Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What Is Multigenerational Housing? [INFOGRAPHIC]

![What Is Multigenerational Housing? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/04/14144240/20220415-MEM-1046x2456.png)

Some Highlights

- If you have additional loved ones coming to live with you but don’t have enough space, it may be time to consider a larger, multigenerational home.

- Some key benefits of multigenerational living include a combined homebuying budget, shared caregiving duties, enhanced relationships, and more. These benefits might be why more people are choosing to live in multigenerational homes today.

- Let’s connect so you can find a house that meets your changing needs and has plenty of space for you and your loved ones.

Where Are Mortgage Rates Headed?

There’s never been a truer statement regarding forecasting mortgage rates than the one offered last year by Mark Fleming, Chief Economist at First American:

“You know, the fallacy of economic forecasting is: Don’t ever try and forecast interest rates and or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

Coming into this year, most experts projected mortgage rates would gradually increase and end 2022 in the high three-percent range. It’s only April, and rates have already blown past those numbers. Freddie Mac announced last week that the 30-year fixed-rate mortgage is already at 4.72%.

Danielle Hale, Chief Economist at realtor.com, tweeted on March 31:

“Continuing on the recent trajectory, would have mortgage rates hitting 5% within a matter of weeks. . . .”

Just five days later, on April 5, the Mortgage News Daily quoted a rate of 5.02%.

No one knows how swiftly mortgage rates will rise moving forward. However, at least to this point, they haven’t significantly impacted purchaser demand. Ali Wolf, Chief Economist at Zonda, explains:

“Mortgage rates jumped much quicker and much higher than even the most aggressive forecasts called for at the end of last year, and yet housing demand appears to be holding steady.”

Through February, home prices, the number of showings, and the number of homes receiving multiple offers all saw a substantial increase. However, much of the spike in mortgage rates occurred in March. We will not know the true impact of the increase in mortgage rates until the March housing numbers become available in early May.

Rick Sharga, EVP of Market Intelligence at ATTOM Data, recently put rising rates into context:

“Historically low mortgage rates and higher wages helped offset rising home prices over the past few years, but as home prices continue to soar and interest rates approach five percent on a 30-year fixed rate loan, more consumers are going to struggle to find a property they can comfortably afford.”

While no one knows exactly where rates are headed, experts do think they’ll continue to rise in the months ahead. In the meantime, if you’re looking to buy a home, know that rising rates do have an impact. As rates rise, it’ll cost you more when you purchase a house. If you’re ready to buy, it may make sense to do so sooner rather than later.

Bottom Line

Mark Fleming got it right. Forecasting mortgage rates is an impossible task. However, it’s probably safe to assume the days of attaining a 3% mortgage rate are over. The question is whether that will soon be true for 4% rates as well.

Using Your Tax Refund To Achieve Your Homeownership Goals This Year

If you’re buying or selling a home this year, you’re likely saving up for a variety of expenses. For buyers, that might include things like your down payment and closing costs. And for sellers, you’re probably working on a bit of spring cleaning and maintenance to spruce up your house before you list it.

