Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Homeownership Could Be in Reach with Down Payment Assistance Programs

A recent survey from Bankrate asks prospective buyers to identify the biggest obstacles in their homebuying journey. It found that 36% of those polled said saving for a down payment is one of their primary hurdles to buying a home.

If you feel the same way, the good news is there are many down payment assistance programs available that can help you achieve your homeownership goals. The key is understanding where to look and learning what options are available. Here’s some information that can help you.

You Can Qualify Even if You’ve Purchased a Home Before

There are several misconceptions about down payment assistance programs. For starters, many people believe there’s only assistance available for first-time homebuyers. While first-time buyers have many options to explore, repeat buyers have some, too. According to the latest Homeownership Program Index from downpaymentresource.com:

“It is a common misconception that homebuyer assistance is only available to first-time homebuyers, however, 38% of homebuyer assistance programs in Q1 2022 did not have a first-time homebuyer requirement.”

That means repeat buyers could qualify for over one-third of the assistance programs available. And if you’re a repeat buyer, you may still be able to take advantage of some first-time homebuyer programs, depending on your personal situation. That’s because downpaymentresource.com also notes many of the first-time homebuyer programs use the U.S. Department of Housing and Urban Development’s definition of a first-time homebuyer. Under their definition, you could qualify as a first-time buyer if you’re:

- Someone who hasn’t owned a primary residence in 3 years.

- A single parent who’s only ever owned a home with a former spouse.

That means no matter where you are in your homeownership journey, there could be an option available for you.

You May Be Eligible for Programs Based on Your Location or Profession

In addition to broader options available for repeat and first-time homebuyers, there are other types of down payment assistance programs that you could qualify for based on your location. According to the National Association of Realtors (NAR):

“Many local governments and non-profit organizations offer down-payment assistance grants and loans, targeted to area borrowers and often with specific borrower requirements.”

Plus, there are programs and special benefits for individuals working in certain professions or with unique statuses, including teachers, doctors and nurses, and veterans.

Ultimately, that means there are many federal, state, and local programs available for you to explore. The best way to do that is to connect with a local real estate professional and your lender to learn more about what’s available in your area.

Bottom Line

Down payment assistance programs have helped many homebuyers achieve their dreams, and if you qualify, they could help you too. Let’s connect today so you can begin exploring your options.

A Key Opportunity for Homebuyers

There’s no denying the housing market has delivered a fair share of challenges to homebuyers over the past two years. Two of the biggest hurdles homebuyers faced during the pandemic were the limited number of homes for sale and the intensity and frequency of bidding wars. But those two things have reached a turning point.

As you may have already heard, the number of homes for sale has increased this year, and even more so this spring. As Danielle Hale, Chief Economist for realtor.com, explains:

“New listings–a measure of sellers putting homes up for sale–were up 6% above one year ago. Home sellers in many markets across the country continue to benefit from rising home prices and fast-selling homes. That’s prompted a growing number of homeowners to sell homes this year compared to last, giving home shoppers much needed options.”

This is encouraging news. More homes coming onto the market give you a greater chance of finding one that checks all your boxes.

Buyer Competition Moderating Helps Inventory Grow Even More

Mark Fleming, Chief Economist at First American, says inventory growth is happening not just because there’s an increase in the number of listings coming onto the market, but also because buyer demand has moderated some in light of higher mortgage rates and other economic factors:

“There has been a pickup in the inventory that we’ve seen recently, but it’s not from a big increase in new listings . . . but rather a slowdown in the pace of sales. And remember that months’ supply measures the inventory of sale relative to the pace of sales. Same inventory, fewer sales, means more months’ supply.”

Basically, the market is shifting away from the frenzy of buyer competition seen during the pandemic, and that’s helping available inventory grow. In their latest forecast, realtor.com also mentions the moderation of demand as a key factor and projects the inventory growth should continue:

“As rising inflation and mortgage rates bring U.S. housing demand back from the 2021 frenzy, . . . inventory will grow double-digits over 2021 and offer buyers a better-than-expected chance to find a home.”

