Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What Are the Best Options for Today’s First-Time Homebuyers?

If you’re looking to buy your first home, you’re likely balancing several factors. Because both mortgage rates and home prices have risen this year, it costs more to buy a home than it did even just a few months ago. But that doesn’t mean you have to put your plans on hold.

If you partner with a trusted real estate advisor and hone your strategy, you can navigate today’s market and find the home you’re looking for. Here are two tips to help you get started.

Work with a Professional To Prioritize Your Wish List

If you’re having trouble finding a home in your budget that checks all the boxes, it may be worth taking another look at your lists of what you want and what you really need. According to the latest First-Time Homebuyer Metro Affordability Report from NerdWallet, your wish list can have as much impact on your search as your finances:

“Your budget isn’t all that you need to be concerned about; your wish list and desired location may carry just as much weight.”

It’s all about prioritization. If you’re serious about purchasing your first home soon, be flexible in what you’re looking for to open up your pool of options. Partner with a local real estate professional to better understand what’s available in today’s market and reprioritize your wish list. Remember, making a concession now doesn’t mean you’ll never have everything on your list. After you’ve moved in, you can always add certain features to make the home your own.

Increase Your Search Radius To Consider More Locations

Some areas may have more homes within your target price range than others, but it may require you to be flexible on your location. For example, if you’re a remote worker, you may be able to expand your search radius. As Fannie Mae explains:

“. . . continued remote work flexibility is likely giving many the ability to live farther away in more affordable areas.”

The decision to search in places with a lower cost of living could help you find a home that fits your budget and checks the most boxes off your wish list.

Bottom Line

If you’re serious about purchasing your first home this year, revisiting your wish list and desired location can help. Let’s connect to explore all the options in our local market – and beyond – so you can achieve your homeownership dreams.

May 2022 Housing Market Update

Geoff Green, the moderator of the monthly Housing Market webinar, is a real estate expert and entrepreneur. And, he is joined for the May 2022 Housing Market Update by Keren Gonen, Green Team New Jersey Realty; Vikki Garby, Green Team New York Realty; Chad Barris, Family First Funding, and Ken Ford, Warwick Valley Financial Advisors.

If you haven’t seen the May 2022 Housing Market Update yet or would like to watch it again, it’s available below. In addition, the Housing Market News section of the Green Team Realty website includes prior HMU recap blogs.

Furthermore, you can sign up to receive updates at HMupdate.com.

The big question… Are we headed for a Housing Bubble?

Of course, it would be wonderful if the panel was able to provide a simple “Yes” or “No” answer. However, there are too many variables to predict whether or not we are headed toward a Housing Bubble.

At each monthly Housing Market Update, Geoff asks mortgage experts if they are seeing a return to the lending practices that contributed to the 2008 housing market crash. To date, there has been no such return to those lending standards.

Furthermore, Geoff shares stats that may impact the answer to the Housing Bubble question. This includes home price appreciation and performance. Also, foreclosure activity is now at an all-time low.

“Housekeeping” Items

The June Housing Market Update will take place on Friday, June 17. Sign up now at HMupdate.com. Again, thanks to NuOp, Sponsor of the Housing Market Update.

Why Home Loans Today Aren’t What They Were in the Past

In today’s housing market, many are beginning to wonder if we’re returning to the riskier lending habits and borrowing options that led to the housing crash 15 years ago. Let’s ease those concerns.

Several times a year, the Mortgage Bankers Association (MBA) releases an index titled the Mortgage Credit Availability Index (MCAI). According to their website:

“The MCAI provides the only standardized quantitative index that is solely focused on mortgage credit. The MCAI is . . . a summary measure which indicates the availability of mortgage credit at a point in time.”

