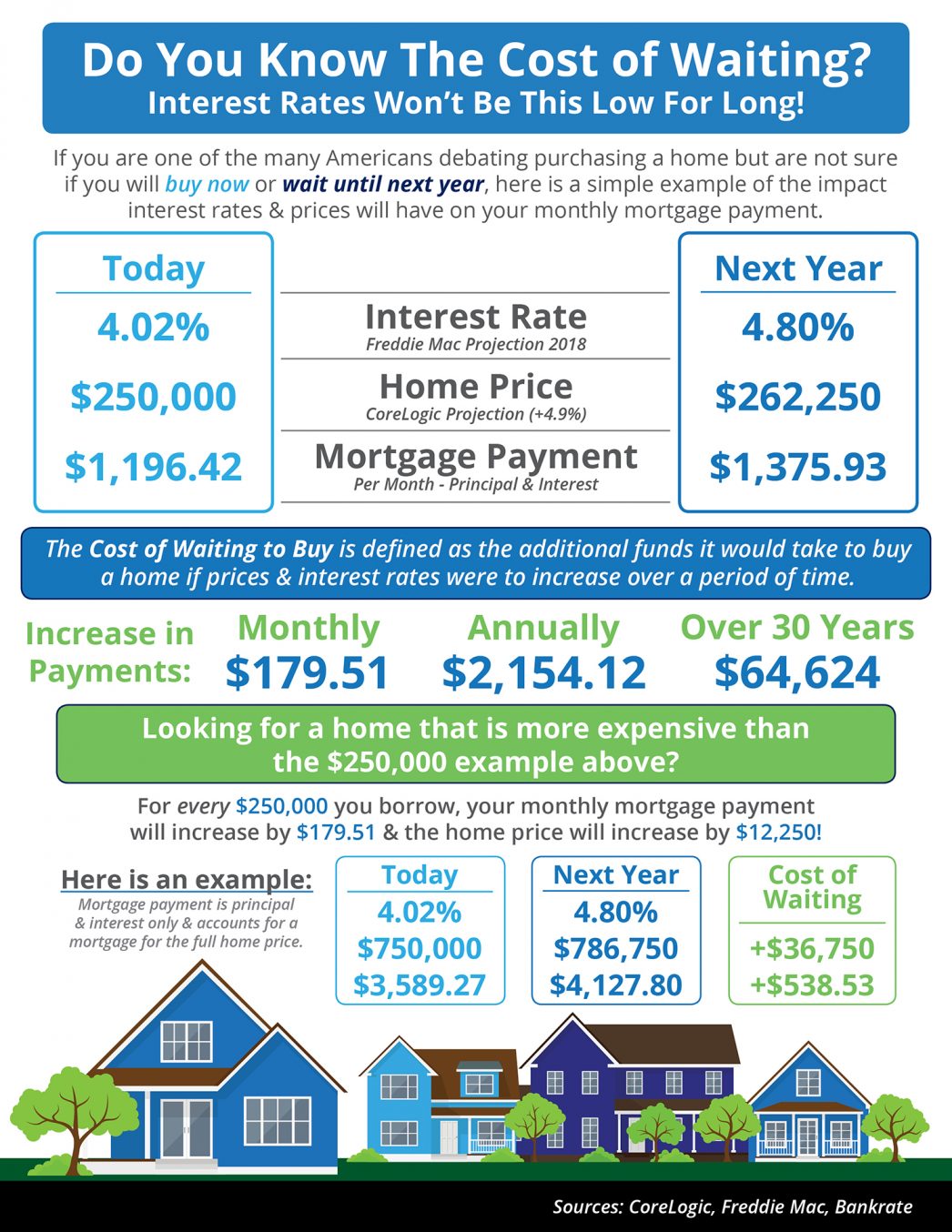

Do You Know the Cost of Waiting? [INFOGRAPHIC]

Some Highlights:

- The “Cost of Waiting to Buy” is defined as the additional funds it would take to buy a home if prices and interest rates were to increase over a period of time.

- Freddie Mac predicts that interest rates will increase to 4.8% by this time next year, while home prices are predicted to appreciate by 4.9% according to CoreLogic.

- Waiting until next year to buy could cost you thousands of dollars a year for the life of your mortgage!