How This Impacts You

The combination of more homes coming onto the market and a slower pace of home sales means you’ll have more options to choose from as you search for your next home. That’s great news if you’ve been searching for a while with little to no luck. Just remember, there isn’t a sudden surplus of inventory, just more homes to choose from than even a few months ago. So, you’ll still want to be decisive and move fast when you find the right home for you.

And when you do, you may be faced with less competition from other buyers too. If you’ve been waiting to jump into the market because the intensity of the bidding wars was intimidating or if you’ve been outbid on several homes, this moderation could help make the homebuying process a bit smoother. It’s not that it’ll be easy or that bidding wars are a thing of the past – that’s not the case. But it won’t feel nearly as impossible.

Bottom Line

As the housing market begins its shift back toward pre-pandemic levels, you could have a unique opportunity in front of you. With moderating levels of buyer competition and more homes actively for sale, your home search may have gotten a bit less challenging. Let’s connect to begin the process today.

Homeownership Is a Great Hedge Against the Impact of Rising Inflation

If you’re following along with the news today, you’ve heard about rising inflation. Today, inflation is at a 40-year high. According to the National Association of Home Builders (NAHB):

“Consumer prices accelerated again in May as shelter, energy and food prices continued to surge at the fastest pace in decades. This marked the third straight month for inflation above an 8% rate and was the largest year-over-year gain since December 1981.”

With inflation rising, you’re likely feeling it impact your day-to-day life as prices go up for gas, groceries, and more. These climbing consumer costs can put a pinch on your wallet and make you re-evaluate any big purchases you have planned to ensure they’re still worthwhile.

If you’ve been thinking about purchasing a home this year, you’re probably wondering if you should continue down that path or if it makes more sense to wait. While the answer depends on your situation, here’s how homeownership can help you combat the rising costs that come with inflation.

Homeownership Helps You Stabilize One of Your Biggest Monthly Expenses

Investopedia explains that during a period of high inflation, prices rise across the board. That’s true for things like food, entertainment, and other goods and services, even housing. Both rental prices and home prices are on the rise. So, as a buyer, how can you protect yourself from increasing costs? The answer lies in homeownership.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. When you have a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same. That’s certainly not the case if you’re renting.”

So even if other prices increase, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

