If you’re thinking of buying a home, you’re probably wondering what you need to save for your down payment. Is it 20% of the purchase price, or could you put down less? While there are lower down payment programs available that allow qualified buyers to put down as little as 3.5%, it’s important to understand the many perks that come with a 20% down payment.

Here are four reasons why putting 20% down may be a great option if it works within your budget.

1. Your Interest Rate May Be Lower

A 20% down payment vs. a 3-5% down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage interest rate they’ll likely be willing to give you.

2. You’ll End Up Paying Less for Your Home

The larger your down payment, the smaller your loan amount will be for your mortgage. If you’re able to pay 20% of the cost of your new home at the start of the transaction, you’ll only pay interest on the remaining 80%. If you put down 5%, the additional 15% will be added to your loan and will accrue interest over time. This will end up costing you more over the lifetime of your home loan.

3. Your Offer Will Stand Out in a Competitive Market

In a market where many buyers are competing for the same home, sellers often like to see offers come in with 20% or larger down payments. The seller gains the same confidence as the lender in this scenario. You are seen as a stronger buyer with financing that’s more likely to be approved. Therefore, the deal will be more likely to go through.

4. You Won’t Have To Pay Private Mortgage Insurance (PMI)

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage.

It is not the same thing as homeowner’s insurance. It’s a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%. . . . Once you’ve built equity of 20% in your home, you can cancel your PMI and remove that expense from your monthly payment.”

As mentioned earlier, if you put down less than 20% when buying a home, your lender will see your loan as having more risk. PMI helps them recover their investment in you if you’re unable to pay your loan. This insurance isn’t required if you’re able to put down 20% or more.

Many times, home sellers looking to move up to a larger or more expensive home are able to take the equity they earn from the sale of their house to put 20% down on their next home. With the equity homeowners have today, it creates a great opportunity to put those savings toward a larger down payment on a new home.

Bottom Line

If you’re looking to buy a home, consider the benefits of 20% down versus a smaller down payment option. Let’s connect so you have expert advice to help make your homeownership goals a reality.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams. What’s your home’s value?

To succeed as a buyer in today’s market, it’s important to understand which market trends will have the greatest impact on your home search. Danielle Hale, Chief Economist at realtor.com, says there are two factors every buyer should keep their eyes on:

“Going forward, the conditions buyers face are primarily dependent on two things: mortgage rates and housing supply.”

Here’s a look at each one.

Mortgage Rates Projected To Rise in 2022

As a buyer, your interest rate directly impacts how much you’ll pay on your monthly mortgage when you purchase a home. Rates are beginning to rise, and experts forecast they’ll continue going up in 2022 (see graph below):As the graph shows, mortgage rates are expected to climb next year. But they’re still low when you compare to where they were just a few years ago. That presents today’s buyers with some motivation to lock in a low mortgage rate before they climb higher.

More Homes Are Expected To Be Available This Season

The other market condition buyers need to monitor is the number of homes available for sale today. The latest Existing Home Sales Report from the National Association of Realtors (NAR) shows the current supply of inventory sits at just 2.4-months. To put that into perspective, a 6-month supply is ideal for a balanced market where there are enough homes to meet buyer demand.

However, there may be good news for buyers who are waiting for more options. A recent realtor.comsurvey shows more sellers are planning to list their homes this winter, meaning more choices will likely be available soon.

What Does That Mean for You?

Even if your options improve some this season, it won’t significantly shift market conditions overnight. According to NAR, many more listings need to be available to move closer to a more neutral market:

“Given the average monthly demand . . . , 3.55 million homes should be on the market to meet a level of inventory equal to six months of demand, implying a shortage of homes for sale of 2.24 million.”

So remember, even with more homes expected to come to market this season, competition among buyers will remain fierce as there still won’t be enough homes for sale to meet the current demand. That means you’ll need to act quickly when you’re ready to make an offer.

Bottom Line

If you’re planning on buying a home this winter, more options are welcome news, but it doesn’t mean you should slow down. Let’s connect today so you have an expert on your side to help act as quickly as possible when the right home for you hits the market.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams. What’s your home’s value?

Black Friday and Cyber Monday are over, which means some shoppers have wrapped up their holiday buying. But there’s still a group of buyers that are very active this holiday season – homebuyers.

Experts anticipate the real estate market will see a flurry of activity this winter, and that’s great news for today’s sellers. If you’re planning on listing your home, there’s no need to wait until the spring for better conditions – today’s real estate market is already heating up.

