Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Technology Is Enabling the Real Estate Process

Today’s everyday reality is pretty different than it looked just a few weeks ago. We’re learning how to do a lot of things in new ways, from how we work remotely to how we engage with our friends and neighbors. Almost everything right now is shifting to a virtual format. One of the big changes we’re adapting to is the revisions to the common real estate transaction, which all vary by state and locality. Technology, however, is making it possible for many of us to continue on the quest for homeownership, an essential need for all.

Here’s a look at some of the elements of the process that are changing (at least in the near-term), due to stay-at-home orders and social distancing, and what you may need to know about each one if you’re thinking of buying or selling a home sooner rather than later.

1. Virtual Consultations – Instead of heading into an office, you can meet with real estate and lending professionals through video chat. Whether it’s your first initial needs analysis as a buyer or your listing appointment as a seller, you can still get the process started remotely and create a plan together. Your trusted advisor is still on your side.

2. Home Searches & Virtual Showings – According to theNational Association of Realtors (NAR), the Internet is one of the three most popular information sources buyers use when searching for homes. Your real estate agent can send you listing information and help you request a virtual showing when you’re ready to start looking. This means you can virtually walk through the homes on your wish list while keeping your family safe. As a seller, you can still have virtual open houses and virtual tours too, so as not to miss those buyers looking to find a home right now.

3. Document Signing – Although this is another area that varies by state, today more portions of the transaction are being done digitally. In many areas, your agent or loan officer can set up an account where you can upload all of the required documents and sign electronically right from your computer.

4. Sending Money – Whether you need to pay for an appraisal or submit closing costs, there are options available. Depending on the transaction and local regulations, you may be able to pay by credit card, and most banks will also allow you to wire funds from your account. Sometimes you can send a check by mail, and in some states, a mobile escrow agent will pick up a check from your home.

5. Closing Process – Again, depending on your area, a mobile notary may be able to bring the required documents to your home before the closing. If your state requires an attorney to be present, check with your legal counsel to see what options are available. Also, depending on the title company, some are allowing drive-thru closings, which is similar to doing a transaction at a bank window.

Although these virtual processes are starting to become more widely accepted, it does not mean that this is the way things are going to get done from now on. Under the current circumstances, however, technology is making it possible to continue much of the real estate transaction today.

Bottom Line

If you need to move today, technology can help make it happen; there are options available. Let’s touch base today to discuss your situation and our local regulations, so you don’t have to put your real estate plans on hold.

Recession? Yes. Housing Crash? No.

With over 90% of Americans now under a shelter-in-place order, many experts are warning that the American economy is heading toward a recession, if it’s not in one already. What does that mean to the residential real estate market?

What is a recession?

According to the National Bureau of Economic Research:

“A recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

COVID-19 hit the pause button on the American economy in the middle of March. Goldman Sachs, JP Morgan, and Morgan Stanley are all calling for a deep dive in the economy in the second quarter of this year. Though we may not yet be in a recession by the technical definition of the word today, most believe history will show we were in one from April to June.

Does that mean we’re headed for another housing crash?