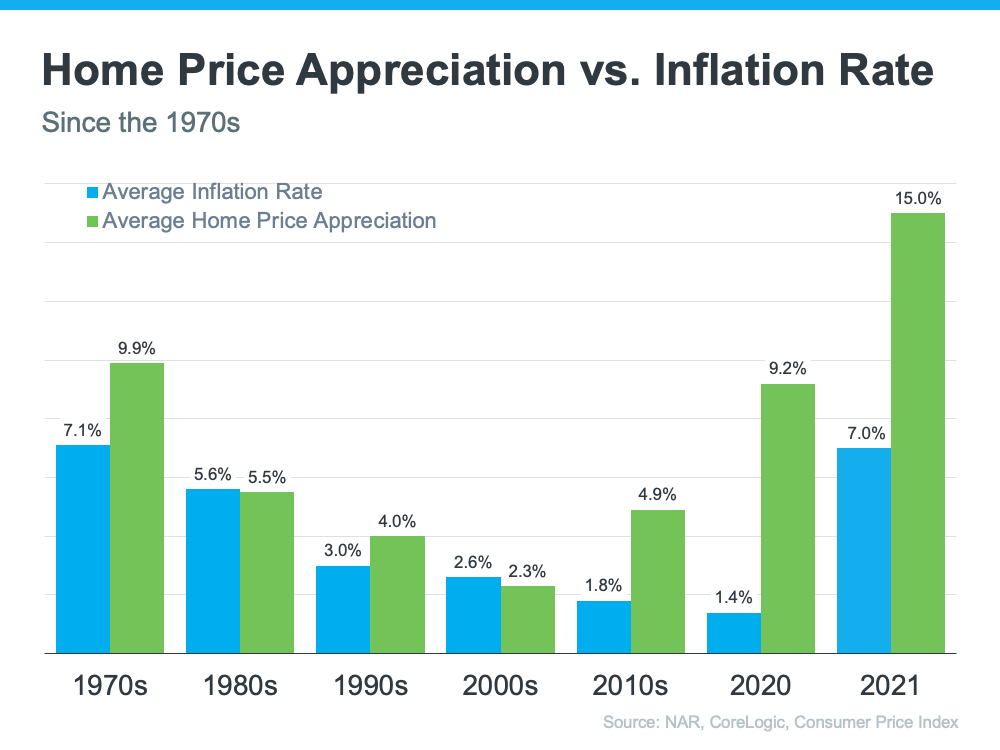

Investing in an Asset That Historically Outperforms Inflation

While it’s true rising home prices and higher mortgage rates mean that buying a house today costs more than it did even a few months ago, you still have an opportunity to set yourself up for a long-term win. That’s because, in inflationary times, you want to be invested in an asset that outperforms inflation and typically holds or grows in value.

The graph below shows how the average home price appreciation outperformed the average inflation rate in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

So, what does that mean for you? Today, experts forecast home prices will only go up from here thanks to the ongoing imbalance of supply and demand. Once you buy a house, any home price appreciation that does occur will grow your equity and your net worth. And since homes are typically assets that grow in value, you have peace of mind that history shows your investment is a strong one.

That means, if you’re ready and able, it makes sense to buy today before prices rise further.

Bottom Line

If you’ve been thinking about buying a home this year, it makes sense to act soon, even with inflation rising. That way you can stabilize your monthly housing cost and invest in an asset that historically outperforms inflation. If you’re ready to get started, let’s connect so you have expert advice on your specific situation when you’re ready to buy a home.

Things To Avoid After Applying for a Home Loan

Once you’ve applied for a mortgage to buy a home, there are some key things to keep in mind. While it’s exciting to start thinking about moving in and decorating, be careful when it comes to making any big purchases. Here are a few things you may not realize you need to avoid after applying for your home loan.

Don’t Deposit Large Sums of Cash

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

Don’t Make Any Large Purchases

It’s not just home-related purchases that could disqualify you from your loan. Any large purchases can be red flags for lenders. People with new debt have higher debt-to-income ratios (how much debt you have compared to your monthly income). Since higher ratios make for riskier loans, borrowers may no longer qualify for their mortgage. Resist the temptation to make any large purchases, even for furniture or appliances.

Don’t Co-Sign Loans for Anyone

When you co-sign for a loan, you’re making yourself accountable for that loan’s success and repayment. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count the payments against you.

Don’t Switch Bank Accounts

Lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

Don’t Apply for New Credit

It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), it will have an impact on your FICO® score. Lower credit scores can determine your mortgage interest rate and possibly even your eligibility for approval.

Don’t Close Any Accounts

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those aspects of your score.

In Short, Consult an Expert

To sum it up, be upfront about any changes when talking with your lender. Blips in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. Ultimately, it’s best to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

Bottom Line

You want your home purchase to go as smoothly as possible. Remember, before you make any large purchases, move your money around, or make any major life changes, be sure to consult your lender – someone who’s qualified to explain how your financial decisions may impact your home loan.

Why Achieving the Dream of Homeownership Can Be More Difficult for Some Americans

Today we take time to honor and recognize the past and present experiences of Black Americans. When it comes to real estate specifically, equitable access to housing has come a long way, but the path to homeownership is still steeper for households of color.