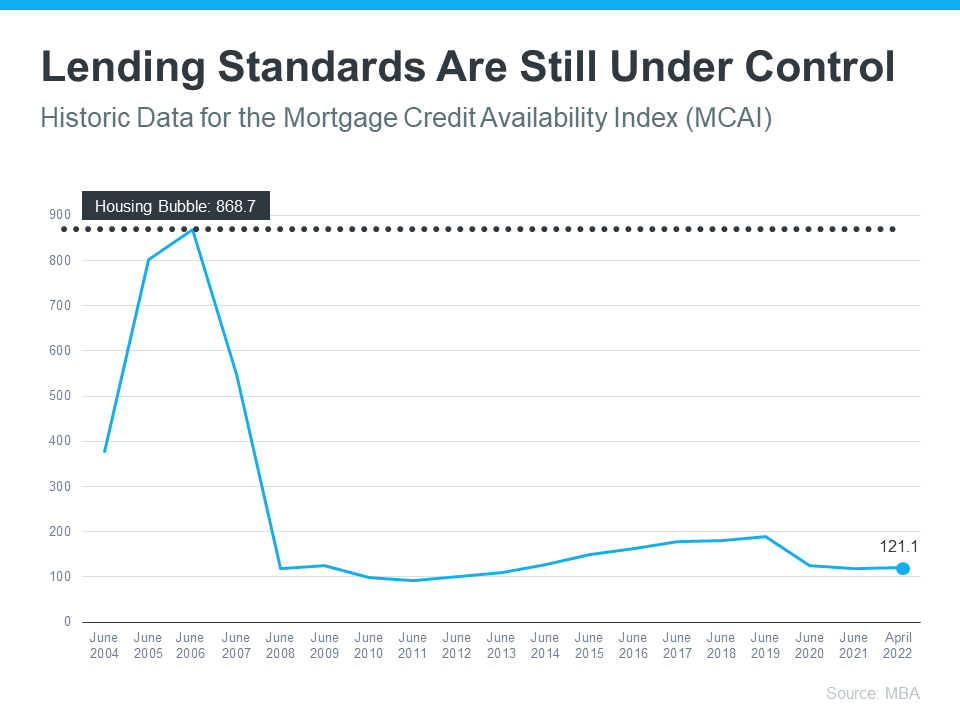

Basically, the index determines how easy it is to get a mortgage. The higher the index, the more available mortgage credit becomes. Here’s a graph of the MCAI dating back to 2004, when the data first became available:

As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006.

As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006.

Why Did the Index Get out of Control During the Housing Bubble?

The main reason was the availability of loans with extremely weak lending standards. To keep up with demand in 2006, many mortgage lenders offered loans that put little emphasis on the eligibility of the borrower. Lenders were approving loans without always going through a verification process to confirm if the borrower would likely be able to repay the loan.

An example of the relaxed lending standards leading up to the housing crash is the FICO® credit score associated with a loan. What’s a FICO® score? The website myFICO explains:

“A credit score tells lenders about your creditworthiness (how likely you are to pay back a loan based on your credit history). It is calculated using the information in your credit reports. FICO® Scores are the standard for credit scores—used by 90% of top lenders.”

During the housing boom, many mortgages were written for borrowers with a FICO score under 620. While there are still some loan programs that allow for a 620 score, today’s lending standards are much tighter. Lending institutions overall are much more attentive about measuring risk when approving loans. According to the latest Household Debt and Credit Report from the New York Federal Reserve, the median credit score on all mortgage loans originated in the first quarter of 2022 was 776.

