Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Why Owning a Home Is a Powerful Financial Decision

In today’s housing market, there are clear financial benefits to owning a home: increasing equity, the chance to build your net worth, and appreciating home values, just to name a few. If you’re a renter, it’s never too early to think about how homeownership can propel you toward a stronger future. Here’s a dive into three often-overlooked financial benefits of homeownership and how preparing for them now can steer you in the direction of greater financial security and savings.

1. You Won’t Always Have a Monthly Housing Payment

Personal finance advisor Dave Ramsey explains:

“Every payment brings you closer to owning the house. When you pay your rent, that money is spent. Gone. Bye. Not returning. But when you pay your mortgage, you work toward full ownership.”

As a homeowner, you can eventually eliminate the monthly payment you make on your house. That’s a huge win and a big factor in how homeownership can drive stability and savings in your life. As soon as you buy a home, your monthly housing costs begin to work for you as forced savings in the form of equity. When you build equity and grow your net worth, you can continue to reinvest those savings into your future, maybe even by buying that next dream home. The possibilities are truly endless.

2. Homeownership Is a Tax Break

One thing people who have never owned a home don’t always think about are the tax advantages of homeownership. The same article states:

“You have tax advantages. Many of the costs of owning a home—like property taxes—are tax deductible. And if you’re paying off a mortgage, you’ll get to count your mortgage interest as a deduction when you file your tax return.”

Whether you’re living in your first home or your fifth, it’s a huge financial advantage to have some tax relief tied to the interest you pay each year. It’s one thing you definitely don’t get when you’re renting. Be sure to work with a tax professional to get the best possible benefits on your annual return.

3. Monthly Housing Costs Are Predictable

A third benefit is the fact that monthly costs start to become more predictable with homeownership, something that doesn’t happen if you’re renting. Ramsey also notes:

“Rent rates will go up. Even if you found a killer deal in a hot area, inflation, competition, and rising property values will cause your rent to go up year after year.”

With a mortgage, you can keep your monthly housing costs relatively steady and predictable. Your monthly costs are most likely based on a fixed-rate mortgage, which allows you to budget your finances over a longer period of time. Rental prices have been skyrocketing since 2012, and with today’s low mortgage rates, it’s a great time to get more for your money when purchasing a home. If you want to lock-in your monthly payment at a low rate and have a solid understanding of what you’re going to spend in your mortgage payment each month, buying a home may be your best bet.

Bottom Line

If you’re ready to start feeling the benefits of stability, savings, and predictability that come with owning a home, let’s connect to determine if buying sooner rather than later is right for you.

Contact one of Our Agents today!

Welcome Joseph Mackey

The Green Team is proud to announce that Joseph Mackey has decided to join our Vernon, NJ office. We’re excited to have him on our team and look forward to helping him grow!

Please join us in Welcoming Joseph Mackey to The Green Team New Jersey!

Welcome Barbara Matchett

The Green Team is proud to announce that Barbara Matchett has decided to join our Vernon, NJ office. We’re excited to have her on our team and look forward to helping her grow!

Please join us in Welcoming Barbara Matchett to The Green Team New Jersey!

How Smart Is It to Buy a Home Today?

Whether you’re buying your first home or selling your current house, if your needs are changing and you think you need to move, the decision can be complicated. You may have to take personal or professional considerations into account, and only you can judge what impact those factors should have on your desire to move.

However, there’s one category that provides a simple answer. When deciding to buy now or wait until next year, the financial aspect of the purchase is easy to evaluate. You just need to ask yourself two questions:

- Do I think home values will be higher a year from now?

- Do I think mortgage rates will be higher a year from now?

From a purely financial standpoint, if the answer is ‘yes’ to either question, you should strongly consider buying now. If the answer to both questions is ‘yes,’ you should definitely buy now.

Nobody can guarantee what home values or mortgage rates will be by the end of this year. The experts, however, seem certain the answer to both questions above is a resounding ‘yes.’ Mortgage rates are expected to rise and home values are expected to appreciate rather nicely.

What does this mean to you?