Buyers Have Warmed Up to the Idea of Purchasing This Winter

The past 18 months brought about significant lifestyle changes for many of us, including the rise in remote work, job changes, and even early retirement for some. For many people, it’s prompting a search for their next home now rather than waiting for warmer months.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), points out how this winter may see a significant number of sales:

“Compared to other past winter seasons, this winter season’s sales activity will be stronger. . . . This winter, there will be more sales compared to pre-pandemic winters going back all the way to 2006.”

You might be wondering: what does strong sales activity mean for you? It means there are likely to be more buyers active in the market this winter – far more than more normal, pre-pandemic years.

In the same article, Danielle Hale, Chief Economist for realtor.com, puts it in these simple terms:

“Sellers can expect to see plenty of buyers.”

The more buyers there are in the market, the more likely it is your home will get noticed. That can lead to a multiple-offer scenario or a potential bidding war. Receiving multiple offers on your home means you can select the right offer and terms for your situation – so you can truly win as a seller when you list your house this winter.

Bottom Line

If you’re thinking about selling your house, you don’t need to wait until the spring. Buyers are ready now. Let’s connect to discuss why selling this holiday season could be the gift that keeps on giving.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams. What’s your home’s value?

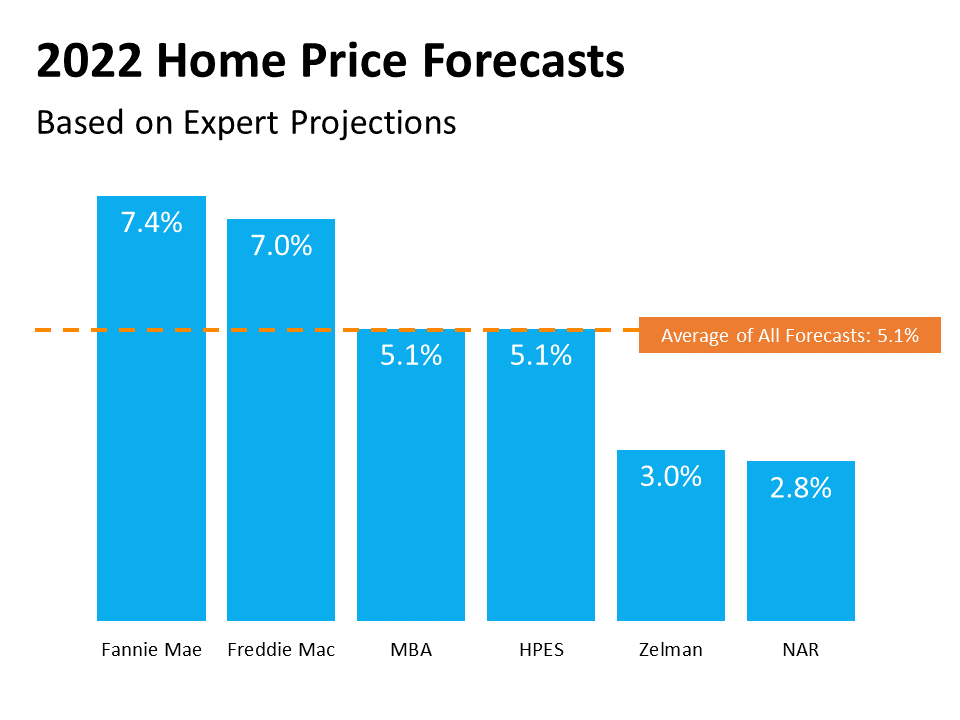

If you’re thinking of buying a home in today’s housing market, you may be wondering how strong your investment will be. You might be asking yourself: if I buy a home now, will it lose value? Or will it continue to appreciate going forward? The good news is, according to the experts, home prices are not projected to decline. Here’s why.

With buyers still outweighing sellers, home prices are forecast to continue climbing in 2022, just at a slower or more moderate pace. Why the continued increase? It’s the simple law of supply and demand. When there are fewer items on the market than there are buyers, the competition for that item makes prices naturally rise.

And while the number of homes for sale today is expected to improve with more sellers getting ready to list their houses this winter, we’re certainly not out of the inventory woods yet. Thus, the projections show continued appreciation, but at a more moderate rate than what we’ve seen over the past year.