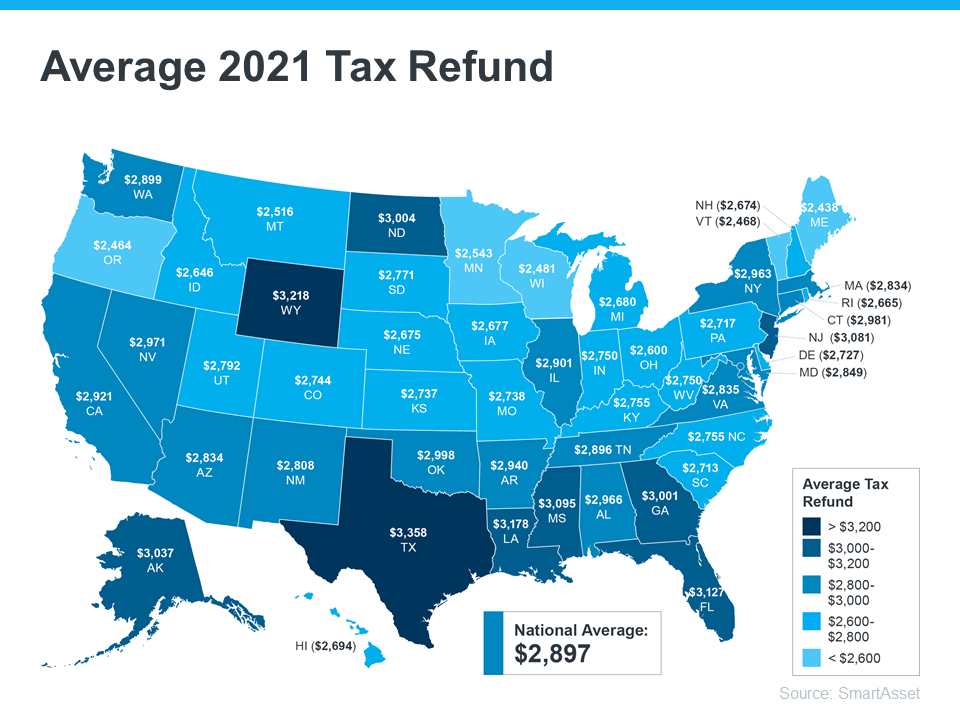

Either way, any money you get back from your taxes can help you achieve your goals. Using a tax refund is a common tactic for buyers and sellers. SmartAsset estimates the average American will receive a $2,897 tax refund this year. The map below provides a more detailed estimate by state:

If you’re getting a refund this year, here are a few tips to help with your home purchase or sale this season.

How Buyers Can Use Their Tax Refund

According to American Financing, there are multiple ways your refund check can help you as a homebuyer. A few include:

- Growing your down payment fund – If you haven’t started saving for your down payment, let your tax refund kick off the process. And if you have a fund already, the money you get back could put you closer to your goal.

- Paying for your home inspection – Your home inspection can save you a lot of headaches down the road by helping you determine the condition of the house. As a buyer, you’ll typically be responsible for paying for your inspection, and it’s definitely worth the investment.

- Saving for closing costs – Closing costs are additional expenses you’ll need to pay once it’s time to close. They average anywhere between 2-5% of the purchase price of your home.

This list is a great start, but it isn’t exhaustive of all the costs you may encounter as you set out on your homebuying journey. The best way to prepare is to work with a trusted real estate professional to make sure you understand what’s to come in the process.

How Sellers Can Use Their Tax Refund

If you own a home and are planning to sell this spring, your tax refund can help you make sure your home is ready to list. Here are a few ways current homeowners can put their tax refund to good use:

- Making small upgrades – NerdWallet provides a list of great ways to use your tax refund, including tackling small projects or boosting your curb appeal to help your home stand out.

- Making repairs – If there’s anything in your house that needs to be fixed, American Financing notes that completing repairs is another great use of that money.

- Buying your next home – Whether you’re selling to move up or downsize, you can use your tax refund to help pay for any costs on the purchase of your next home.

Of course, it’s important to talk with your trusted real estate advisor before taking on any projects. They’ll make sure you can focus on areas that’ll help you receive the best possible price when you sell.

Bottom Line

Funding your home purchase or sale can feel like a daunting task, but it doesn’t have to be. Your tax refund can help you reach your goals. Let’s connect to discuss how you can start on your journey.

Do You Know How Much Equity You Have in Your Home? [INFOGRAPHIC]

![Do You Know How Much Equity You Have in Your Home? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/04/05162315/20220408-MEM-1046x2334.png)

Some Highlights

- If you’re a homeowner, your net worth has gotten a big boost. That’s because recent home price appreciation has increased your equity.

- Your equity grows as you pay down your loan and as your home increases in value. Over the past year, the average homeowner’s equity grew by $55,300.

- Ready to sell? Let’s connect to talk about how you can use that equity to fuel your next move.

The Future of Home Price Appreciation and What It Means for You

Many consumers are wondering what will happen with home values over the next few years. Some are concerned that the recent run-up in home prices will lead to a situation similar to the housing crash 15 years ago.

However, experts say the market is totally different today. For example, Odeta Kushi, Deputy Chief Economist at First American, tweeted just last week on this issue:

“. . . We do need price appreciation to slow today (it’s not sustainable over the long run) but high price growth today is supported by fundamentals- short supply, lower rates & demographic demand. And we are in a much different & safer space: better credit quality, low DTI [Debt-To-Income] & tons of equity. Hence, a crash in prices is very unlikely.”

Price appreciation will slow from the double-digit levels the market has seen over the last two years. However, experts believe home values will not depreciate (where a home would lose value).

To this point, Pulsenomics just released the latest Home Price Expectation Survey – a survey of a national panel of over 100 economists, real estate experts, and investment and market strategists. It forecasts home prices will continue appreciating over the next five years. Below are the expected year-over-year rates of home price appreciation based on the average of all 100+ projections:

- 2022: 9%

- 2023: 4.74%

- 2024: 3.67%

- 2025: 3.41%

- 2026: 3.57%

Those responding to the survey believe home price appreciation will still be relatively high this year (though half of what it was last year), and then return to more normal levels over the next four years.

