Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

April 2022 Housing Market Update

Geoff Green is President of Green Team Realty and Co-founder and CEO of NuOp. In addition, he is the moderator of the monthly Housing Market Updates. With so many changes in the market, Geoff began the April 2022 Housing Market Update with information on rising mortgage rates.

If you haven’t yet seen the April 2022 Housing Market Update or would like to watch it again, it’s available below.

Geoff provided some historical perspectives on rising rates and their impact. With statistics going back to 1993, it appears that prices will continue to climb even as rates are climbing.

Spring Market

Buyer traffic is very strong. Inventory continues to be very low. However, there has been a slight bump in active listings for the first time in 6 months. According to Lance Lambert, Editorial Director, Fortune,

“…some experts say that 2022 spring housing market might go down as one of the most competitive on record.”

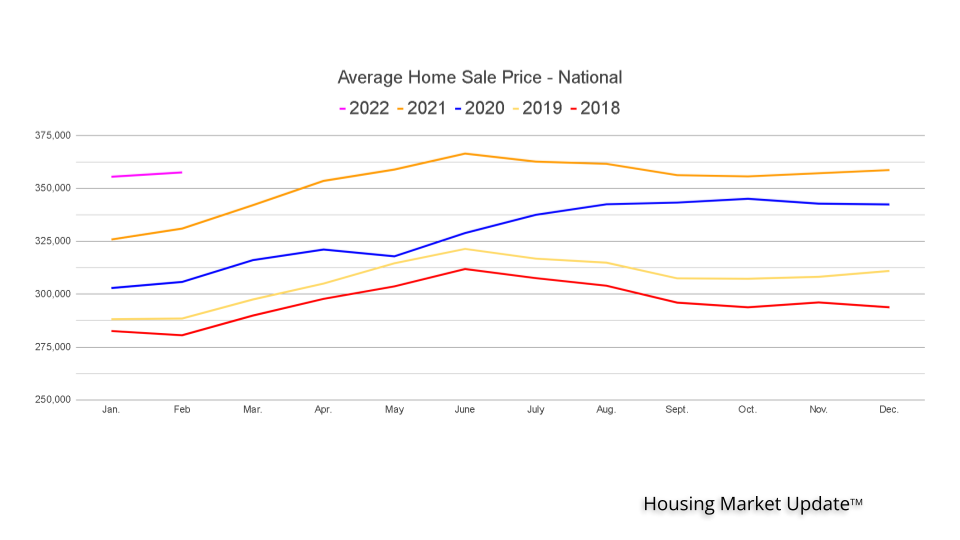

Home Sale Price

The year-over-year stats show that sales prices are not going backward.

Meet our Panel

Vikki Garby, of Green Team New York Realty and Michael Giannetto of CrossCountry Mortgage, joined Geoff for their take on the market. To watch the panel discussion, click here.

Thanks to our Sponsor

NuOp is the Business Opportunity Exchange. View a live feed of Real Estate and Mortgage Referrals on NuOp.com

Sign up for Housing Market Updates

Join us for our next Housing Market Update on May 15, 2022. To stay informed and sign up for our housing market updates, click here.

How To Approach Rising Mortgage Rates as a Buyer

In the last few weeks, the average 30-year fixed mortgage rate from Freddie Mac inched up to 5%. While that news may have you questioning the timing of your home search, the truth is, timing has never been more important. Even though you may be tempted to put your plans on hold in hopes that rates will fall, waiting will only cost you more. Mortgage rates are forecast to continue rising in the year ahead.

If you’re thinking of buying a home, here are a few things to keep in mind so you can succeed even as mortgage rates rise.