The Gap in Homeownership Rate in America

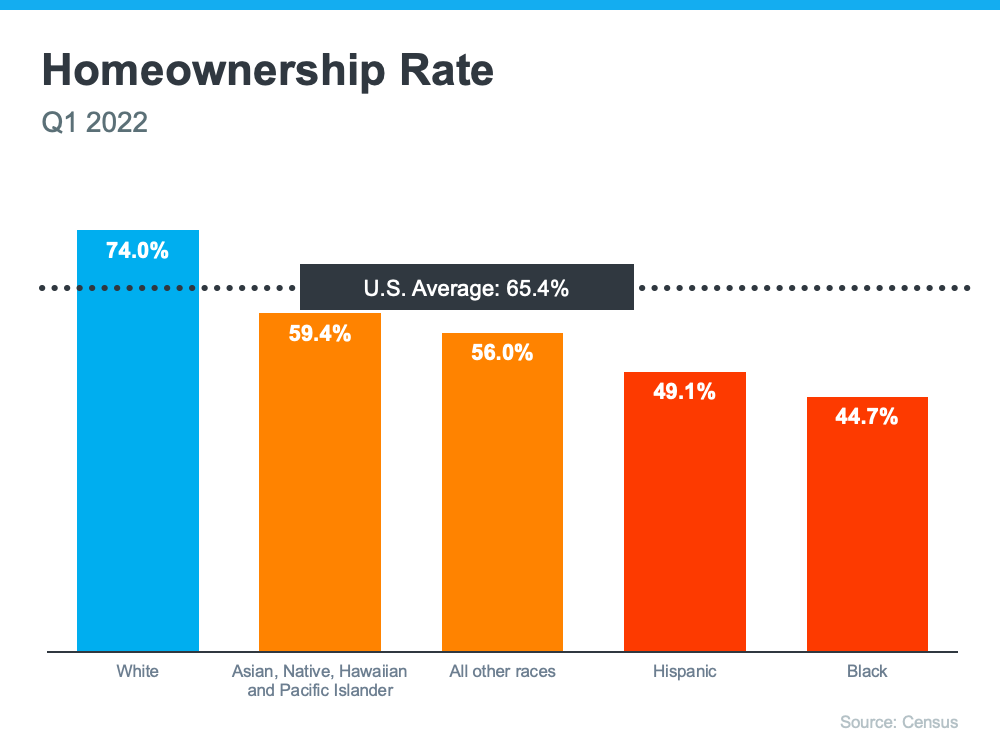

It’s a more challenging journey to achieve homeownership for some buyers, as shown by the measurable gap between the overall average U.S. homeownership rate and that of non-white groups. Today, Census data shows the lowest homeownership rate persists in the Black community (see graph below):

This graph clearly indicates there’s a gap that still exists in the percentage of people in each community who are able to achieve homeownership.

How Homeownership Impacts Household Wealth

One of the challenges that could make buying a home harder for these groups is how difficult it can be to accumulate wealth. Even today, there are obstacles certain racial and ethnic groups, especially the Black community, still face. A recent article from NextAdvisor explains:

“The median Black household earns 61 cents for every dollar earned by a comparable White household, according to the Economic Policy Institute. This not only makes it more difficult to afford a home, but also to accumulate and pass on generational wealth.”

This can delay or prevent many from achieving homeownership, challenging their ability to grow their net worth and build wealth that can pass down to future generations – a point that’s clear in a 2022 report from the National Association of Realtors (NAR):

“Given that homeownership contributes to wealth accumulation and the homeownership rate is lower in minority groups, data shows that the net worth for these groups is also lower. At $188,200, the net worth of a typical white family was nearly 8 times greater than that of a Black family ($24,100) in 2019.”

It’s important to talk about the experience Black homebuyers may have and the challenges they may face as they pursue their dream of homeownership. The inequity that remains in housing can be a point of pain and frustration. That’s why it’s so important for members of diverse groups to have the right team of experts on their sides throughout the homebuying process.

These professionals aren’t only experienced advisors who understand the market and give the best advice. They’re also compassionate allies who will advocate for your best interests every step of the way. They can point you to important resources and tools that can help you throughout your journey to homeownership.

Bottom Line

Opportunities in real estate improve every day, but there are still equity challenges that many face. Let’s connect to make sure you have an advocate on your side to help you achieve your dream of homeownership.