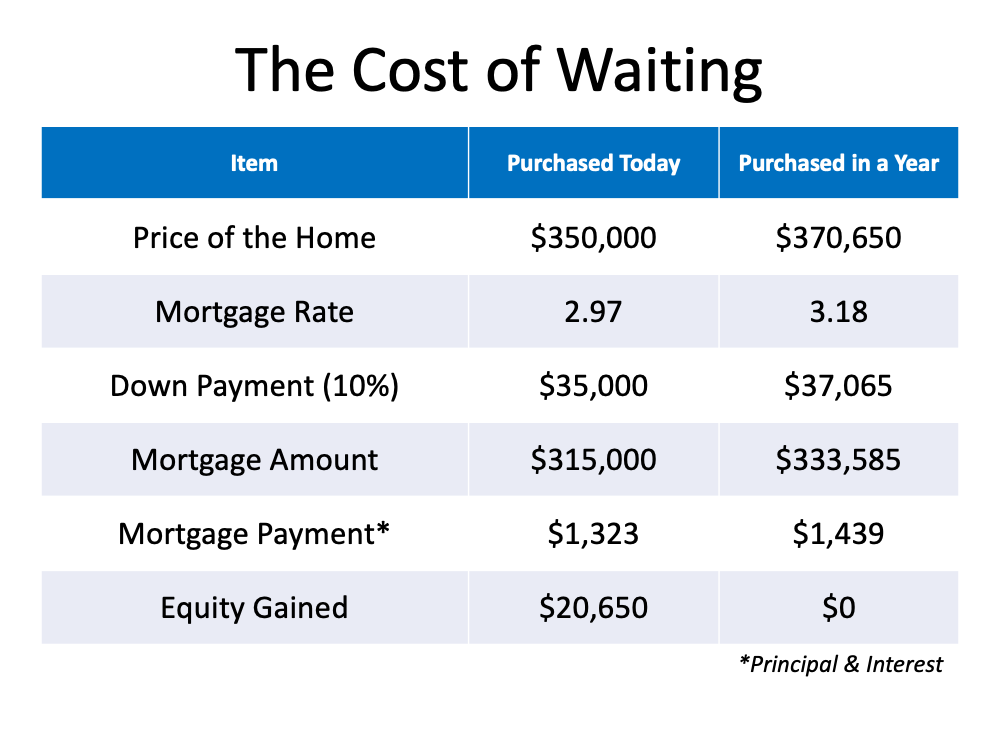

Let’s look at how waiting would impact your financial situation. Here are the assumptions made for this example:

- The experts are right – mortgage rates will be 3.18% at the end of the year

- The experts are right – home values will appreciate by 5.9%

- You want to buy a home valued at $350,000 today

- You decide on a 10% down payment

Here’s the financial impact of waiting:

Here’s the financial impact of waiting:

- You pay an extra $20,650 for the house

- You need an additional $2,065 for a down payment

- You pay an extra $116/month in your mortgage payment ($1,392 additional per year)

- You don’t gain the $20,650 increase in wealth through equity build-up

Bottom Line

There are many things to consider when buying a home. However, from a purely financial aspect, if you find a home that meets your needs, buying now makes much more sense than buying next year.

Contact one of Our Agents today!

Welcome Amy Klypka

The Green Team is proud to announce that Amy Klypka has decided to join our Vernon, NJ office. We’re excited to have her on our team and look forward to helping her grow!

Please join us in Welcoming Amy Klypka to The Green Team New Jersey!

Welcome Joseph Gorman

The Green Team is proud to announce that Joseph Gorman has decided to join our Warwick, NY office. We’re excited to have him on our team and look forward to helping him grow!

Please join us in Welcoming Joseph Gorman to The Green Team New York!

Home Mortgage Rates by Decade

![Home Mortgage Rates by Decade [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/02/18124453/20210219-MEM-1046x1207.png)

Some Highlights

- Mortgage interest rates have dropped considerably over the past year, and compared to what we’ve seen in recent decades, it’s a great time to buy a home.

- Locking in a low rate today could save you thousands of dollars over the lifetime of your home loan, but these low rates may not last forever.

- If you’re in a position to buy a home, let’s connect to determine your best move in today’s housing market while interest rates are still in your favor.

Contact one of Our Agents today!

Home Prices: What Happened in 2020? What Will Happen This Year?

The real estate market was on fire during the second half of 2020. Buyer demand was way up, and the supply of homes available for sale hit record lows. The price of anything is determined by the supply and demand ratio, so home prices skyrocketed last year. Dr. Lynn Fisher, Deputy Director of the Federal Housing Finance Agency (FHFA) Division of Research and Statistics, explains:

“House prices nationwide recorded the largest annual and quarterly increase in the history of the FHFA Home Price Index. Low mortgage rates, pent up demand from homebuyers, and a limited housing supply propelled every region of the country to experience faster growth in 2020 compared to a year ago despite the pandemic.”