How Rising Mortgage Rates Impact You

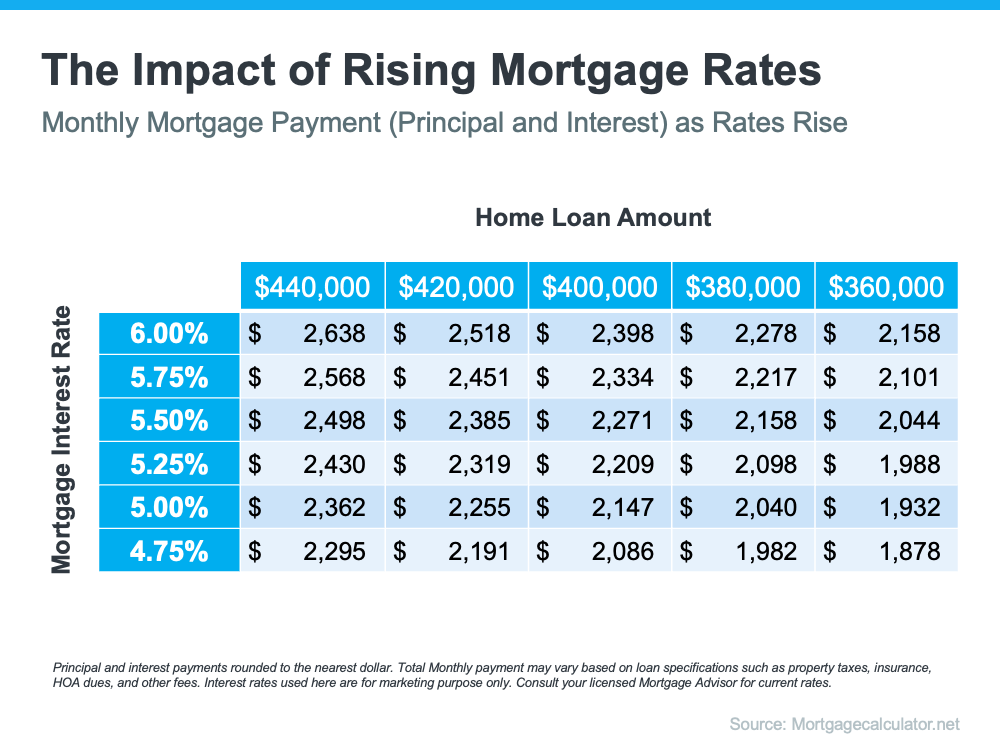

Mortgage rates play a significant role in your home search. As rates go up, they impact how much you’ll pay in your monthly mortgage payment, which directly affects how much you can comfortably afford. Here’s an example of how even a quarter-point increase can have a big impact on your monthly payment (see chart below):

With mortgage rates on the rise, you’ve likely seen your purchasing power impacted already. Instead of delaying your plans, today’s rates should motivate you to purchase now before rates increase more. Use that motivation to energize your search and plan your next steps accordingly.

The best way to prepare is to work with a trusted real estate advisor now. An agent can connect you with a trusted lender, help you adjust your search based on your budget, and make sure you’re ready to act quickly when it’s time to make an offer.

Bottom Line

Serious buyers should approach rising rates as a motivating factor to buy sooner, not a reason to wait. Waiting will cost you more in the long run. Let’s connect today so you can better understand your budget and be prepared to buy your home even before rates climb higher.

Where Are Mortgage Rates Headed?

There’s never been a truer statement regarding forecasting mortgage rates than the one offered last year by Mark Fleming, Chief Economist at First American:

“You know, the fallacy of economic forecasting is: Don’t ever try and forecast interest rates and or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

Coming into this year, most experts projected mortgage rates would gradually increase and end 2022 in the high three-percent range. It’s only April, and rates have already blown past those numbers. Freddie Mac announced last week that the 30-year fixed-rate mortgage is already at 4.72%.

Danielle Hale, Chief Economist at realtor.com, tweeted on March 31:

“Continuing on the recent trajectory, would have mortgage rates hitting 5% within a matter of weeks. . . .”

Just five days later, on April 5, the Mortgage News Daily quoted a rate of 5.02%.

No one knows how swiftly mortgage rates will rise moving forward. However, at least to this point, they haven’t significantly impacted purchaser demand. Ali Wolf, Chief Economist at Zonda, explains:

“Mortgage rates jumped much quicker and much higher than even the most aggressive forecasts called for at the end of last year, and yet housing demand appears to be holding steady.”

Through February, home prices, the number of showings, and the number of homes receiving multiple offers all saw a substantial increase. However, much of the spike in mortgage rates occurred in March. We will not know the true impact of the increase in mortgage rates until the March housing numbers become available in early May.

Rick Sharga, EVP of Market Intelligence at ATTOM Data, recently put rising rates into context:

“Historically low mortgage rates and higher wages helped offset rising home prices over the past few years, but as home prices continue to soar and interest rates approach five percent on a 30-year fixed rate loan, more consumers are going to struggle to find a property they can comfortably afford.”