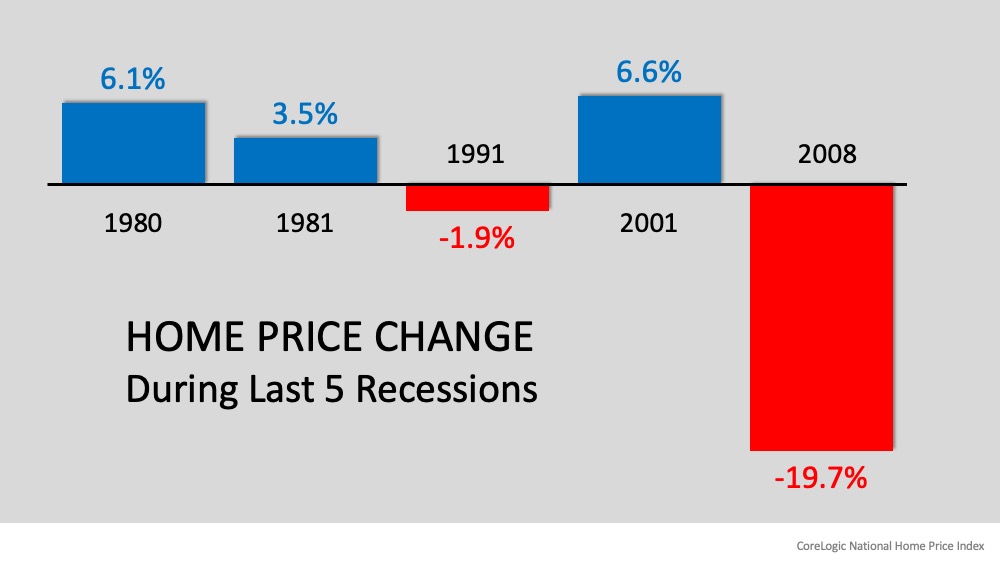

Many fear a recession will mean a repeat of the housing crash that occurred during the Great Recession of 2006-2008. The past, however, shows us that most recessions do not adversely impact home values. Doug Brien, CEO of Mynd Property Management, explains:

“With the exception of two recessions, the Great Recession from 2007-2009, & the Gulf War recession from 1990-1991, no other recessions have impacted the U.S. housing market, according to Freddie Mac Home Price Index data collected from 1975 to 2018.”

CoreLogic, in a second study of the last five recessions, found the same. Here’s a graph of their findings:

What are the experts saying this time?

This is what three economic leaders are saying about the housing connection to this recession:

Robert Dietz, Chief Economist with NAHB

“The housing sector enters this recession underbuilt rather than overbuilt…That means as the economy rebounds – which it will at some stage – housing is set to help lead the way out.”

Ali Wolf, Chief Economist with Meyers Research

“Last time housing led the recession…This time it’s poised to bring us out. This is the Great Recession for leisure, hospitality, trade and transportation in that this recession will feel as bad as the Great Recession did to housing.”

John Burns, founder of John Burns Consulting, also revealed that his firm’s research concluded that recessions caused by a pandemic usually do not significantly impact home values:

“Historical analysis showed us that pandemics are usually V-shaped (sharp recessions that recover quickly enough to provide little damage to home prices).”

Bottom Line

If we’re not in a recession yet, we’re about to be in one. This time, however, housing will be the sector that leads the economic recovery.

Why the Stock Market Correction Probably Won’t Impact Home Values

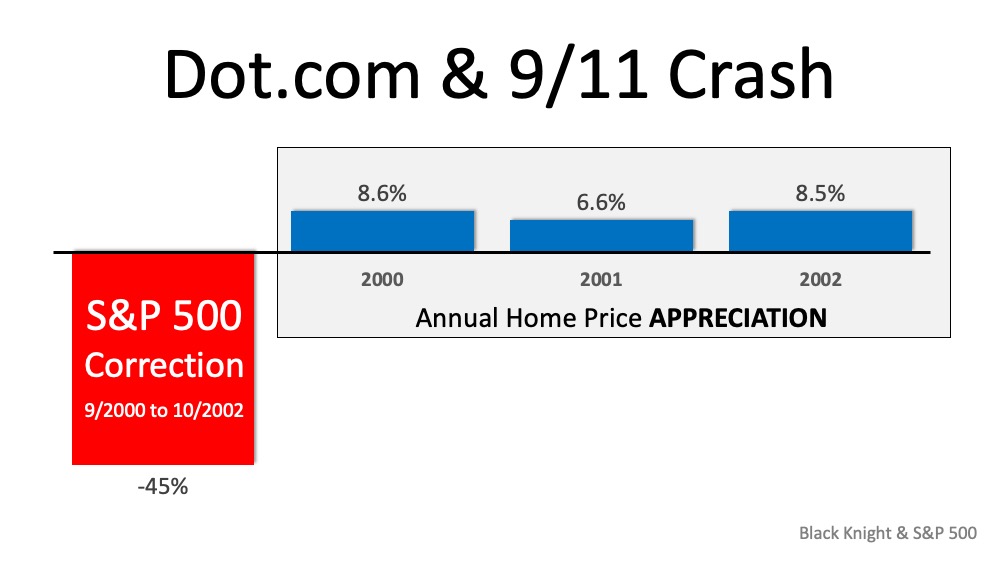

With the housing crash of 2006-2008 still visible in the rear-view mirror, many are concerned the current correction in the stock market is a sign that home values are also about to tumble. What’s taking place today, however, is nothing like what happened the last time. The S&P 500 did fall by over fifty percent from October 2007 to March 2009, and home values did depreciate in 2007, 2008, and 2009 – but that was because that economic slowdown was mainly caused by a collapsing real estate market and a meltdown in the mortgage market.