More Listings Are Coming onto the Market [INFOGRAPHIC]

![More Listings Are Coming onto the Market [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/06/16132154/20220617-MEM-1046x2089.png)

Some Highlights

- Worried you won’t be able to find your next home after you sell? You should know data from realtor.com shows more listings are coming onto the market each month this year.

- Having additional options can make the search for your next home easier. But inventory is still low overall, which means your house should still stand out when you sell.

- If your biggest question is where you’ll go if you sell, take this as encouraging news. Let’s connect to start the process today.

The Top Reasons To Own Your Home [INFOGRAPHIC]

![The Top Reasons To Own Your Home [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/06/09112013/20220603-MEM-1-1046x2276.png)

Some Highlights

- June is National Homeownership Month, and it’s a great time to consider the benefits of owning your own home.

- If you’re considering homeownership, know that it can give you privacy, comfort, and a place to express yourself. It can also provide financial stability and help you grow your net worth.

- Are you ready to experience all the great benefits that come from purchasing a home? Let’s connect to begin the process today.

What Are the Best Options for Today’s First-Time Homebuyers?

If you’re looking to buy your first home, you’re likely balancing several factors. Because both mortgage rates and home prices have risen this year, it costs more to buy a home than it did even just a few months ago. But that doesn’t mean you have to put your plans on hold.

If you partner with a trusted real estate advisor and hone your strategy, you can navigate today’s market and find the home you’re looking for. Here are two tips to help you get started.

Work with a Professional To Prioritize Your Wish List

If you’re having trouble finding a home in your budget that checks all the boxes, it may be worth taking another look at your lists of what you want and what you really need. According to the latest First-Time Homebuyer Metro Affordability Report from NerdWallet, your wish list can have as much impact on your search as your finances:

“Your budget isn’t all that you need to be concerned about; your wish list and desired location may carry just as much weight.”

It’s all about prioritization. If you’re serious about purchasing your first home soon, be flexible in what you’re looking for to open up your pool of options. Partner with a local real estate professional to better understand what’s available in today’s market and reprioritize your wish list. Remember, making a concession now doesn’t mean you’ll never have everything on your list. After you’ve moved in, you can always add certain features to make the home your own.

Increase Your Search Radius To Consider More Locations

Some areas may have more homes within your target price range than others, but it may require you to be flexible on your location. For example, if you’re a remote worker, you may be able to expand your search radius. As Fannie Mae explains:

“. . . continued remote work flexibility is likely giving many the ability to live farther away in more affordable areas.”

The decision to search in places with a lower cost of living could help you find a home that fits your budget and checks the most boxes off your wish list.

Bottom Line

If you’re serious about purchasing your first home this year, revisiting your wish list and desired location can help. Let’s connect to explore all the options in our local market – and beyond – so you can achieve your homeownership dreams.

How Homeownership Impacts You

June is National Homeownership Month, and it’s the perfect time to reflect on how impactful owning a home can truly be. When you purchase a house, it becomes more than just a space you occupy. It’s your stake in the community, an investment, and a place you can put your stamp on.

If you’re thinking about buying a home this year, here are some of the benefits you’ll experience when you do.

The Emotional Benefits of Homeownership

Because it’s a place that’s uniquely yours, owning a home can give you a sense of pride and happiness in several ways.

Your Home Can Reflect Your Tastes and Personality

Investopedia puts it like this:

“One often-cited benefit of homeownership is the knowledge that you own your little corner of the world.”

That knowledge can lead to a powerful, emotional connection to the place where you live. But so can the realization that your home will grow with you. Because it’s yours, you have the freedom to make updates to it as your needs and tastes change. As Logan Mohtashami, Lead Analyst for HousingWire, says:

“The psychology is that this is yours and you’re going to make it as good as possible because you’re in for a long time, . . . “

And that can create a greater sense of ownership, pride, and connection with your home and your community.

It Can Enhance Your Neighborhood and Civic Engagement

Homeownership can lead you to get even more involved with your local area. After all, you’re putting your roots down in a location and will want to do what you can to help improve it, much like your home. In a recent report, the National Association of Realtors (NAR) says:

“Living in one place for a longer amount of time creates and [sic] obvious sense of community pride, which may lead to more investment in said community.”