While no one knows exactly where rates are headed, experts do think they’ll continue to rise in the months ahead. In the meantime, if you’re looking to buy a home, know that rising rates do have an impact. As rates rise, it’ll cost you more when you purchase a house. If you’re ready to buy, it may make sense to do so sooner rather than later.

Bottom Line

Mark Fleming got it right. Forecasting mortgage rates is an impossible task. However, it’s probably safe to assume the days of attaining a 3% mortgage rate are over. The question is whether that will soon be true for 4% rates as well.

The Future of Home Price Appreciation and What It Means for You

Many consumers are wondering what will happen with home values over the next few years. Some are concerned that the recent run-up in home prices will lead to a situation similar to the housing crash 15 years ago.

However, experts say the market is totally different today. For example, Odeta Kushi, Deputy Chief Economist at First American, tweeted just last week on this issue:

“. . . We do need price appreciation to slow today (it’s not sustainable over the long run) but high price growth today is supported by fundamentals- short supply, lower rates & demographic demand. And we are in a much different & safer space: better credit quality, low DTI [Debt-To-Income] & tons of equity. Hence, a crash in prices is very unlikely.”

Price appreciation will slow from the double-digit levels the market has seen over the last two years. However, experts believe home values will not depreciate (where a home would lose value).

To this point, Pulsenomics just released the latest Home Price Expectation Survey – a survey of a national panel of over 100 economists, real estate experts, and investment and market strategists. It forecasts home prices will continue appreciating over the next five years. Below are the expected year-over-year rates of home price appreciation based on the average of all 100+ projections:

- 2022: 9%

- 2023: 4.74%

- 2024: 3.67%

- 2025: 3.41%

- 2026: 3.57%

Those responding to the survey believe home price appreciation will still be relatively high this year (though half of what it was last year), and then return to more normal levels over the next four years.

What Does This Mean for You as a Buyer?

With a limited supply of homes available for sale and both prices and mortgage rates increasing, it can be a challenging market to navigate as a buyer. But buying a home sooner rather than later does have its benefits. If you wait to buy, you’ll pay more in the future. However, if you buy now, you’ll actually be in the position to make future price increases work for you. Once you buy, those rising home prices will help you build your home’s value, and by extension, your own household wealth through home equity.