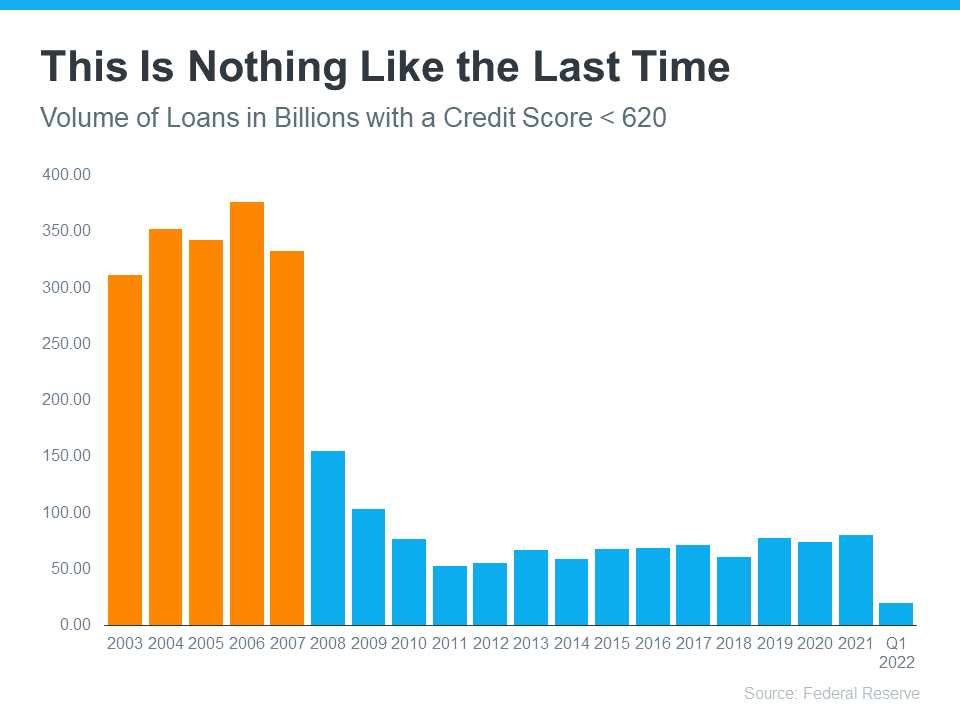

The graph below shows the billions of dollars in mortgage money given annually to borrowers with a credit score under 620.

In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

Bottom Line

In 2006, lending standards were much more relaxed with little evaluation done to measure a borrower’s potential to repay their loan. Today, standards are tighter, and the risk is reduced for both lenders and borrowers. These are two very different housing markets, and today is nothing like the last time.

Sellers Have an Opportunity with Today’s Home Prices

As mortgage rates started to rise this year, many homeowners began to wonder if the value of their homes would fall. Here’s the good news. Historically, when mortgage rates rise by a percentage point or more, home values continue to appreciate. The latest data on home prices seems to confirm that trend.

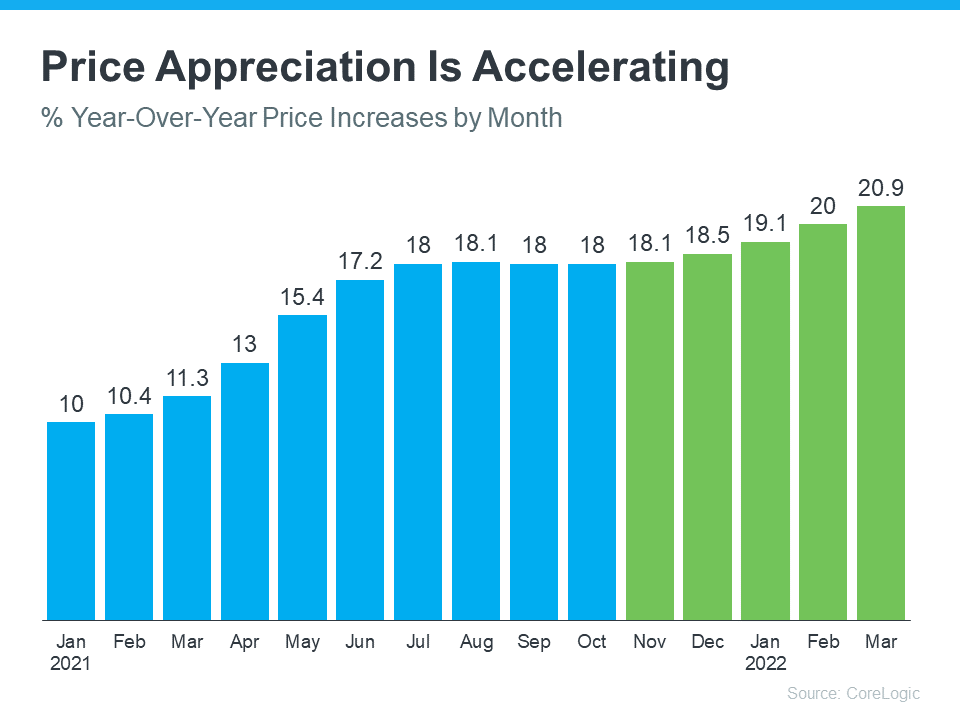

According to data from CoreLogic, home price appreciation has been re-accelerating since November. The graph below shows this increase in home price appreciation in green:

This is largely due to an ongoing imbalance in supply and demand. Specifically, housing supply is still low, and demand is high. As mortgage rates started to rise this year, many homebuyers rushed to make their purchases before those rates could climb higher. The increased competition drove home prices up even more. Selma Hepp, Deputy Chief Economist at CoreLogic, explains:

This is largely due to an ongoing imbalance in supply and demand. Specifically, housing supply is still low, and demand is high. As mortgage rates started to rise this year, many homebuyers rushed to make their purchases before those rates could climb higher. The increased competition drove home prices up even more. Selma Hepp, Deputy Chief Economist at CoreLogic, explains:

“Home price growth continued to gain speed in early spring, as eager buyers tried to get in front of the mortgage rate surge.”

And experts say prices are forecast to continue appreciating, just at a more moderate pace moving forward. A recent article from Fortune says:

“. . . the swift move up in mortgage rates . . . doesn’t mean home prices are about to crash. In fact, every major real estate firm with a publicly released forecast model . . . still predicts home prices will climb further this year.”

What This Means for You

If you’re thinking about selling your house, you should know you have a great opportunity to list your home and capitalize on today’s home price appreciation. As prices rise, so does the value of your home, which gives your equity a big boost.

When you sell, you can use that equity toward the purchase of your next home. And at today’s record-level of appreciation, that equity may be enough to cover some (if not all) of your down payment.

Bottom Line

History shows rising mortgage rates have not had a negative impact on home prices. Now is still a great time to sell your house thanks to ongoing price appreciation. When you’re ready to find out how much equity you have in your current home and what’s happening with home prices in your local area, let’s connect.

Don’t Let Rising Inflation Delay Your Homeownership Plans [INFOGRAPHIC]

![Don’t Let Rising Inflation Delay Your Homeownership Plans INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/05/18153723/20220520-MEM-1046x2334.png)

Some Highlights

- If recent headlines about rising inflation are making you wonder if it’s still a good time to buy, here’s what experts have to say.

- Housing is an asset that typically grows in value. Plus, your mortgage helps stabilize your monthly housing costs, and buying protects you from rising rents.

- Experts say owning a home is historically a good hedge against inflation. Let’s connect if you’re ready to start the homebuying process today.

The One Thing Every Homeowner Needs To Know About a Recession

A recession does not equal a housing crisis. That’s the one thing that every homeowner today needs to know. Everywhere you look, experts are warning we could be heading toward a recession, and if true, an economic slowdown doesn’t mean homes will lose value.

The National Bureau of Economic Research (NBER) defines a recession this way:

“A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.”