The Financial Benefits of Homeownership

When you choose to become a homeowner, you’re making a financial decision as well. That’s because your home is also an investment.

It Can Help You Feel Financially Stable

Homeownership is truly one of the best ways to improve your long-term financial position. Not only will you have a predictable monthly housing expense that can benefit your budget in the short term, but you’ll also gain equity as your home appreciates in value and you make your monthly mortgage payment. As Freddie Mac says:

“Building equity through your monthly principal payments and appreciation is a critical part of homeownership that can help you create financial stability.”

It Can Grow Your Wealth

Because of your growing equity, you can build your net worth as a homeowner. And when you compare the difference in net worth between a renter and a homeowner, it’s clear that owning a home truly offers a great way to build your long-term financial position.

According to the latest data from NAR, the median household net worth of a homeowner is roughly $300,000, while the median net worth of renters is only about $8,000. That means a homeowner’s net worth is nearly 40 times that of a renter.

Bottom Line

Homeownership is truly a way to find greater satisfaction and happiness and to build financial freedom. If National Homeownership Month has you dreaming about purchasing a home, then let’s connect to begin the process today.

Why Home Loans Today Aren’t What They Were in the Past

In today’s housing market, many are beginning to wonder if we’re returning to the riskier lending habits and borrowing options that led to the housing crash 15 years ago. Let’s ease those concerns.

Several times a year, the Mortgage Bankers Association (MBA) releases an index titled the Mortgage Credit Availability Index (MCAI). According to their website:

“The MCAI provides the only standardized quantitative index that is solely focused on mortgage credit. The MCAI is . . . a summary measure which indicates the availability of mortgage credit at a point in time.”

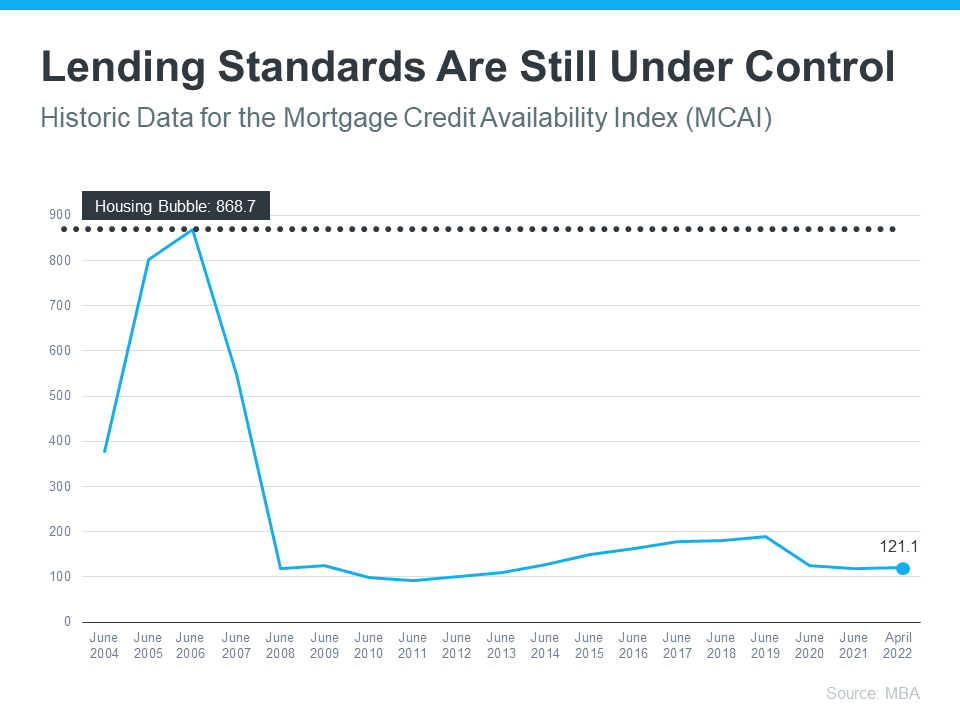

Basically, the index determines how easy it is to get a mortgage. The higher the index, the more available mortgage credit becomes. Here’s a graph of the MCAI dating back to 2004, when the data first became available:

As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006.