What Does This Mean for You as a Buyer?

With a limited supply of homes available for sale and both prices and mortgage rates increasing, it can be a challenging market to navigate as a buyer. But buying a home sooner rather than later does have its benefits. If you wait to buy, you’ll pay more in the future. However, if you buy now, you’ll actually be in the position to make future price increases work for you. Once you buy, those rising home prices will help you build your home’s value, and by extension, your own household wealth through home equity.

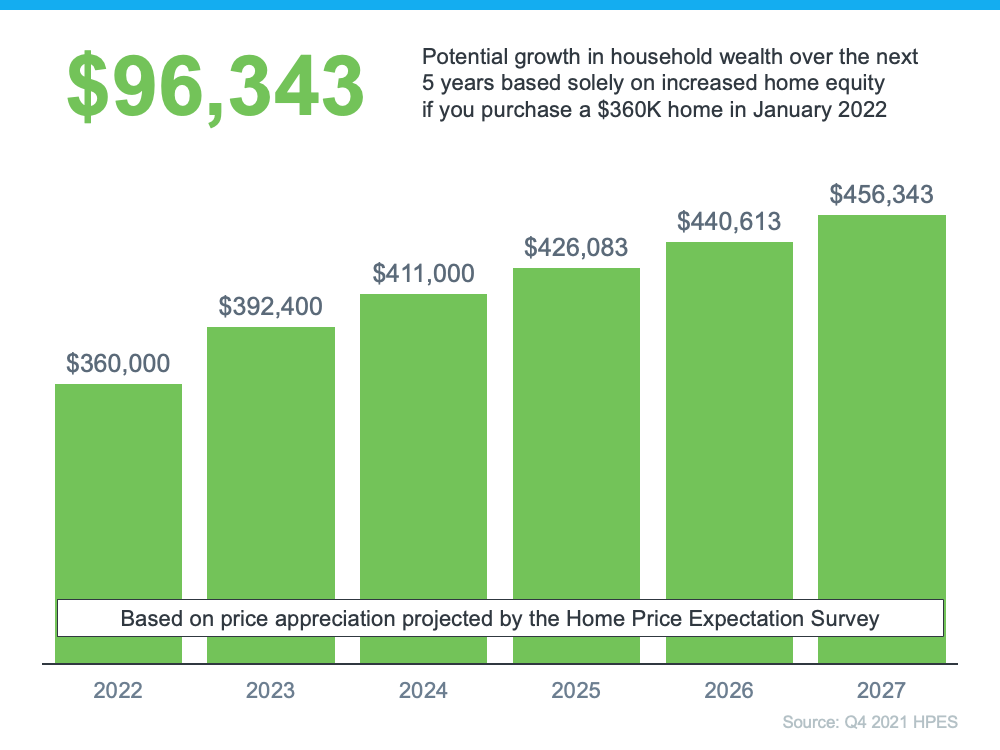

As an example, let’s assume you purchased a $360,000 home in January of this year (the median price according to the National Association of Realtors rounded up to the nearest $10K). If you factor in the forecast for appreciation from the Home Price Expectation Survey, you could accumulate over $96,000 in household wealth over the next five years (see graph below):

Bottom Line

If you’re trying to decide whether to buy now or wait, the key is knowing what’s expected to happen with home prices. Experts say prices will continue to climb in the years ahead, just at a slower pace. So, if you’re ready to buy, doing so now may be your best bet for your wallet. It’ll also give you the chance to use the future home price appreciation to build your own net worth through rising equity. If you want to get started, let’s connect today.

Remote Work Trends Mean Flexibility for First-Time Homebuyers

Today’s low inventory can be challenging for homebuyers, especially if you’re looking to purchase your first home. But if you’re one of many people who work remotely, you may have a great opportunity to use the flexibility you have at work to achieve your homebuying goals this year.

In a recent report, Arch Capital Services explains how the ongoing trend of remote work can open up more options for homebuyers:

“. . . This will enable those who are able to work from home on a part-time or hybrid basis to move slightly farther away from job centers. . . . For workers who secure full-time remote jobs, their place of residence will be determined by affordability and personal preferences.”

Basically, working from home is great news if you’re a first-time buyer trying to find a home that meets your needs and budget. Here’s a deeper look at how it could benefit you.

Extra Flexibility in Your Career Means Extra Flexibility in Your Home Search

If your job is 100% remote, you don’t have to be tied to a specific location or office. So, if you’ve been having a hard time finding what you want in your local area, it may be time to expand your search.