Here are the year-end home price appreciation numbers from the FHFA and two other prominent pricing indexes:

- Federal Housing Finance Agency House Price Index Report: 10.8%

- CoreLogic Home Price Insights: 9.2%

- S&P Case-Shiller U.S. National Home Price Index: 10.4%

The past year was truly a remarkable time for homeowners as prices appreciated substantially. Lawrence Yun, Senior Economist at the National Association of Realtors (NAR), reveals:

“A typical homeowner in 2020, just by being a homeowner, would have accumulated around $24,000 in housing wealth.”

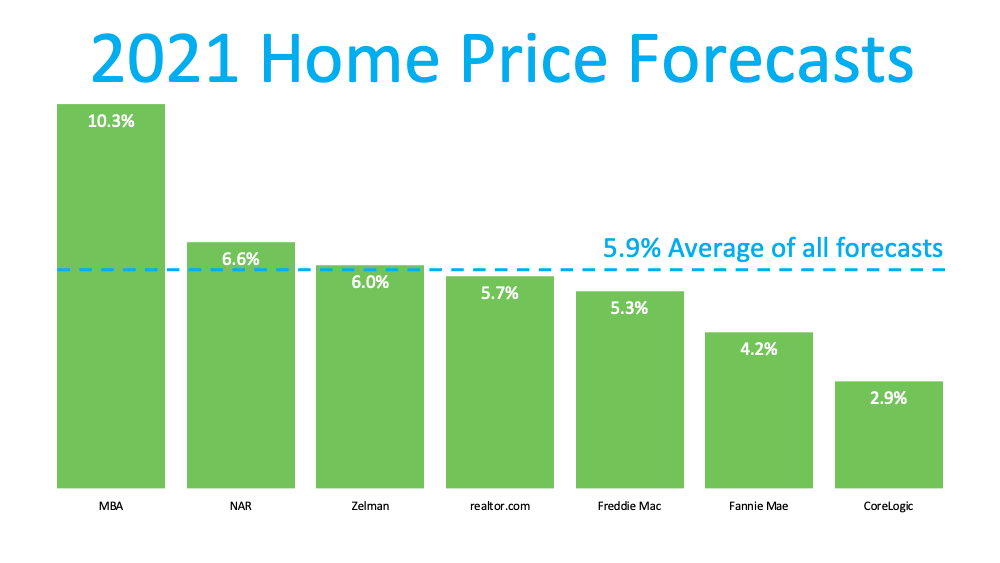

What will happen with home prices this year?

Many experts believe buyer demand will soften somewhat as mortgage rates are poised to bump up slightly. Some also believe the inventory challenge will ease as more listings come to market this year.

Based on this, most forecasters anticipate we’ll see strong appreciation in 2021 – but not as strong as last year. Here are seven prominent groups and their projections:

Bottom Line

Home price appreciation will be strong this year, but it won’t reach the historic levels of 2020. Let’s connect if you’d like to find out what your house is currently worth in our local market.

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams.

What’s your home’s value?

What Are the Benefits of a 20% Down Payment?

If you’re thinking of buying a home this year, you may be wondering how much money you need to come up with for your down payment. Many people may think it’s 20% of the loan to secure a mortgage. While there are plenty of lower down payment options available for qualified buyers who don’t want to put 20% down, it’s important to understand how a larger down payment can have great benefits too.

The truth is, there are many programs available that allow you to put down as little as 3.5%, which can be a huge benefit to those who want to purchase a home sooner rather than later. Those who have served our country may also qualify for a Veterans Affairs Home Loan (VA) and may not need a down payment. These programs have really cut down the savings time for many potential buyers, enabling them to start building family wealth sooner.

Here are four reasons why putting 20% down is a good plan if you can afford it.

1. Your interest rate may be lower.

A 20% down payment vs. a 3-5% down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage interest rate they’ll likely be willing to give you.

2. You’ll end up paying less for your home.

The larger your down payment, the smaller your loan amount will be for your mortgage. If you’re able to pay 20% of the cost of your new home at the start of the transaction, you’ll only pay interest on the remaining 80%. If you put down 5%, the additional 15% will be added to your loan and will accrue interest over time. This will end up costing you more over the lifetime of your home loan.

3. Your offer will stand out in a competitive market.

In a market where many buyers are competing for the same home, sellers like to see offers come in with 20% or larger down payments. The seller gains the same confidence as the lender in this scenario. You are seen as a stronger buyer with financing that’s more likely to be approved. Therefore, the deal will be more likely to go through.