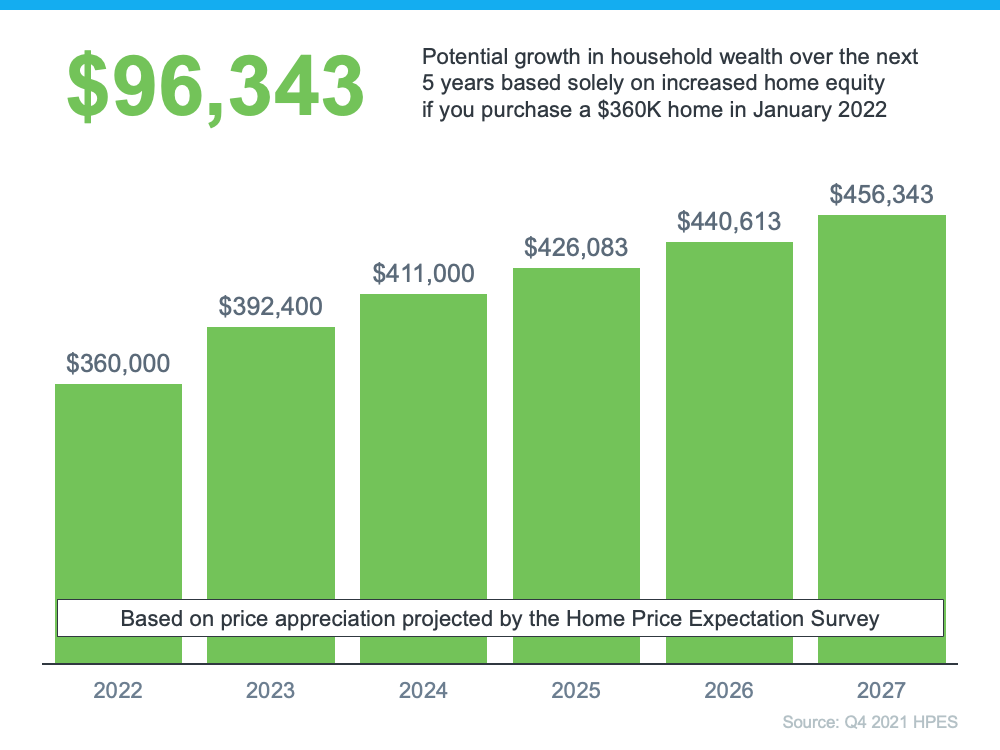

As an example, let’s assume you purchased a $360,000 home in January of this year (the median price according to the National Association of Realtors rounded up to the nearest $10K). If you factor in the forecast for appreciation from the Home Price Expectation Survey, you could accumulate over $96,000 in household wealth over the next five years (see graph below):

Bottom Line

If you’re trying to decide whether to buy now or wait, the key is knowing what’s expected to happen with home prices. Experts say prices will continue to climb in the years ahead, just at a slower pace. So, if you’re ready to buy, doing so now may be your best bet for your wallet. It’ll also give you the chance to use the future home price appreciation to build your own net worth through rising equity. If you want to get started, let’s connect today.

Remote Work Trends Mean Flexibility for First-Time Homebuyers

Today’s low inventory can be challenging for homebuyers, especially if you’re looking to purchase your first home. But if you’re one of many people who work remotely, you may have a great opportunity to use the flexibility you have at work to achieve your homebuying goals this year.

In a recent report, Arch Capital Services explains how the ongoing trend of remote work can open up more options for homebuyers:

“. . . This will enable those who are able to work from home on a part-time or hybrid basis to move slightly farther away from job centers. . . . For workers who secure full-time remote jobs, their place of residence will be determined by affordability and personal preferences.”

Basically, working from home is great news if you’re a first-time buyer trying to find a home that meets your needs and budget. Here’s a deeper look at how it could benefit you.

Extra Flexibility in Your Career Means Extra Flexibility in Your Home Search

If your job is 100% remote, you don’t have to be tied to a specific location or office. So, if you’ve been having a hard time finding what you want in your local area, it may be time to expand your search.

One option you could consider is moving to a place where you’ve always wanted to live, like the mountains, beach, or closer to loved ones. When you broaden your search radius to include those locations, it’ll give you additional homes to consider.

It could also allow you to search for a more affordable location where you have more options in your price range. This can help you achieve two goals – saving money and finding additional features that meet your needs. To truly highlight this benefit, a recent First American article discusses the great ways remote work can really help you with your homebuying goals. Ksenia Potapov, Economist at First American, says:

“For potential first-time home buyers, leveraging their house-buying power in more affordable markets can also help them buy more attractive homes – more square footage and rooms, more options for different home styles and neighborhood amenities – increasing the opportunity to find a home that suits their preferences.”

That means you can use your work flexibility to search for homes with the amenities you need at a lower price point.

Bottom Line

Remote work doesn’t just give you expanded flexibility for your career. If you’re no longer tied to a location because of your office, you have a great opportunity to expand your housing search. Let’s connect to explore how this can open up your options.

What’s Happening with Mortgage Rates, and Where Will They Go from Here?

Based on the Primary Mortgage Market Survey from Freddie Mac, the average 30-year fixed-rate mortgage has increased by 1.2% (3.22% to 4.42%) since January of this year. The rate jumped by more than a quarter of a point from just a week ago. Here’s a visual to show how mortgage rate movement throughout 2021 was steady compared to the rapid increase in mortgage rates this year:

Just a few months ago, Freddie Mac projected mortgage rates would average 3.6% in 2022. Earlier this month, Fannie Mae forecast mortgage rates would average 3.8% in 2022. As the chart above shows, rates have already surpassed those projections.

Sam Khater, Chief Economist at Freddie Mac, explained in a press release last week:

“This week, the 30-year fixed-rate mortgage increased by more than a quarter of a percent as mortgage rates across all loan types continued to move up. Rising inflation, escalating geopolitical uncertainty and the Federal Reserve’s actions are driving rates higher and weakening consumers’ purchasing power.”

Where Are Mortgage Rates Going from Here?

In a recent article by Bankrate, several industry experts weighed in on where rates might be headed going forward. Here are some of their forecasts:

Greg McBride, Chief Financial Analyst, Bankrate:

“With inflation figures continuing to surprise to the upside, mortgage rates will remain above 4.0% on the 30-year fixed.”