One option you could consider is moving to a place where you’ve always wanted to live, like the mountains, beach, or closer to loved ones. When you broaden your search radius to include those locations, it’ll give you additional homes to consider.

It could also allow you to search for a more affordable location where you have more options in your price range. This can help you achieve two goals – saving money and finding additional features that meet your needs. To truly highlight this benefit, a recent First American article discusses the great ways remote work can really help you with your homebuying goals. Ksenia Potapov, Economist at First American, says:

“For potential first-time home buyers, leveraging their house-buying power in more affordable markets can also help them buy more attractive homes – more square footage and rooms, more options for different home styles and neighborhood amenities – increasing the opportunity to find a home that suits their preferences.”

That means you can use your work flexibility to search for homes with the amenities you need at a lower price point.

Bottom Line

Remote work doesn’t just give you expanded flexibility for your career. If you’re no longer tied to a location because of your office, you have a great opportunity to expand your housing search. Let’s connect to explore how this can open up your options.

What You Need To Budget for When Buying a Home

When it comes to buying a home, it can feel a bit intimidating to know how much you need to save and where to find that information. But you should know, you’re not expected to have all the answers yourself. There are many trusted professionals who can help you understand your finances and what you’ll need to budget for throughout the process.

To get you started, here are a few things experts say you should plan for along the way.

1. Down Payment

As you set your savings goal for your purchase, your down payment is likely already top of mind. And, like many other people, you may believe you need to set aside 20% of the home’s purchase price for that down payment – but that’s not always the case. The National Association of Realtors (NAR) says:

“One of the biggest misconceptions among housing consumers is what the typical down payment is and what amount is needed to enter homeownership. Having this knowledge is critical to know what to save . . .”

The good news is, you may be able to put as little as 3.5% (or even 0%) down in some situations. To understand your options, partner with a trusted professional who can go over the various loan types, down payment assistance programs, and what each one requires.

2. Earnest Money Deposit

Another item you may want to plan for is an earnest money deposit. While it isn’t required, it’s common in today’s highly competitive market because it can help your offer stand out in a bidding war.

So, what is it? It’s money you pay as a show of good faith when you make an offer on a house. This deposit works like a credit. You’re using some of the money you already saved for your purchase to show the seller you’re committed and serious about their house. It’s not an added expense, it’s just paying some of that up front. First American explains what it is and how it works:

“The deposit made from the buyer to the seller when submitting an offer. This deposit is typically held in trust by a third party and is intended to show the seller you are serious about purchasing their home. Upon closing the money will generally be applied to your down payment or closing costs.”

In other words, an earnest money deposit could be the very first check you’ll write toward your purchase. The amount varies by state and situation. Realtor.com elaborates:

“The amount you’ll deposit as earnest money will depend on factors such as policies and limitations in your state, the current market, what your real estate agent recommends, and what the seller requires. On average, however, you can expect to hand over 1% to 2% of the total home purchase price.”

Work with a real estate advisor to understand any requirements in your local area and what they’ve recommended for other buyers in your market. They’ll help you determine if it’s something that could be a useful option for you.

3. Closing Costs

The next thing to plan for is your closing costs. The Federal Trade Commission (FTC) defines closing costs as:

“The upfront fees charged in connection with a mortgage loan transaction. …generally including, but not limited to a loan origination fee, title examination and insurance, survey, attorney’s fee, and prepaid items, such as escrow deposits for taxes and insurance.”

Basically, your closing costs cover the fees for various people and services involved in your transaction. NAR has this to say about how much to budget for:

“A home costs more than just the sale price. For example, closing costs—which make up about 2% to 5% of the home’s purchase price—are a major added expense…Lenders provide a Closing Disclosure at least three business days prior to closing on a mortgage. But buyers will need to budget for these added costs ahead of time to avoid sticker shock days before closing.”

The key takeaway is savvy buyers plan ahead for these expenses so they can come into the process prepared. Freddie Mac sums it up like this:

“If you’re in the market to buy a home, your down payment is probably top of mind. And rightly so – it’s likely the biggest cost of homebuying. However, it is not the only cost and it’s critical you understand all your expenses before diving in. The more prepared you are for your down payment, closing and other costs, the smoother your homebuying journey will be.”

Bottom Line

Knowing what to budget for in the homebuying process is essential. To make sure you understand these and any other expenses that may come up, let’s connect so you have reliable expertise on what to expect when you buy a home.