Here’s a look at the latest 2022 expert forecasts on home price appreciation:What’s the biggest takeaway from this graph? None of the major experts are projecting depreciation in 2022. They’re all showing an increase in home prices next year.

And here’s what some of the industry’s experts say about how that will play out in the housing market next year:

“. . . the recent unsustainable rate of home price appreciation will slow sharply. . . . home prices will not decline. . . but they will simply rise at a more sustainable pace.”

“Price growth is expected to move back toward a normal range, but this is on top of recent high prices, . . . So prices will [still] hit new highs. . . . The pace of price growth is going to slow notably . . . ”

What Does This Mean for the Housing Market?

While home price appreciation is expected to continue, it isn’t projected to be the record-breaking 18 to almost 20% increase the market saw over the past 12 months. Overall, it’s important to note that price increases won’t be as monumental as they were in 2021 – but they certainly won’t decline anytime soon.

What Does That Mean for You?

With motivated buyers in the market and so few homes available to purchase, the imbalance of supply and demand will continue to put upward pressure on home prices in 2022. And when home price appreciation is in the forecast, that’s a clear indication your investment in homeownership is a sound one.

Bottom Line

It’s important to know that home prices are not projected to decline in the new year. Instead, they’re forecast to rise, just at a more moderate pace. Let’s connect to make sure you’re up to date on what’s happening with home price appreciation in our market, so you can make an informed decision about your next move.

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams. What’s your home’s value?

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

The sense of pride you’ll feel when you purchase a home can’t be overstated. For first-generation homebuyers, that feeling of accomplishment is even greater. That’s because the pride of homeownership for first-generation buyers extends far beyond the homebuyer. AJ Barkley, Head of Neighborhood and Community Lending for Bank of America, says:

“Achieving this goal can create a sense of pride and accomplishment that resonates both for the buyer and those closest to them, including their parents and future generations.”

In other words, your dream of homeownership has far-reaching impacts. If you’re about to be the first person in your family to buy a home, let that motivate you throughout the process. As you begin your journey, here are three helpful tips to make that dream come true.

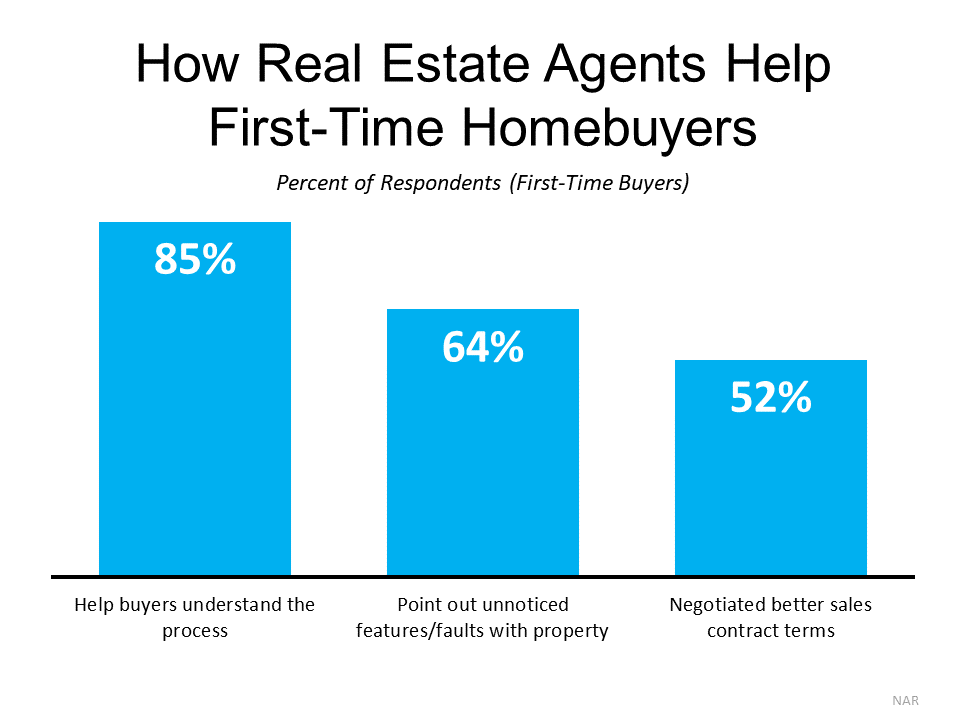

1. Reach Out to a Real Estate Professional

It’s important to reach out to a trusted advisor early in your homebuying process. Not only can an agent help you find the right home, but they’ll serve as your expert advisor and answer any questions you might have along the way.