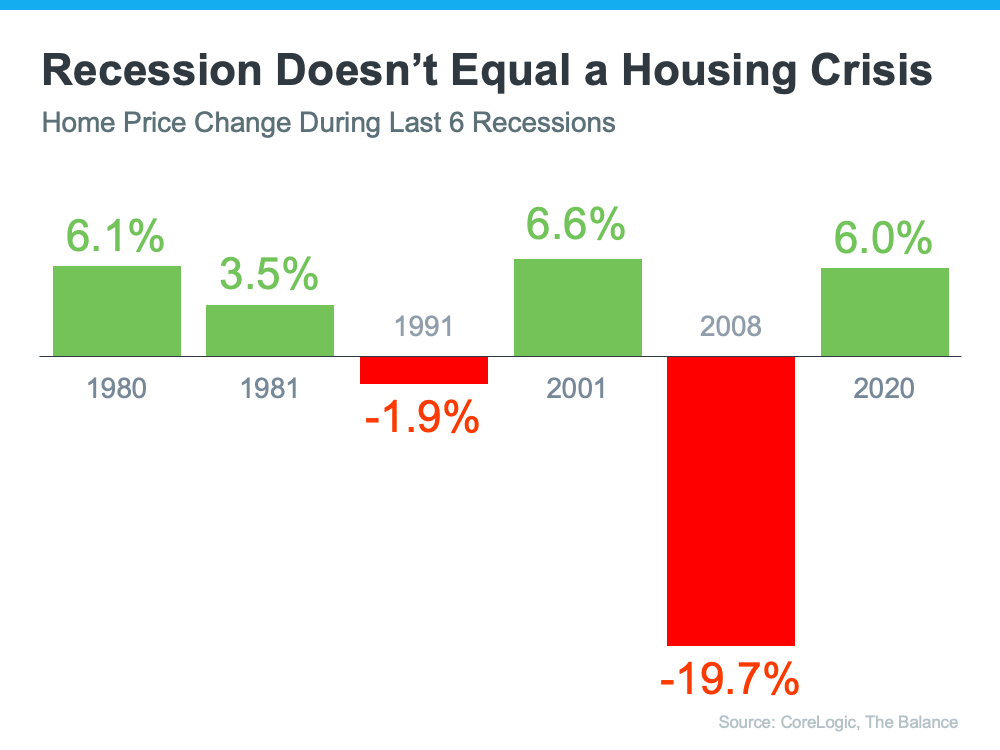

To help show that home prices don’t fall every time there’s a recession, take a look at the historical data. There have been six recessions in this country over the past four decades. As the graph below shows, looking at the recessions going all the way back to the 1980s, home prices appreciated four times and depreciated only two times. So, historically, there’s proof that when the economy slows down, it doesn’t mean home values will fall or depreciate.

The first occasion on the graph when home values depreciated was in the early 1990s when home prices dropped by less than 2%. It happened again during the housing crisis in 2008 when home values declined by almost 20%. Most people vividly remember the housing crisis in 2008 and think if we were to fall into a recession that we’d repeat what happened then. But this housing market isn’t a bubble that’s about to burst. The fundamentals are very different today than they were in 2008. So, we shouldn’t assume we’re heading down the same path.

Bottom Line

We’re not in a recession in this country, but if one is coming, it doesn’t mean homes will lose value. History proves a recession doesn’t equal a housing crisis.

Why Rising Mortgage Rates Push Buyers off the Fence

If you’re thinking about buying a home, you’ve probably heard mortgage rates are rising and have wondered what that means for you. Since mortgage rates have increased over two percentage points this year, it’s natural to think about how this will impact your homeownership plans.

Today, buyers are reacting in one of two ways: they’re either making the decision to buy now before rates climb higher or they’re waiting it out in hopes rates will fall. Let’s look at some context that can help you understand why so many buyers are jumping off the fence and into action rather than waiting to buy.