Nadia Evangelou, Senior Economist and Director of Forecasting, National Association of Realtors (NAR):

“While higher short-term interest rates will push up mortgage rates, I expect some of this impact to be mitigated eventually through lower inflation. Thus, I expect the 30-year fixed mortgage rate to continue to rise, although we aren’t likely to see the big jumps that occurred over the past few weeks.”

Len Kiefer, Deputy Chief Economist, Freddie Mac:

“Mortgage rates are likely to continue to move higher throughout the balance of 2022, although the pace of rate increases is likely to moderate.”

In a recent realtor.com article, another expert adds to the conversation:

Danielle Hale, Chief Economist, realtor.com:

“. . . As markets digest the Fed’s updated economic projections, I anticipate a continued increase in mortgage rates over the next several months. . . .”

What Does This Mean for You if You’re Looking To Buy a Home?

With both mortgage rates and home values expected to increase throughout the year, it would be better to buy sooner rather than later if you’re able. That’s because it’ll cost you more the longer you wait. But, there is a possible silver lining to buying a home right now. While you’ll be paying a higher price and a higher mortgage rate than you would have last year, rising prices do have a long-term benefit once you buy.

If you purchase a home today valued at $400,000 and put 10% down, you would be taking out a $360,000 mortgage. According to mortgagecalculator.net, at a 4.42% fixed mortgage rate, your mortgage payment would be $1,807 a month (this does not include insurance, taxes, and other fees because those vary by location).

Now, let’s put that mortgage payment into a new perspective based on the substantial growth in equity that comes with the escalation in home prices. Every quarter, Pulsenomics surveys a panel of over 100 economists, investment strategists, and housing market analysts about their expectations for future home prices in the United States. Last week, Pulsenomics released their latest Home Price Expectation Survey. The survey reveals that the average of the experts’ forecasts calls for a 9% increase in home values in 2022.

Based on those projections, a $400,000 house you buy today could be valued at $436,000 by this time next year. If you break that down, that means the equity in your home would increase by $3,000 a month over that period. That’s greater than the estimated monthly payment above. Granted, the increase in your net worth is tied to the home, but it is one way to put the home price appreciation to use in a way that benefits you.

Bottom Line

Paying a higher price for a home and a higher mortgage rate can be a difficult pill to swallow. However, waiting will just cost you more. If you’re ready, willing, and able to buy a home, now will be a better time than a year, or even six months from now. Let’s connect to begin the process today.

The Best Week To List Your House Is Just Around the Corner

Are you thinking about selling your house? If so, you may want to make it a priority to start the process soon. According to realtor.com, the sweet spot for sellers is just around the corner. In a recent study, experts analyzed housing market trends by looking at data from the past several years (excluding 2020, since it was an atypical year). When applied to the current market, experts determined the ideal week to list a house this year. The research says:

“Home sellers on the fence waiting for that perfect moment to sell should start preparations, because the best time to list a home in 2022 is approaching quickly. The week of April 10-16 is expected to have the ideal balance of housing market conditions that favor home sellers, more so than any other week in the year.”

If you’ve been putting your move on the back burner waiting for the ideal time to sell, you should know your golden window of opportunity is coming up. If you’re able to get your house ready quickly, here’s what you can expect from that week.

You Should See More Buyer Activity

The article expects higher buyer demand based on what’s happened in previous years. This could result in increased competition among buyers and ultimately a bidding war over your house. And since mortgage rates recently ticked up over 4%, chances are good that analysis is right. When rates rise, experts say buyers often hurry to make their purchase before rates climb higher. As Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), says:

“. . . Buyers are rushing to lock in lower rates as the outlook is for even higher mortgage rates in the following months.”

Your House Is Expected To Sell Quickly

Additionally, the realtor.com analysis shows houses sell even faster during this week of the year, likely due to the heightened buyer demand. If you work with a trusted real estate professional to price your house right, it should sell quickly. And when homes are already selling in just 18 days according to NAR, that could set you up for a big win.

Your House Will Be in the Spotlight

Since the beginning of the year, the number of homes available for sale has been at or near record lows. According to the realtor.com study, the typical trend for this week of the year is that there will be even fewer sellers on the market. If you list when inventory is low, your house will be the center of attention for eager buyers craving options.