The latest Profile of Home Buyers and Sellers from the National Association of Realtors (NAR) surveyed first-time homebuyers to see how their agent helped them with their home purchase (see chart below):

As the graph shows, your agent is a great source of information throughout the process. They’ll help you understand what’s happening, assess a home’s condition, and negotiate a contract that has the best possible terms for you. These are just some of the reasons having an expert in your corner is critical as you navigate one of the most significant purchases of your life.

2. Do Your Research and Know What You Can Afford

The second piece of advice for first-generation homebuyers is practical: do your research so you know what you can afford. That means getting your finances in order, reviewing your budget, and getting pre-approved through a lender. It also means learning the ins and outs of what it takes to pay for your home, including what you’ll need for a down payment.

Many homebuyers believe the common misconception that you can’t purchase a home without coming up with a 20% for a down payment. As Freddie Macsays:

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

The chart below shows what recent homebuyers have actually put down on their purchases:

On average, first-time buyers only put 7% down on their home purchase. That’s far less than the 20% many people believe is necessary. That means your down payment, and your home purchase, may be in closer reach than you realize. Keep that in mind as you work with a real estate professional to better understand what you’ll need for your purchase.

3. Don’t Lose Sight of What Home Means to You

Finally, it’s important keep in mind why you’re searching for a home to begin with. Overwhelmingly, first-generation homeowners recognize the financial and non-financial benefits of owning a home. In fact, in a recent survey:

73% of first-generation homeowners say the safety and security homeownership provides is increasing in importance.

Nearly two-thirds of first-generation homeowners say the importance of building equity in a home is growing more important as well.

As AJ Barkley explains:

“For many first-generation homeowners and their families, homeownership has a unique importance, given the collective efforts to overcome financial challenges that can often span generations…”

Bottom Line

If you’re a first-generation homebuyer, being prepared and working with a trusted expert is key to achieving your dream. Let’s connect today so you can get started on your path to homeownership.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

It’s no secret that we love our furry friends – about 70% of U.S. households have pets. What may come as a surprise is how large a role they play in the homebuying process.

Americans spend $1,163 a year on their pets, and nearly half of pet owners say they would move for better accommodations and amenities for their pets.

If you’re thinking of adding a furry friend, or if you already have, let’s connect to discuss how you can find a home that meets all your pet’s needs

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams. What’s your home’s value?

If you’re a homeowner who’s decided your current house no longer fits your needs, or a renter with a strong desire to become a homeowner, you may be hoping that waiting until next year could mean better market conditions to purchase a home.

To determine whether you should buy now or wait another year, you can ask yourself two simple questions:

Where will home prices be a year from now?

Where will mortgage rates be a year from now?

Let’s shed some light on the answers to both of these questions.

Where Will Home Prices Be a Year from Now?

Three major housing industry entities are projecting ongoing home price appreciation in 2022. Here are their forecasts:

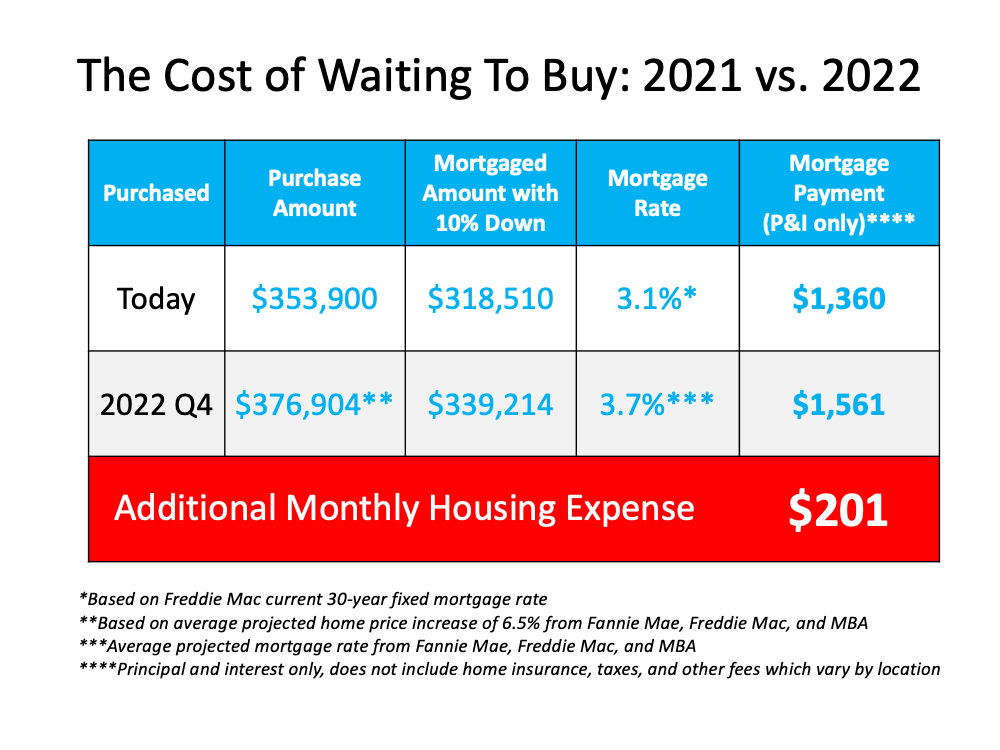

According to the National Association of Realtors (NAR), the median price of a home today is $353,900. Using an average of the three price projections above (6.5%), a home that sold for $353,900 today would be valued at $376,904 at the end of next year. As a prospective buyer, you would therefore pay an additional $23,004 by waiting.

Where Will Mortgage Rates Be a Year from Now?

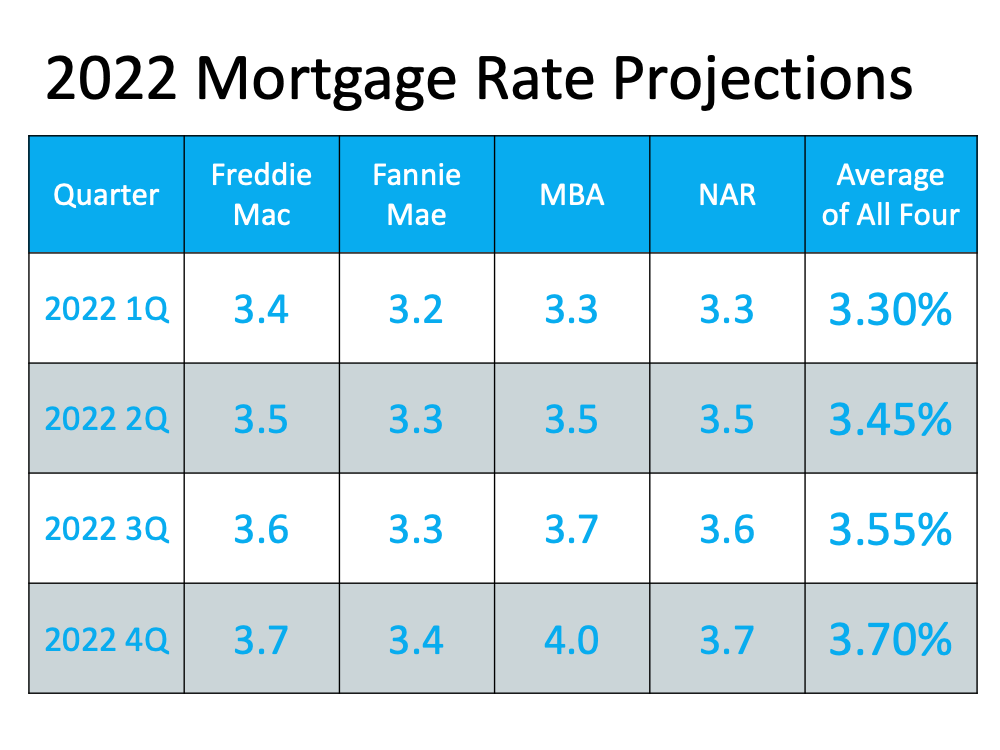

Today, Freddie Macannounced their 30-year fixed mortgage rate was at 3.1%. However, most experts believe mortgage rates will rise as the economy recovers. Here are the forecasts for the fourth quarter of 2022 by the three major entities mentioned above:

That averages out to 3.7% if you include all three forecasts. Any increase in mortgage rates will increase your costs.

What Does It Mean for You if Home Values and Mortgage Rates Increase?

If both variables increase, you’ll pay a lot more in mortgage payments each month. Let’s assume you purchase a $353,900 home today with a 30-year fixed-rate loan at 3.1% (the current rate from Freddie Mac) after making a 10% down payment. According to mortgagecalculator.net, your monthly mortgage payment would be approximately $1,360 (this does not include insurance, taxes, and other fees because those vary by location).