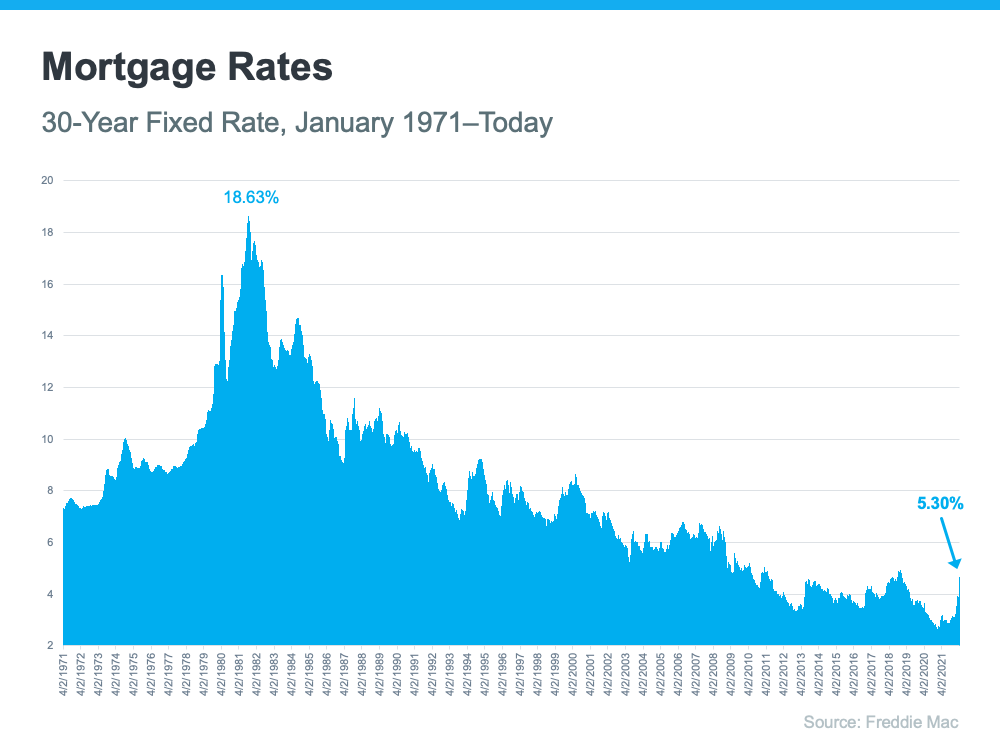

A Look Back: How the Current Mortgage Rate Compares to Historical Data

One factor that could help you make your decision to buy now is how today’s mortgage rates compare to historical data. While higher than the average 30-year fixed rate in recent years, the latest rates are still comparatively low when you look at the bigger picture of where rates have been since 1971 (see graph below):

Mark Fleming, Chief Economist at First American, explains it like this:

“. . . historical context is important. An average 30-year, fixed mortgage rate of 5.5 percent is still well below the historical average of nearly 8 percent.”

If you’re deciding whether to buy now or wait, this is important context to have. Today’s mortgage rate still gives you a window of opportunity to lock in a rate that’s comparatively lower than decades past.

A Look Ahead: What Happens if Rates Climb Further

The buyers who are springing into action now are also motivated to make their move because they know rates have risen steadily this year, and they’re eager to get ahead of any further increases.

Why? When mortgage rates climb, they impact the monthly mortgage payment you’ll have on the home you’re buying. Basically, it’ll likely cost you more to buy a home if you wait. Experts say mortgage rates will rise (although more moderately) in the months ahead. Odeta Kushi, Deputy Chief Economist at First American, explains:

“. . . ongoing inflationary pressure remains likely to push mortgage rates even higher in the months to come.”

So, if you’re ready and financially able to buy now, it may make more sense to get off the fence and make your purchase sooner rather than later. As Nadia Evangelou, Senior Economist at the National Association of Realtors (NAR), says:

“With even higher interest rates on the horizon, I don’t see any reason to hold off from purchasing a home right now. If you feel financially secure, you should start looking for a home.”

At the end of the day, there is no perfect advice on when to buy a home. What you should do depends on your goals, your finances, and your personal situation. Use this information with the help of local real estate professionals to make an informed decision on what’s best for you. The Mortgage Reports sums it up best:

“. . . if you’re on the fence about whether to buy now or wait for a better deal, buying sooner rather than later might be wise. That said, home buying is always a personal decision. Whether you should buy in 2022 depends on your financial situation and the local housing market where you live.”

Bottom Line

For many buyers, rising mortgage rates are motivating them to act now and make a purchase before rates rise higher. To decide what move is best for you, let’s connect so you have expert advice on your side.

If You’re a Homeowner, You Have Incredible Leverage When You Sell Today

In today’s housing market, homeowners have a great opportunity to sell their house and receive the best terms for their personal situation. That’s because there’s a limited number of homes for sale, which is creating competition among buyers. Right now, homebuyers want three things:

- To be the winning bid on their dream home

- To buy before mortgage rates rise more

- To buy before home prices go even higher

These buyer needs give you an amazing advantage – also known as leverage – when you sell.

What Does This Mean for Sellers Today?

You might already realize this enables you to sell at a good price, but you’re also in a great position to get the best terms to suit your needs.

According to the latest Realtors Confidence Index from the National Association of Realtors (NAR), the average home sold is receiving 4.8 offers. That’s why there’s a good chance you’ll get offers from multiple buyers who are willing to compete for your house. When you do, you should look closely at the terms of each offer to find out which one has the best options for you.

And if you have questions at any point in the process, remember your trusted real estate advisor can help. They’re experts who understand the fine print, know how to compare the terms of various offers, and will help you select the best one for your situation.

Bottom Line

If you’re thinking of selling your home, know buyer demand in today’s market gives you a great opportunity to get the best terms and price when you sell your house. Let’s connect today to discuss how much leverage you have as a seller in today’s market.