4. You won’t have to pay Private Mortgage Insurance (PMI)

What is PMI? According to Freddie Mac:

“PMI is an insurance policy that protects the lender if you are unable to pay your mortgage. It’s a monthly fee, rolled into your mortgage payment, that is required for all conforming, conventional loans that have down payments less than 20%. Once you’ve built equity of 20% in your home, you can cancel your PMI and remove that expense from your mortgage payment.”

As mentioned earlier, when you put down less than 20% when buying a home, your lender will see your loan as having more risk. PMI helps them recover their investment in you if you’re unable to pay your loan. This insurance isn’t required if you’re able to put down 20% or more.

Many times, home sellers looking to move up to a larger or more expensive home are able to take the equity they earn from the sale of their house to put down 20% on their next home. With the equity homeowners have today, it creates a great opportunity to put those savings toward a 20% or greater down payment on a new home.

If you’re looking to buy your first home, you’ll want to consider the benefits of 20% down versus a smaller down payment option.

Bottom Line

If you’re thinking of buying a home and are already saving for your down payment, let’s connect to discuss what fits best with your long-term plans.

Contact one of Our Agents today!

The Reason Mortgage Rates Are Projected to Increase and What It Means for You

We’re currently experiencing historically low mortgage rates. Over the last fifty years, the average on a Freddie Mac 30-year fixed-rate mortgage has been 7.76%. Today, that rate is 2.81%. Flocks of homebuyers have been taking advantage of these remarkably low rates over the last twelve months. However, there’s no guarantee rates will remain this low much longer.

Whenever we try to forecast mortgage rates, we should consider the advice of Mark Fleming, Chief Economist at First American:

“You know, the fallacy of economic forecasting is don’t ever try and forecast interest rates and/or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