That same home one year from now could cost $376,904, and the mortgage rate could be 3.7% (based on the industry forecasts mentioned above). Your monthly mortgage payment after putting down 10%, would be approximately $1,561.The difference in your monthly mortgage payment would be $201. That’s $2,412 more per year and $72,360 over the life of the loan.

Add to that the approximately $23,004 a house with a similar value would build in home equity this year due to home price appreciation, and the total net worth increase you could gain by buying this year is over $95,364 (the $72,360 mortgage savings plus the $23,004 potential gain in equity if you buy now).

Bottom Line

When asking if you should buy a home, you may think of the non-financial benefits of homeownership. When asking when to buy, the financial benefits make it clear that doing so now is much more advantageous than waiting until next year.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams. What’s your home’s value?

Since the pandemic began, Americans have reevaluated the meaning of the word home. That’s led some renters to realize the many benefits of homeownership, including the feelings of security and stability and the financial benefits that come with rising home equity. At the same time, many current homeowners have decided their house no longer meets their needs, so they moved into homes with more space inside and out, including a home office for remote work.

However, not every purchaser has been able to fulfill their desire for a new home. Here are two obstacles some homebuyers are facing:

The ability to save for a down payment

The ability to qualify for a mortgage at the current lending standards

This past week, both of those challenges have been mitigated to some degree for many purchasers. The FHFA (which handles mortgages by Freddie Mac, Fannie Mae, and the Federal Housing Administration) is raising its loan limit for prospective purchasers in 2022. The term used to describe the maximum loan amount they will entertain is the Conforming Loan Limit.

What Is the Difference Between a Conforming Loan and a Non-Conforming Loan?

Investopedia explains the difference in a recent post:

“Conforming loans are the only loans that meet the requirements to be acquired by Fannie Mae and Freddie Mac. Jumbo loans, which exceed the conforming limit, are the most common type of nonconforming loan.”

What Difference Does It Make to Me as a Home Buyer?

A Forbesarticle earlier this year explains the benefits of a conforming loan and why they exist:

“Since lenders can’t sell non-conforming loans to Fannie Mae or Freddie Mac to free up their cash, they’re a bit riskier for the lender. This is especially true for jumbo loans, which aren’t backed by any government guarantees. If you default on a jumbo loan, it’s a huge blow to the lender.

Thus, lenders generally charge higher interest rates to compensate, and they can have even more requirements. For example, lenders who give out jumbo loans often require that you make a down payment of at least 20% and show that you have at least six months’ worth of cash in reserve, if not more.”

What Happened Last Week?

The FHFA has significantly increased its Conforming Loan Limits for 2022. Sandra L. Thompson, FHFA Acting Director, explains in the press release that:

“Compared to previous years, the 2022 Conforming Loan Limits represent a significant increase due to the historic house price appreciation over the last year. While 95 percent of U.S. counties will be subject to the new baseline limit of $647,200, approximately 100 counties will have conforming loan limits approaching $1 million.”

This means that more homes now qualify for a conforming loan with lower down payment requirements and easier lending standards – the two challenges holding many buyers back over the last year.

The Federal Housing Administration (FHA) also increased its Conforming Loan Limits for 2022. That could also mean an easier path to homeownership for many prospective buyers. As the Forbes article explains:

“FHA loans can be very beneficial if you don’t have as much savings, or if your credit score could use some work.”

Bottom Line

Buying your first or your next home may have just gotten much easier (less stringent qualifying standards) and less expensive (possibly lower mortgage rate). Let’s connect to discuss how these changes may impact you.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams. What’s your home’s value?

If you’re trying to decide when to sell your house, there may not be a better time than this winter. Selling this season means you can take advantage of today’s strong sellers’ market when you make a move.

Win When You Sell

Right now, conditions are very favorable for current homeowners looking for a change. If you sell now, here’s what you can expect:

Your House Will Stand Out – While recent data shows there are more sellers getting ready to list their homes this winter, there are still more buyers in the market than there are homes for sale. If you sell your house now before more houses are listed, it will get more attention from serious buyers who are eager to find a home.

Your House Will Likely Get Multiple Offers – When supply is low and demand is high, buyers have to compete with each other for a limited number of homes. The latest Realtors Confidence Index from the National Association of Realtors (NAR) shows sellers are getting an average of 3.6 offers in today’s market.