Should You Update Your House Before Selling? Ask a Real Estate Professional. [INFOGRAPHIC]

![Should You Update Your House Before Selling? Ask a Real Estate Professional. [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/05/11144408/20220513-MEM-1046x2120.png)

Some Highlights

- If you’re deciding whether you should make updates before you sell your house, lean on your trusted real estate advisor to be your guide.

- In today’s sellers’ market, buyers have limited options and may be more willing to take on repairs themselves.

- If you’re thinking about selling your house, let’s connect so you have expert advice that’s customized to your home and our local area.

What You Actually Need To Know About the Number of Foreclosures in Today’s Housing Market

While you may have seen recent stories about the volume of foreclosures today, context is important. During the pandemic, many homeowners were able to pause their mortgage payments using the forbearance program. The goal was to help homeowners financially during the uncertainty created by the health crisis.

When the forbearance program began, many experts were concerned it would result in a wave of foreclosures coming to the market, as there was after the housing crash in 2008. Here’s a look at why the number of foreclosures we’re seeing today is nothing like the last time.

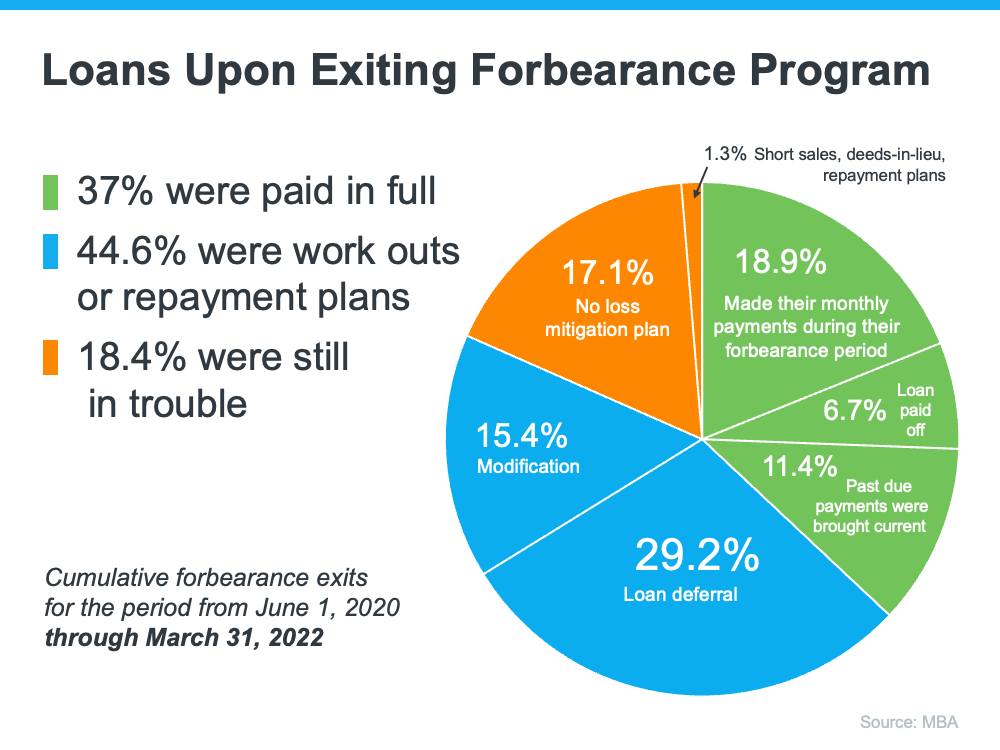

1. There Are Fewer Homeowners in Trouble

Today’s data shows that most homeowners are exiting their forbearance plan either fully caught up on payments or with a plan from the bank that restructured their loan in a way that allowed them to start making payments again. The graph below depicts those findings from the Mortgage Bankers Association (MBA):

The same MBA report mentioned above estimates there are approximately 525,000 homeowners who remain in forbearance today. Thankfully, those people still have the chance to work out a suitable repayment plan with the servicing company that represents their lender.

2. Most Homeowners Have Enough Equity To Sell Their Homes

For those who are exiting the forbearance program without a plan in place, many will have enough equity to sell their homes instead of facing foreclosures. Due to rapidly rising home prices over the last two years, the average homeowner has gained record amounts of equity in their home.

