[et_pb_section fb_built=”1″ _builder_version=”3.0.47″][et_pb_row _builder_version=”3.0.48″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”][et_pb_column type=”4_4″ _builder_version=”3.0.47″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.18.2″ background_size=”initial” background_position=”top_left” background_repeat=”repeat”]

There are so many great reasons to purchase a home, and over the past year, we’ve realized more of them than we ever thought possible. If you’re a first-time homebuyer, having a home of your own can give you a greater sense of security and accomplishment in a time that’s largely uncertain. If you’re a repeat buyer looking for your dream home, making a move might give you the space or features you need to find greater success and happiness in a new normal way of life. Whatever your motivations are, here are three reasons why becoming a homeowner now may help you win big in the long run.

1. Buying a Home Is a Great Investment

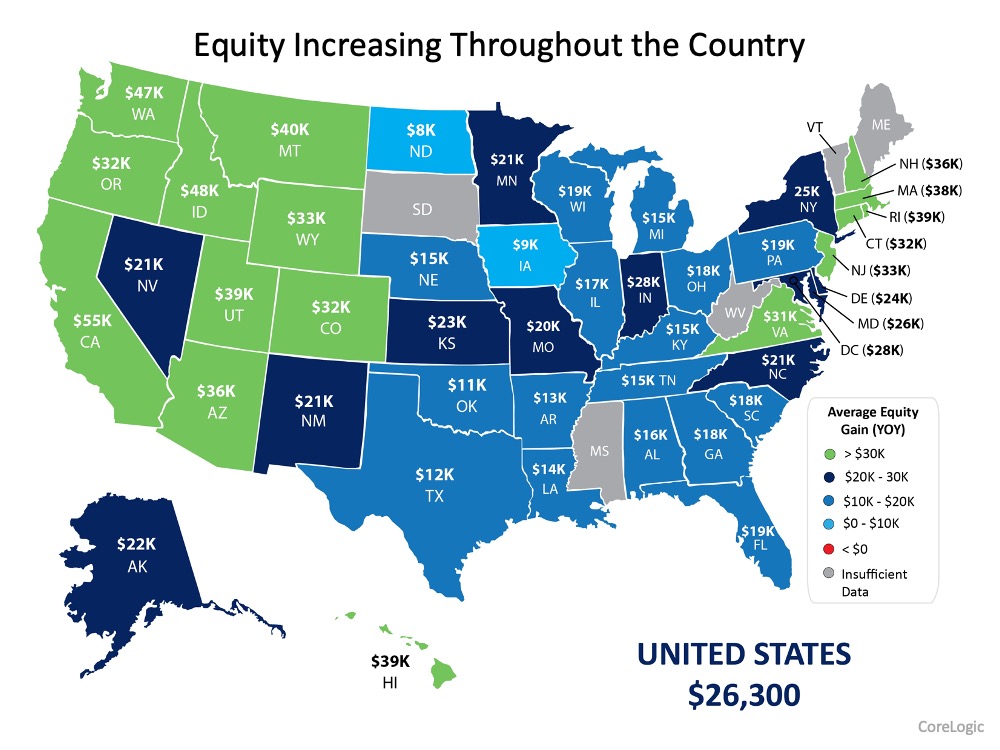

Several recent reports indicate that real estate is still a good investment, topping other options such as gold, stocks, bonds, and savings. Why? Real estate helps you build equity, a type of forced savings that grows your net worth. According to the latest Equity Report from ATTOM Data Solutions:

“The count of equity-rich properties in the fourth quarter of 2020 represented 30.2 percent, or about one in three, of the 59 million mortgaged homes in the United States. That was up from 28.3 percent in the third quarter of 2020, 27.5 percent in the second quarter and 26.7 percent in the fourth quarter of 2019, despite the ongoing economic damage caused by the worldwide Coronavirus pandemic.”