Your House Should Sell Quickly – According to the same report from NAR, homes are selling in an average of just 18 days. As a seller, that’s great news for you if you’re looking for a quick process.

Win When You Move

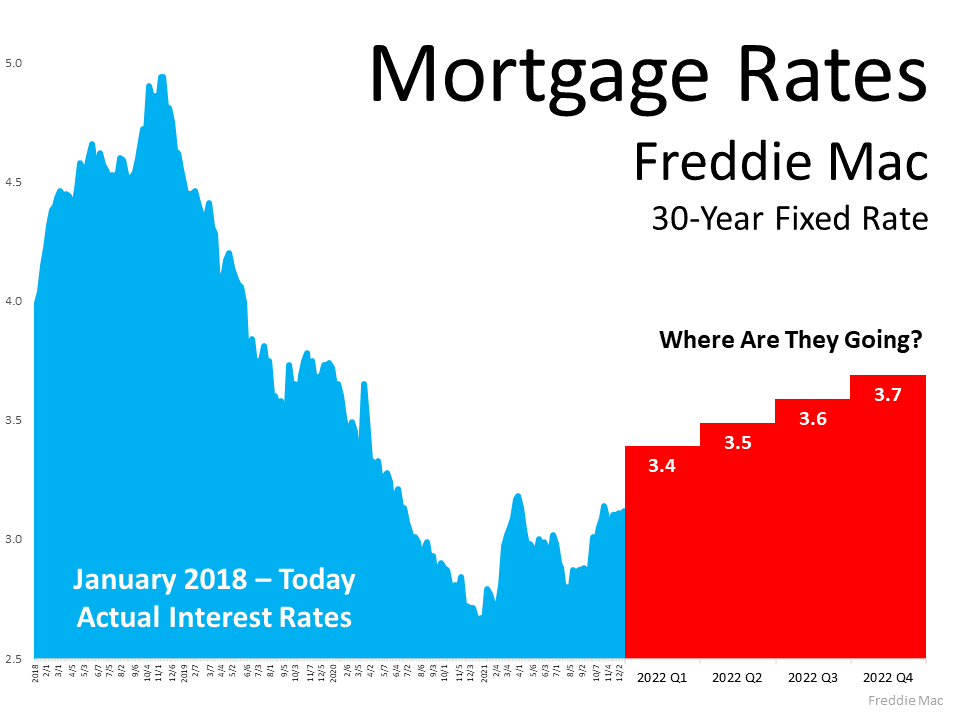

In addition to these great perks, you’ll also win big on your next move if you sell now. CoreLogicreports homeowners gained an average of $51,500 in equity over the past year. This wealth boost is the result of buyer competition driving home prices up. You can leverage that equity to fuel a move, before mortgage rates and home prices climb higher. To get a feel for how rates are projected to rise, see the chart below.The longer you wait to make your move, the more it will cost you down the road. As mortgage rates rise, even modestly, it will impact your monthly payment when you purchase your next home. Waiting just a few months to make that change could mean a long-term financial impact.

The good news is today’s rates are still hovering in a historically low range. According to Doug Duncan, Senior VP and Chief Economist at Fannie Mae:

“Right now, we forecast mortgage rates to average 3.3 percent in 2022, which, though slightly higher than 2020 and 2021, by historical standards remains extremely low . . .”

Selling before rates climb higher means you can make your move and lock in a low rate on the mortgage for your next home. This helps you get more home for your money and keeps your payments down too.

Bottom Line

As a homeowner, you have a great opportunity to get the best of both worlds this season. You can truly win when you sell and when you buy. If you’re thinking about making a move, let’s connect so you have the information you need to get the process started.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams. What’s your home’s value?

There’s no denying the financial benefits of homeownership, but what’s often overlooked are the feelings of gratitude, security, pride, and comfort we get from owning a home. This year, those emotions are stronger than ever. We’ve lived through a time that has truly changed our needs and who we are, and as a result, homeownership has a whole new meaning for many of us.

“Last year, staying home became a necessity and that caused many homeowners to have renewed gratitude for the roof over their head.”