Marina Walsh, CMB, Vice President of Industry Analysis at MBA, says:

“Given the nation’s limited housing inventory and the variety of home retention and foreclosure alternatives on the table across various loan types, . . . Borrowers have more choices today to either stay in their homes or sell without resorting to a foreclosure.”

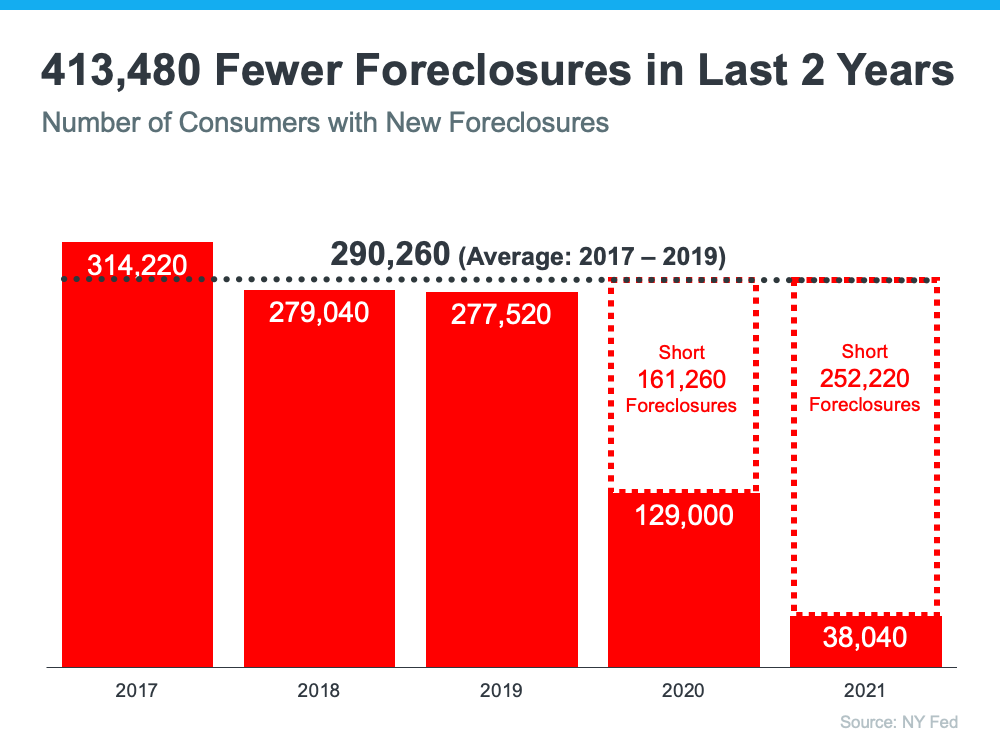

3. There Have Been Fewer Foreclosures over the Last Two Years

One of the seldom-reported benefits of the forbearance program was it gave homeowners facing difficulties an extra two years to get their finances in order and work out a plan with their lender. That helped prevent the foreclosures that normally would have come to the market had the new forbearance program not been available.

Even as people leave the forbearance program, there are still fewer foreclosures happening today than before the pandemic. That means, while there are more foreclosures now compared to last year (when foreclosures were paused), the number is still well below what the housing market has seen in a more typical year, like 2017-2019 (see graph below):

4. The Current Market Can Easily Absorb New Listings

When the foreclosures in 2008 hit the market, they added to the oversupply of houses that were already for sale. It’s exactly the opposite today. The latest Existing Home Sales Report from the National Association of Realtors (NAR) reveals:

“Total housing inventory at the end of March totaled 950,000 units, up 11.8% from February and down 9.5% from one year ago (1.05 million). Unsold inventory sits at a 2.0-month supply at the present sales pace, up from 1.7 months in February and down from 2.1 months in March 2021.”

A balanced market would have approximately a six-month supply of inventory. At 2.0 months, today’s housing market is severely understocked. Even if one million homes enter the market, there still won’t be enough inventory to meet the current demand.

Bottom Line

If you see headlines about the increasing number of foreclosures today, remember context is important. While it’s true the number of foreclosures is higher now than it was last year, foreclosures are still well below pre-pandemic years.

If you have questions, let’s connect to talk through the latest market conditions and what they mean for you.