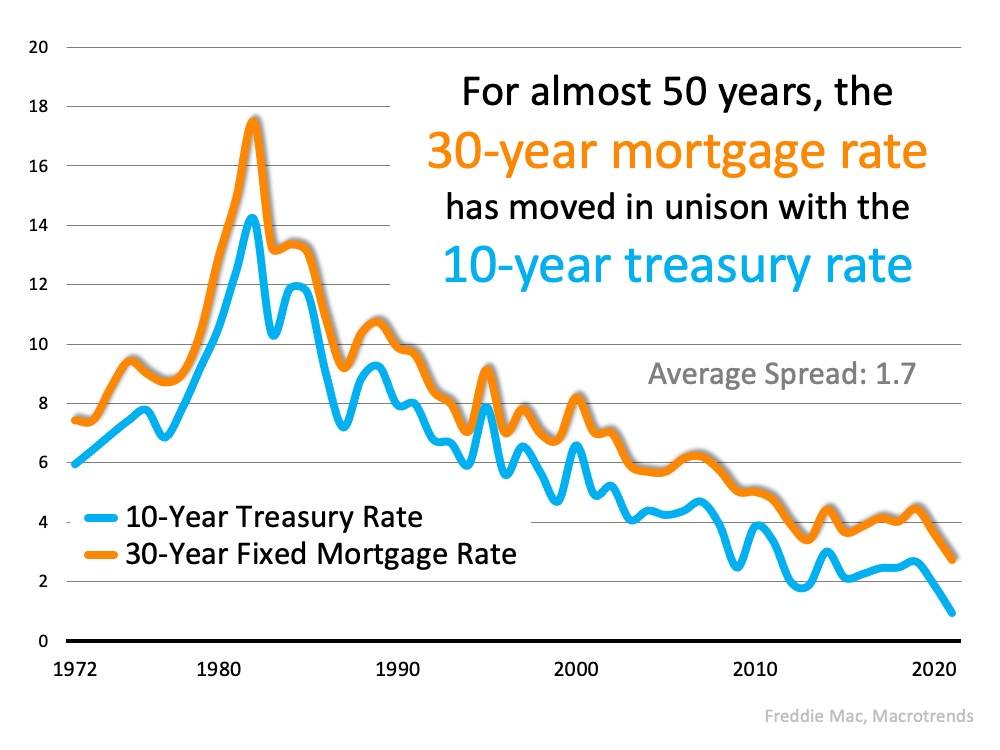

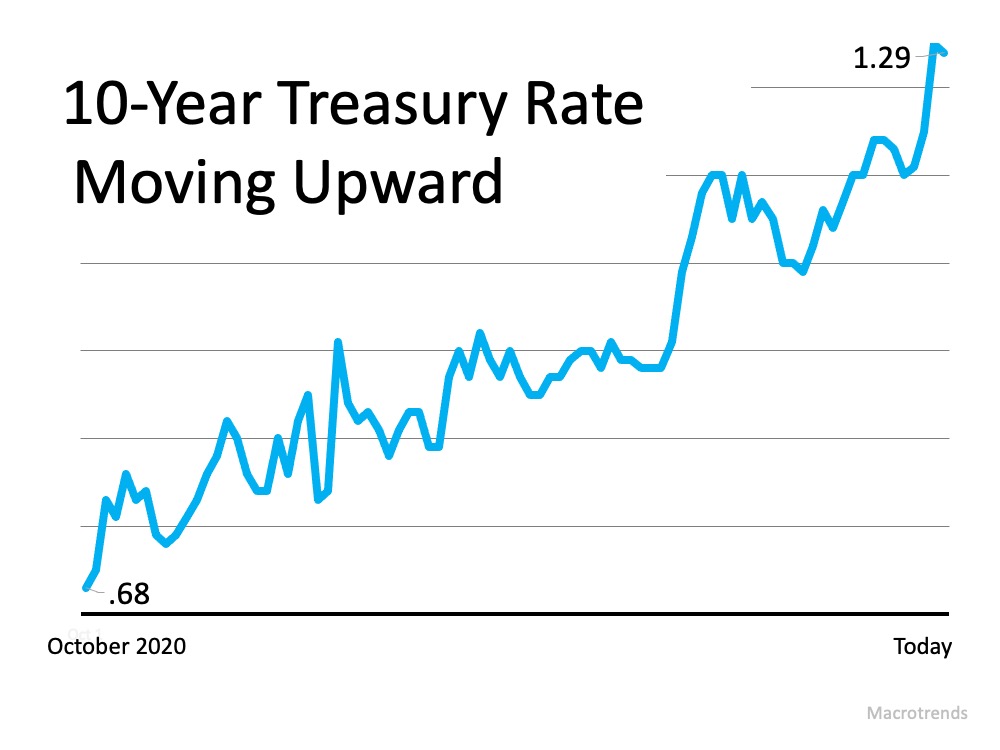

Many things impact mortgage rates. The economy, inflation, and Fed policy, just to name a few. That makes forecasting rates difficult. However, there’s one metric that has held up over the last fifty years – the relationship between mortgage rates and the 10-year treasury rate. Here’s a graph detailing this relationship since Freddie Mac started keeping mortgage rate records in 1972: There’s no denying the close relationship between the two. Over the last five decades, there’s been an average 1.7-point spread between these two rates. It’s this long-term relationship that has some forecasters projecting an increase in mortgage rates as we move throughout the year. This is based on the recent surge in the 10-year treasury rate shown here:

There’s no denying the close relationship between the two. Over the last five decades, there’s been an average 1.7-point spread between these two rates. It’s this long-term relationship that has some forecasters projecting an increase in mortgage rates as we move throughout the year. This is based on the recent surge in the 10-year treasury rate shown here: The spread between the two is now 1.53, indicating mortgage rates could rise. Actually, a bump-up in rate has already begun. As Joel Kan, Associate VP of Economic Forecasting for the Mortgage Bankers Association, reveals:

The spread between the two is now 1.53, indicating mortgage rates could rise. Actually, a bump-up in rate has already begun. As Joel Kan, Associate VP of Economic Forecasting for the Mortgage Bankers Association, reveals:

“Expectations of faster economic growth and inflation continue to push Treasury yields & mortgage rates higher. Since hitting a survey low in December, the 30-year fixed rate has slowly risen, & last week climbed to its highest level since Nov 2020.”

How high might they go in 2021?

No one knows for sure. Sam Khater, Chief Economist for Freddie Mac, recently suggested:

“While there are multiple temporary factors driving up rates, the underlying economic fundamentals point to rates remaining in the low 3% range for the year.”

What does this mean for you?

Whether you’re a first-time buyer or you’ve purchased a home before, even an increase of half a point in mortgage rate (2.81 to 3.31%) makes a big difference. On a $300,000 mortgage, that difference (including principal and interest) is $82 a month, $984 a year, or a total of $29,520 over the life of the home loan.

Bottom Line

Based on the 50-year symbiotic relationship between treasury rates and mortgage rates, it appears mortgage rates could be headed up this year. It may make sense to buy now rather than wait.

Contact one of Our Agents today!