As a nation, we continue to work through the challenges of a pandemic that’s pushed us all to new limits. Over the past year and a half, we’ve spent more time than ever at home: working, eating, schooling, exercising, and more. The world around us changed almost overnight, and our homes were redefined. Our needs shifted, and our shelters became a place that protected us on a whole new level. The same study from Unison notes:

91% of homeowners say they feel secure, stable, or successful owning a home

64% of American homeowners say living through a pandemic has made their home more important to them than ever

83% of homeowners say their home has kept them safe during the COVID-19 pandemic

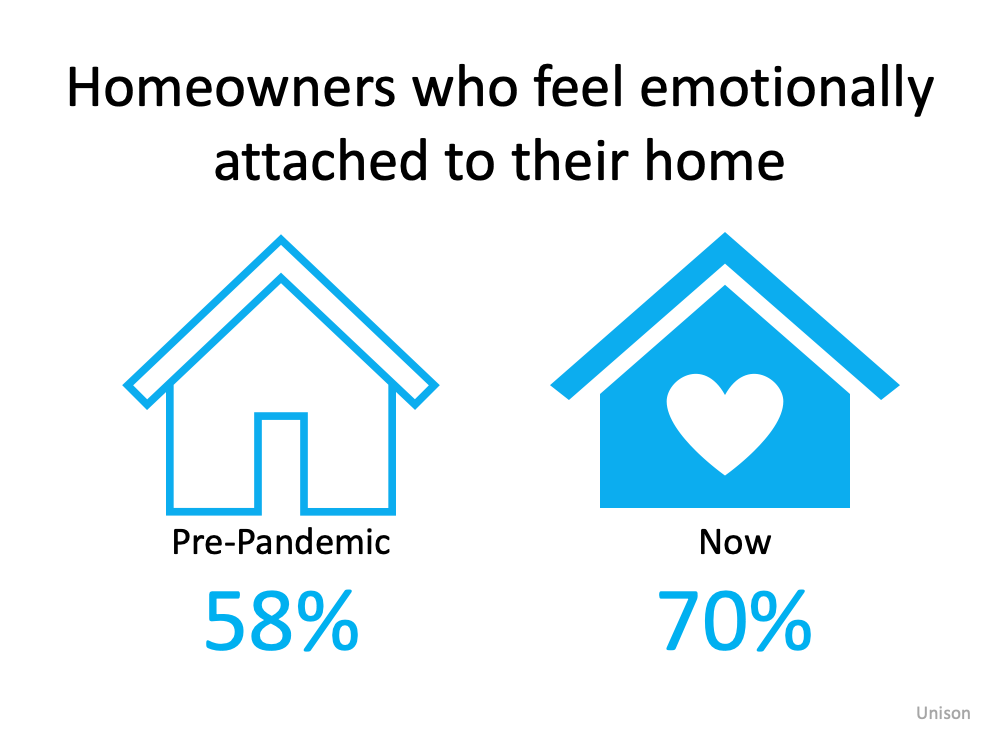

It’s no surprise this study also reveals that homeowners are now more emotionally attached to their homes as well:As we’ve learned throughout this health crisis, homeownership can provide the safety and security we crave in a time of uncertainty. That sense of connection and emotional stability genuinely reaches beyond just the financial aspect of owning a home. As JD Esajian, President of CT Homes, LLC, says:

“Aside from the financial factors, there are several social benefits of homeownership and stable housing to consider. It has long been thought that buying a home contributes to a sense of accomplishment. Still, most individuals fail to realize that homeownership can benefit your mental health and the community around you.”

Whether you’re thinking of buying your first home, moving up to your dream home, or downsizing to something that better fits your changing lifestyle, take a moment to reflect on what Mark Fleming, Chief Economist at First American,notes:

“Buying a home is not just a financial decision. It’s also a lifestyle decision.”

Bottom Line

If you’re considering buying a home, it’s not entirely about the dollars and cents. Don’t forget to weigh the non-financial benefits that may truly change your life when you need them most.

Put an experts eye on your home search! You’ll receive personalized matches of results delivered directly to you. We’ll take into account your goals, criteria, and preferences to find properties that are exactly what you were always dreaming of. Start Here!

Maybe with the leverage you currently have, you can negotiate a deal that will allow you to make the move of your dreams. What’s your home’s value?

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

![A Happy Tail Pets and the Homebuying Process [INFOGRAPHIC]](https://greenteamrealty.com/files/2021/12/A-Happy-Tail-Pets-and-the-Homebuying-Process-INFOGRAPHIC.png)

![A Happy Tail: Pets and the Homebuying Process [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/12/16123858/20211210-MEM-1-1046x1910.png)