This time, the stock market correction is being caused by an outside event (the coronavirus) with no connection to the housing industry. Many experts are saying the current situation is much more reminiscent of the challenges we had when the dot.com crash was immediately followed by 9/11. As an example, David Rosenberg, Chief Economist with Gluskin Sheff + Associates Inc., recently explained:

“What 9/11 has in common with what is happening today is that this shock has also generated fear, angst and anxiety among the general public. People avoided crowds then as they believed another terrorist attack was coming and are acting the same today to avoid getting sick. The same parts of the economy are under pressure ─ airlines, leisure, hospitality, restaurants, entertainment ─ consumer discretionary services in general.”

Since the current situation resembles the stock market correction in the early 2000s, let’s review what happened to home values during that time. The S&P dropped 45% between September 2000 and October 2002. Home prices, on the other hand, appreciated nicely at the same time. That stock market correction proved not to have any negative impact on home values.

The S&P dropped 45% between September 2000 and October 2002. Home prices, on the other hand, appreciated nicely at the same time. That stock market correction proved not to have any negative impact on home values.

Bottom Line

If the current situation is more like the markets in the early 2000s versus the markets during the Great Recession, home values should be minimally affected, if at all.

Economic Slowdown: What the Experts Are Saying

More and more economists are predicting a recession is imminent as the result of the pullback in the economy caused by COVID-19. According to the National Bureau of Economic Research:

“A recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, industrial production, and wholesale-retail sales.”

Bill McBride, the founder of Calculated Risk, believes we are already in a recession:

“With the sudden economic stop, and with many states shutting down by closing down schools, bars and restaurants…my view is the US economy is now in a recession (started in March 2020), and GDP will decline sharply in Q2. The length of the recession will depend on the course of the pandemic.”

How deep will it go?

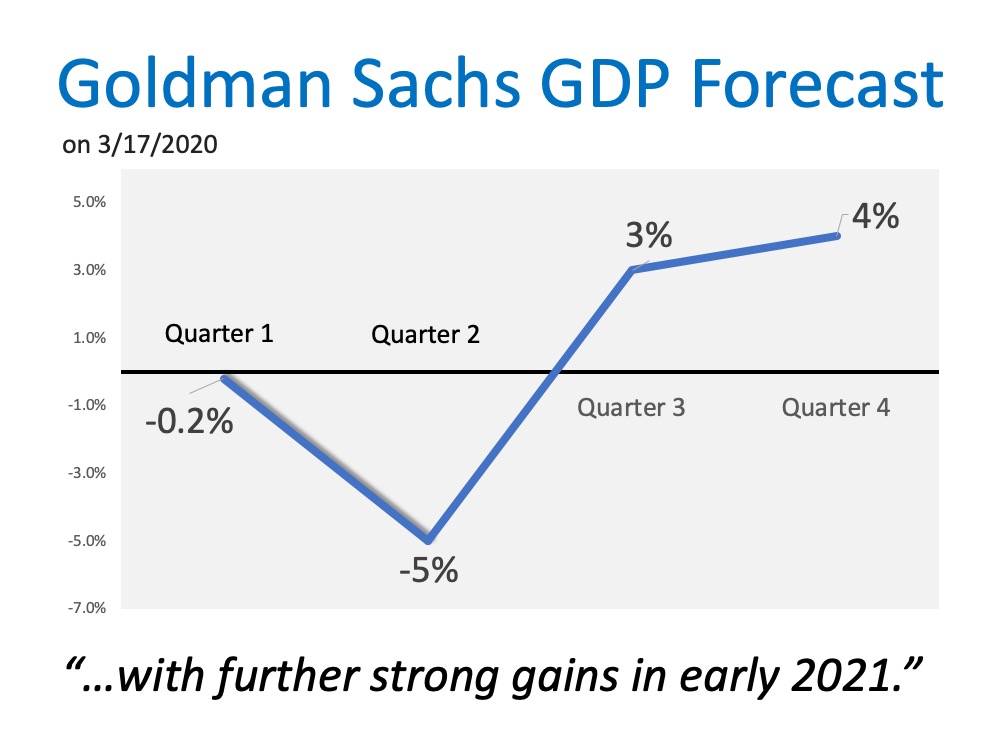

No one knows for sure. It depends on how long it takes to beat this virus. Goldman Sachsanticipates we will see a difficult first half of the year, but the economy will recover in the second half (see below): Goldman also projects we’ll have “further strong gains in early 2021.”