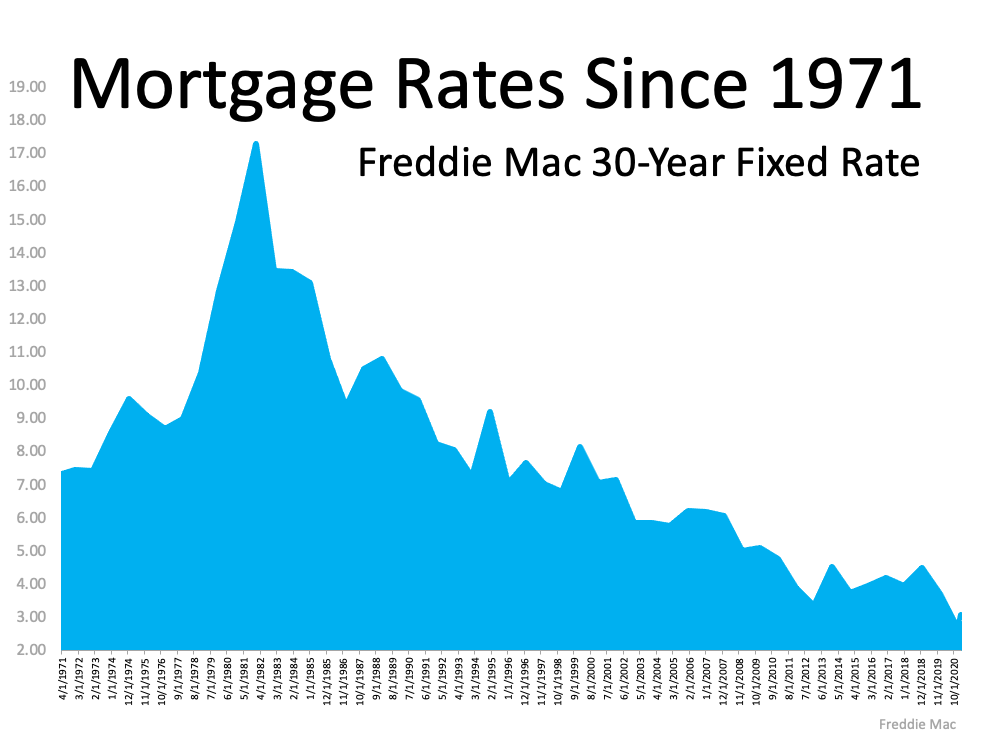

2. Mortgage Interest Rates Are Low

The Primary Mortgage Market Survey from Freddie Mac indicates interest rates for a 30-year mortgage have fallen since November 2018 when they hit 4.94%. In their latest forecast, Freddie Mac expects rates to remain low, leveling out to an average of 2.9% in 2021.

When you purchase a home at a low mortgage rate, it will impact your monthly mortgage payment, giving you the opportunity to likely get more house for your money.

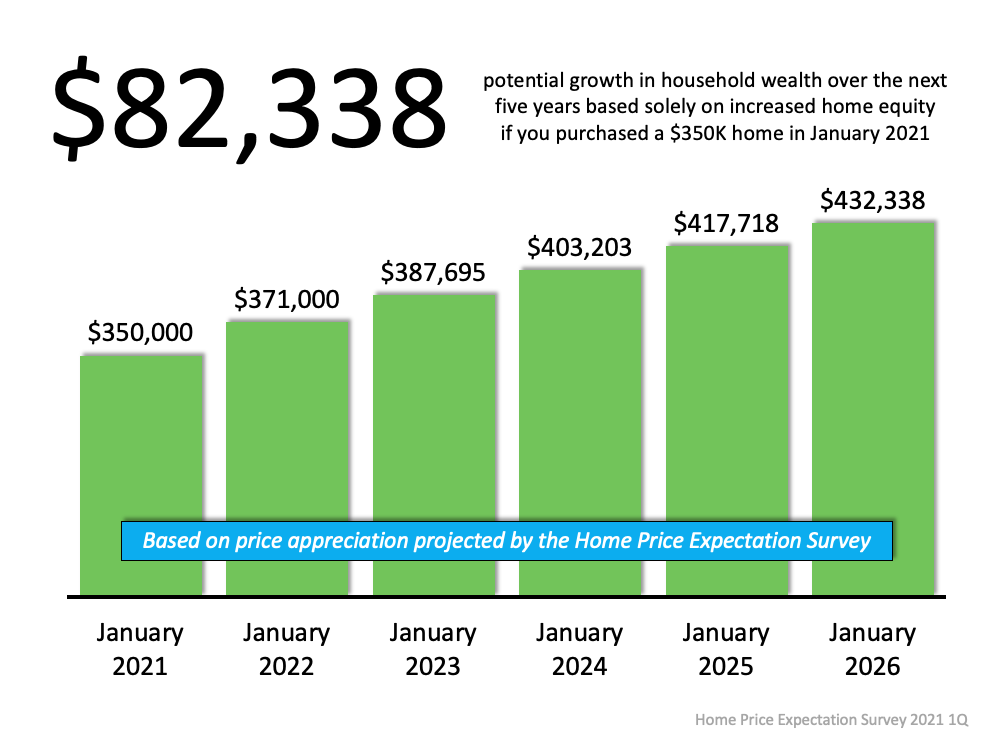

3. Investing in Your Future Pays Off

There are some renters who haven’t purchased a home yet because they’re uncomfortable taking on the obligation of a mortgage. What many renters don’t realize, though, is the financial power of equity.

As a homeowner, your monthly mortgage payment becomes a form of ‘forced savings’ you can reinvest later in life as you see fit. You can use it in a variety of ways, like to fund a loved one’s education, move up to a bigger home, or start your own business. As a renter, you’re actually growing your landlord’s equity instead of your own.

If you’re ready to put your monthly payments to work for you and take steps toward those dreams and goals, purchasing a home may be the way to go, especially as rental prices continue to rise.

Bottom Line

Buying a home sooner rather than later could lead to substantial savings and long-term financial growth. Let’s connect to determine if homeownership is the right choice for you this year. Find your home with ease using our personalized home match tool.

Contact one of Our Agents today!

See out Complete Inventory of Available Properties!

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section fb_built=”1″ _builder_version=”3.18.2″][et_pb_row _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_blog fullwidth=”off” posts_number=”3″ include_categories=”34″ show_author=”off” show_date=”off” show_categories=”off” _builder_version=”3.18.2″ header_level=”h5″ header_font=”||||||||” body_font=”||||||||” border_radii=”on|12px|12px|12px|12px” text_orientation=”center”][/et_pb_blog][/et_pb_column][/et_pb_row][/et_pb_section]

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

![The Power of Mortgage Pre-Approval [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/05/06093925/20210507-MEM-1046x1559.png)

![How to Be a Competitive Buyer in Today’s Housing Market [INFOGRAPHIC]](https://greenteamrealty.com/files/2021/04/How-to-Be-a-Competitive-Buyer-in-Todays-Housing-Market-INFOGRAPHIC.png)

![How to Be a Competitive Buyer in Today’s Housing Market [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/03/10135710/20210312-MEM-1046x2024.png)