Balancing Your Wants and Needs as a Homebuyer Today

Since the number of homes for sale is low today, it can feel challenging to find one that checks all your boxes. But if you know which features are absolutely essential in your next home and which ones are just nice bonuses, you can land a home that fits your needs.

Danielle Hale, Chief Economist for realtor.com, explains it like this:

“Focus on the goal you set out for yourself, like your list of must-haves and nice-to-haves and your budget, . . . Stick to that. Be persistent.”

So how do you go about creating your list of desired features? The first step is to get pre-approved for your mortgage. Pre-approval helps you better understand your budget, and that plays an important role in how you’ll craft your list. After all, you don’t want to fall in love with a home that’s too far out of reach.

Once you have a good grasp of your budget, you can begin to list all the features of a home you would like. Here’s a great way to think about them before you begin:

- Must-Haves – If a house doesn’t have these features, it won’t work for you and your lifestyle (examples: distance from work or loved ones, number of bedrooms/bathrooms, etc.).

- Nice-To-Haves – These are features that you’d love to have but can live without. Nice-To-Haves aren’t dealbreakers, but if you find a home that hits all the must-haves and some of the these, it’s a contender (examples: a second home office, garage, etc.).

- Dream State– This is where you can really think big. Again, these aren’t features you’ll need, but if you find a home in your budget that has all the must-haves, most of the nice-to-haves, and any of these, it’s a clear winner (examples: farmhouse sink, multiple walk-in closets, etc.).

Finally, once you’ve created your list and categorized it in a way that works for you, discuss it with your real estate advisor. They’ll be able to help you refine the list further, coach you through the best way to stick to it, and find a home in your area that meets your needs.

Bottom Line

Crafting your home search checklist may seem like a small task, but it can save you time and money. It’s also one of the keys to being successful in today’s competitive market. Let’s connect so we can work together to find a home that fits your wants and needs.

How an Energy Efficient Home Can Be a Bright Idea [INFOGRAPHIC]

![How an Energy Efficient Home Can Be a Bright Idea [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/03/23164218/20220325-MEM-1046x1745.png)

Some Highlights

- With inflation driving up the cost of everyday items, seeking out an energy-efficient home can be a great way to decrease the expenses you can control.

- Energy efficiency can help lower your utility bills and possibly even save you money on your taxes. Options to look for include efficient appliances, windows, and solar panels.

- If you’re planning to buy a home this year, consider energy efficiency in your search. Let’s connect so you can better understand features that can save you money for years to come.

There Are Several Great Reasons To Consider Buying a Condo Today

If you’re a first-time buyer looking to break into the housing market but struggling to find a home to buy, condominiums (or condos) could be a great alternative for you.

Here are a few reasons condos may be something you’ll want to consider.

Exploring Condos Could Add Options That Fit Your Budget

Supply challenges are a reality across the board in today’s housing market. Broadening your home search to include condos could increase your overall pool of options. Just keep in mind, condos generally differ from single-family homes in average space and floorplans.

In a recent article, Bankrate covers some of these differences:

“Condos are generally more affordable because they come with less space — you likely won’t have your own backyard, for example, and the interior tends to be smaller than the square footage of a single-family home.”

But if the size of a condominium meets your needs, they could match your budget as well. Data from the National Association of Realtors (NAR) shows the difference in the median price for both housing types. For single-family homes, the median price is $363,800. And for condominiums, the median price is lower at $305,400.

So, if budget is top of mind for you, a condominium could be a great fit within your target price range.

Not to mention, buying a condo is a great way to break into the market and start building equity that can help power a future move up. The condo you purchase today may not be your forever home, but it can be a great stairstep that can help you buy your dream home later on.

Find Out if Condo Living Is Right for You

In addition, owning and living in a condo is also a lifestyle choice. While it’s true they may be smaller than single-family homes, the amenities condos provide could be a draw for many buyers. Less space in your home might mean minimal upkeep, lower maintenance, and more time for you to spend doing the things you enjoy.

To understand if condo life is for you, Bankrate recommends asking yourself a few simple questions:

“Hate to mow the lawn and trim the hedges? What about pressure washing your driveway? Are your finances such that having to lay out $5,000 or more for a new roof will be a burden? . . . Condos tend to work best for those comfortable with most of the aspects of apartment living, minus the built-in maintenance.”

Ultimately, talking with an expert real estate advisor is the best first step to determining if condo living might work for you.

Bottom Line

Condominiums are a great option for many buyers, especially those looking to buy their first home. If you’re willing to consider condos in your search, you could find something that’s in line with your target numbers and your needs. To learn more, let’s connect so you have an expert in the condo-buying process on your side.