Goldman also projects we’ll have “further strong gains in early 2021.”

This aligns with the projection from Wells Fargo Investment Institute:

“Once the virus infection rate peaks, we expect a recovery to gain momentum into the final quarter of the year and especially into 2021.”

Again, no one knows for sure how long the pandemic will last. The hope is that it will resolve sometime over the next several months. Most agree that when it does, the economy will regain its strength quickly.

*QUARTER 1 DATA FROM GOLDMAN SACHS WAS UPDATED FROM 0% TO -0.2% ON 3/17/20 AFTER THE INITIAL RELEASE.

Bottom Line

This virus is not only impacting the physical health of Americans, but also the financial health of the nation. The sooner we beat it, the sooner our lives will return to normal.

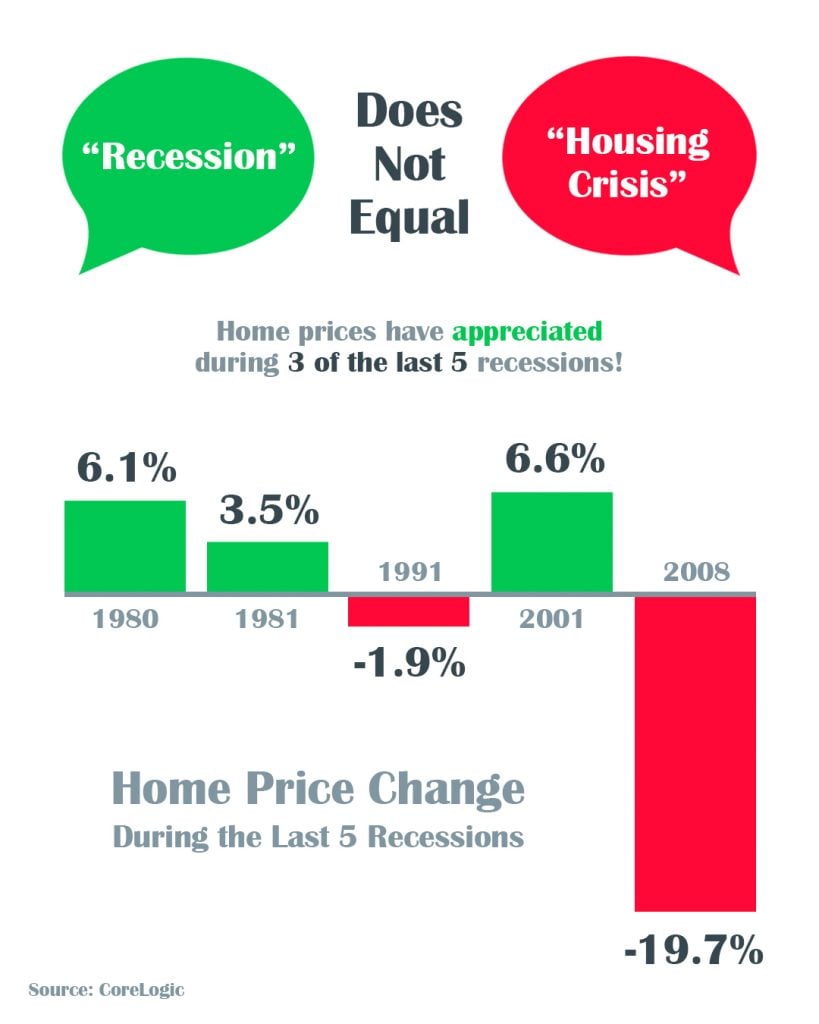

A Recession Does Not Equal a Housing Crisis [INFOGRAPHIC]

Some Highlights

- The COVID-19 pandemic is causing an economic slowdown.