As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006.

Why Did the Index Get out of Control During the Housing Bubble?

The main reason was the availability of loans with extremely weak lending standards. To keep up with demand in 2006, many mortgage lenders offered loans that put little emphasis on the eligibility of the borrower. Lenders were approving loans without always going through a verification process to confirm if the borrower would likely be able to repay the loan.

An example of the relaxed lending standards leading up to the housing crash is the FICO® credit score associated with a loan. What’s a FICO® score? The website myFICO explains:

“A credit score tells lenders about your creditworthiness (how likely you are to pay back a loan based on your credit history). It is calculated using the information in your credit reports. FICO® Scores are the standard for credit scores—used by 90% of top lenders.”

During the housing boom, many mortgages were written for borrowers with a FICO score under 620. While there are still some loan programs that allow for a 620 score, today’s lending standards are much tighter. Lending institutions overall are much more attentive about measuring risk when approving loans. According to the latest Household Debt and Credit Report from the New York Federal Reserve, the median credit score on all mortgage loans originated in the first quarter of 2022 was 776.

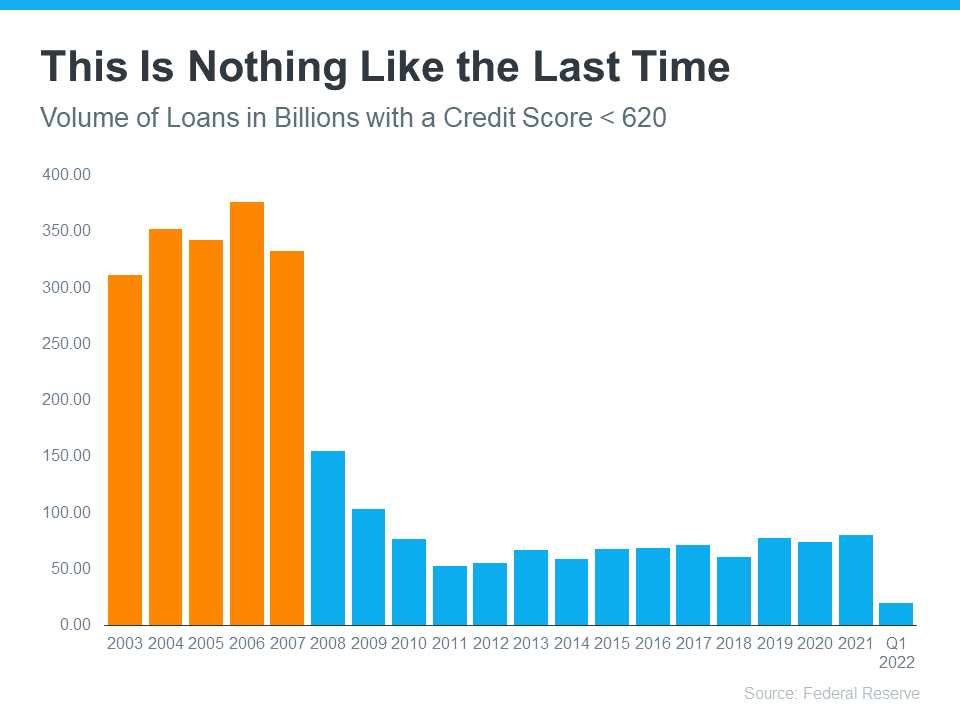

The graph below shows the billions of dollars in mortgage money given annually to borrowers with a credit score under 620.

In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

Bottom Line

In 2006, lending standards were much more relaxed with little evaluation done to measure a borrower’s potential to repay their loan. Today, standards are tighter, and the risk is reduced for both lenders and borrowers. These are two very different housing markets, and today is nothing like the last time.