- The good news is, home values actually increased in 3 of the last 5 U.S. recessions and decreased by less than 2% in the 4th.

- All things considered, an economic slowdown does not equal a housing crisis, and this will not be a repeat of 2008.

Are We About to See a New Wave of Foreclosures?

With all of the havoc being caused by COVID-19, many are concerned we may see a new wave of foreclosures. Restaurants, airlines, hotels, and many other industries are furloughing workers or dramatically cutting their hours. Without a job, many homeowners are wondering how they’ll be able to afford their mortgage payments.

In spite of this, there are actually many reasons we won’t see a surge in the number of foreclosures like we did during the housing crash over ten years ago. Here are just a few of those reasons:

The Government Learned its Lesson the Last Time

During the previous housing crash, the government was slow to recognize the challenges homeowners were having and waited too long to grant relief. Today, action is being taken swiftly. Just this week:

- The Federal Housing Administration indicated it is enacting an “immediate foreclosure and eviction moratorium for single family homeowners with FHA-insured mortgages” for the next 60 days.

- The Federal Housing Finance Agency announced it is directing Fannie Mae and Freddie Macto suspend foreclosures and evictions for “at least 60 days.”

Homeowners Learned their Lesson the Last Time

When the housing market was going strong in the early 2000s, homeowners gained a tremendous amount of equity in their homes. Many began to tap into that equity. Some started to use their homes as ATM machines to purchase luxury items like cars, jet-skis, and lavish vacations. When prices dipped, many found themselves in a negative equity situation (where the mortgage was greater than the value of their homes). Some just walked away, leaving the banks with no other option but to foreclose on their properties.

Today, the home equity situation in America is vastly different. From 2005-2007, homeowners cashed out $824 billion worth of home equity by refinancing. In the last three years, they cashed out only $232 billion, less than one-third of that amount. That has led to:

- 37% of homes in America having no mortgage at all

- Of the remaining 63%, more than 1 in 4 having over 50% equity

Even if prices dip (and most experts are not predicting that they will), most homeowners will still have vast amounts of value in their homes and will not walk away from that money.

There Will Be Help Available to Individuals and Small Businesses

The government is aware of the financial pain this virus has caused and will continue to cause. Yesterday, the Associated Press reported:

“In a memorandum, Treasury proposed two $250 billion cash infusions to individuals: A first set of checks issued starting April 6, with a second wave in mid-May. The amounts would depend on income and family size.”

The plan also recommends $300 billion for small businesses.

Bottom Line

These are not going to be easy times. However, the lessons learned from the last crisis have Americans better prepared to weather the financial storm. For those who can’t, help is on the way.

Two Big Myths in the Homebuying Process

The 2020 Millennial Home Buyer Report shows how this generation is not really any different from previous ones when it comes to homeownership goals:

“The majority of millennials not only want to own a home, but 84% of millennials in 2019 considered it a major part of the American Dream.”

Unfortunately, the myths surrounding the barriers to homeownership – especially those related to down payments and FICO® scores – might be keeping many buyers out of the arena. The piece also reveals:

“Millennials have to navigate a lot of obstacles to be able to own a home. According to our 2020 survey, saving for a down payment is the biggest barrier for 50% of millennials.”

Millennial or not, unpacking two of the biggest myths that may be standing in the way of homeownership among all generations is a great place to start the debunking process.

Myth #1: “I Need a 20% Down Payment”

Many buyers often overestimate what they need to qualify for a home loan. According to the same article:

“A down payment of 20% for a home of that price [$210,000] would be about $42,000; only about 30% of the millennials in our survey have enough in savings to cover that, not to mention the additional closing costs.”

While many potential buyers still think they need to put at least 20% down for the home of their dreams, they often don’t realize how many assistance programs are available with as little as 3% down. With a bit of research, many renters may be able to enter the housing market sooner than they ever imagined.

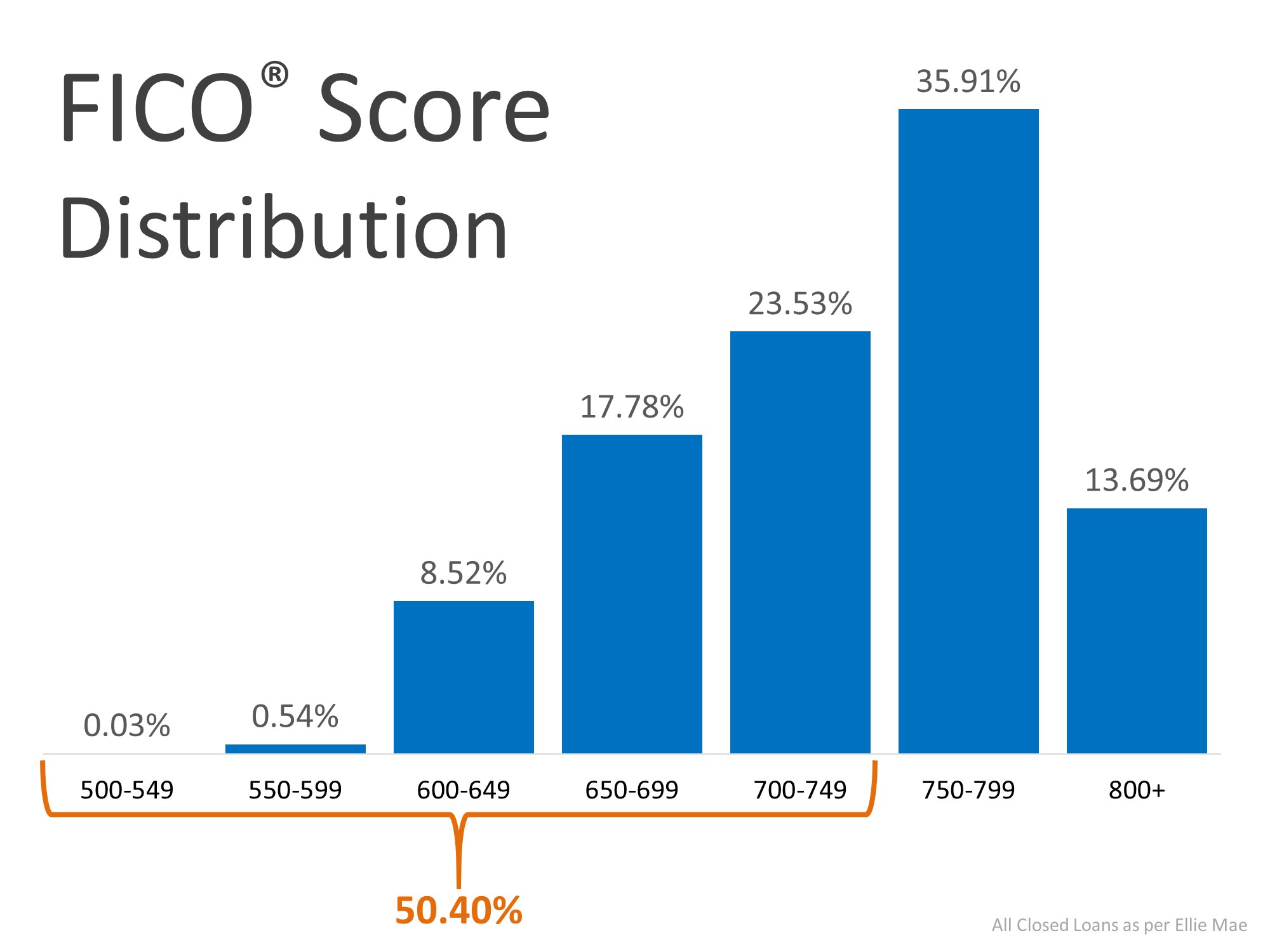

Myth #2: “I Need a 780 FICO® Score or Higher”

In addition to down payments, buyers are also often confused about the FICO® score it takes to qualify for a mortgage, believing they need a credit score of 780 or higher.

Ellie Mae’s latest Origination Insight Report, which focuses on recently closed (approved) loans, shows the truth is, over 50% of approved loans were granted with a FICO® score below 750 (see graph below): Even today, many of the myths of the homebuying process are unfortunately keeping plenty of motivated buyers on the sidelines. In reality, it really doesn’t have to be that way.

Even today, many of the myths of the homebuying process are unfortunately keeping plenty of motivated buyers on the sidelines. In reality, it really doesn’t have to be that way.

Bottom Line

If you’re thinking of buying a home, you may have more options than you think. Let’s connect to answer your questions and help you determine your next steps.

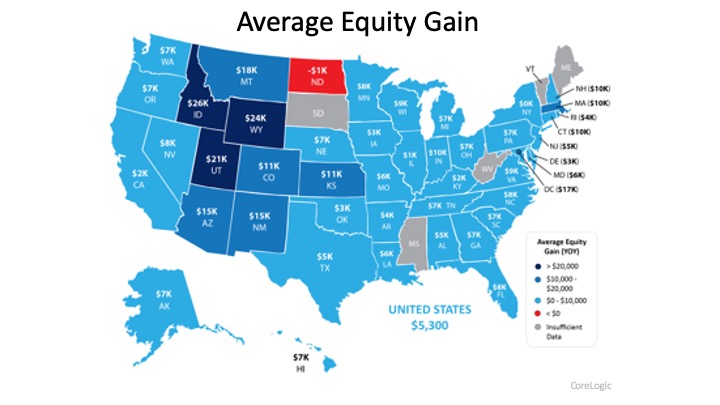

Equity Gain Growing in Nearly Every State

Rising home prices have been in the news a lot lately, and much of the focus is on whether they’re accelerating too quickly and how sustainable the growth in prices really is. One of the often-overlooked benefits of rising prices, however, is the impact they have on a homeowner’s equity position.

Home equity is defined as the difference between a home’s fair market value and the outstanding balance of all liens on the property. While homeowners pay down their mortgages, the amount of equity they have in their homes climbs each time the value increases.

Today, the number of homeowners that currently have significant equity in their homes is growing. According to the Census Bureau, 38% of all homes in the country are mortgage-free. In a home equity study, ATTOM Data Solutions revealed that of the 54.5 million homes with a mortgage, 26.7% of them have at least 50% equity. That number has been increasing over the last eight years.

CoreLogic also notes:

“…the average homeowner gained approximately $5,300 in equity during the past year.”

The map below shows a breakdown of the increasing equity gain across the country, painting a clear picture that home equity is growing in nearly every state.

Bottom Line

This may be the year to take advantage of your home equity by applying it forward, either as you downsize or as you move up to a new home.

Want to see what your home is worth? Use our quick and easy Home Value Estimator.

Confidence Is the Key to Success for Young Homebuyers

[et_pb_section fb_built=”1″ _builder_version=”3.18.2″][et_pb_row _builder_version=”3.18.2″][et_pb_column type=”4_4″ _builder_version=”3.18.2″ parallax=”off” parallax_method=”on”][et_pb_text _builder_version=”3.18.2″]

Buying your first home can seem overwhelming. Thankfully, there’s a lot of great information out there to help you feel more confident as you learn about the process. For those in younger generations who aspire to buy, here are three things to consider sooner rather than later in your journey:

1. Understand What it Takes to Purchase a Home

Overall, Millennials make up the largest group of homebuyers in today’s real estate market, and Gen Z is not too far behind. A recent study shared by Freddie Mac shows, however, that Generation Z isn’t as confident in the homebuying process as Millennials. The best thing potential young buyers can do is understand what it takes to buy a home. Learn as much as you can about the mortgage process, down payment options, and the overall steps to take along the way.

2. Realize Your Opportunity to Build Wealth

Homeownership allows you the chance to put a small portion of the home’s value down when you buy, and then watch your appreciation grow on the full value of the home – not just on the down payment. It’s one of the best investments you can make, and a form of ‘forced savings’ working in your favor over time. The added bonus? You get to live there, too.

3. Find Someone You Trust to Help You Through the Process

Having someone you trust to guide you through this process is invaluable. Finding a local real estate expert to help you navigate through the transaction and feel more confident as you make important decisions could be the best choice you make.

For Millennials and Gen Z’ers thinking about buying, today’s historically low interest ratescombined with the outlook for future home appreciation is a big win. This means whatever you buy today, you’ll be bragging about 10 years from now. You can feel confident about that!

Bottom Line

If you’re ready, buying your first home sooner rather than later is one of the best decisions you can make. But there are many things to consider before taking that step, so let’s work together to help you confidently navigate the full journey.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]