If you’re ready to move fast, you may want to shoot for April 10th-16th as your target goal. Just remember, even if you’re not ready to list within the next couple of weeks, rest assured this is still a hot sellers’ market. If you list later in April, you’ll still be in the driver’s seat.

Bottom Line

Ready to get the ball rolling? Let’s connect and schedule a time to go over your next steps. In the meantime, make a checklist of things you need to tackle to get your house ready. When we talk, we can prioritize your to-do list and get you on the road to selling your house.

What You Need To Know if You’re Thinking About Building a Home

If you’re ready to move up, you may be trying to decide whether you want to buy a home that’s already on the market or build a new one. And since the supply of homes available for sale today is low, you’re willing to consider either avenue. While home builders are doing everything they can to construct more houses and help narrow the supply shortage, they’re also facing delays due to factors outside of their control.

Here’s the latest on some of the key challenges homebuilders are experiencing today and how they could impact your plans to move up. When you know what’s happening in the industry, you can make an informed decision on whether to look for a newly built or an existing home in your home search.

Supply Chain Issues

The first hurdle builders are dealing with is the lack of supply of various building materials. According to a recent article from HousingWire:

“. . . Nearly everything needed in the homebuilding process is facing some sort of delay and subsequent price increase.”

The supply issue isn’t just with lumber, even though that’s what’s covered most in the news. The article explains many other supplies are impacted too, including roofing materials, windows, garage doors, siding, and gypsum (which is used in drywall).

The difficulty in getting these items is dragging out timelines for new homes as builders wait on what they need to finish construction. And since materials are in short supply, even when they do get the product, the principle of supply and demand is driving prices up for those goods. HousingWire explains it like this:

“When supplies are low, charges inevitably go up, . . . Meanwhile, a lack of availability is causing huge delays, meaning builders are struggling to stay on schedule.”

The National Association of Home Builders (NAHB) agrees:

“Builders are grappling with supply-chain issues that are extending construction times and increasing costs.”

Skilled Labor Shortage

But that’s not the only challenge with new home construction today. Builders are also having a hard time finding skilled labor, which means they’re short-handed, further dragging out their timelines. Odeta Kushi, Deputy Chief Economist at First American, says this is an ongoing challenge for the industry:

“The skilled labor shortage in the construction industry is not new – it’s been an issue for more than a decade now.”

But there is good news. The February jobs report shows employment gains in the construction industry. Kushi puts this encouraging news into perspective in the article mentioned above:

“Overall this was a good report, . . . The supply of workers continues to fall short of demand, but the underlying momentum of the labor market recovery is strong, and falling COVID case counts provide further forward momentum.”

That means, while finding workers continues to be a challenge for builders, there are signs of positive momentum moving forward.

How This Impacts You

HousingWire explains how these things can impact move-up buyers today:

“The residential construction industry is facing a crisis as builders manage the critical shortage of building materials and labor. Explosive supply and labor costs are forcing long delays. . . .”

So, when you weigh your options and try to decide between building a home or buying an existing one, factor the potential delay in new home construction into your decision. While it doesn’t mean you should cross newly built homes off your list, it does mean you should consider your timeline and if you’re willing to wait while your home is being constructed.

Bottom Line

When planning your next move, understanding the latest market conditions is key to making the best decision possible. To make sure you have all the information you need, let’s connect. Together we can make sure you know what’s happening in our local market so you can confidently decide what’s right for you, your priorities, and your timeline.

The #1 Reason To Sell Your House Today

Almost every industry is currently struggling with supply chain disruptions. This also applies to the current U.S. housing market, where buyer demand far exceeds housing supply.

Purchaser demand is very strong right now. The National Association of Realtors (NAR) just released their latest Existing Home Sales Report which reveals that sales surged in January. Existing home sales rose to a seasonally adjusted annual rate of 6.5 million – an increase of 6.7% from the prior month, with sales up in all regions. However, there’s one big challenge.

Inventory Is at an All-Time Low

Because purchaser demand is so high, the market is running out of available homes for sale. The above-mentioned report states that the current months’ supply of inventory of homes for sale has fallen to 1.6 months. This prompts Lawrence Yun, Chief Economist at NAR, to say:

“The inventory of homes on the market remains woefully depleted, and in fact is currently at an all-time low.”

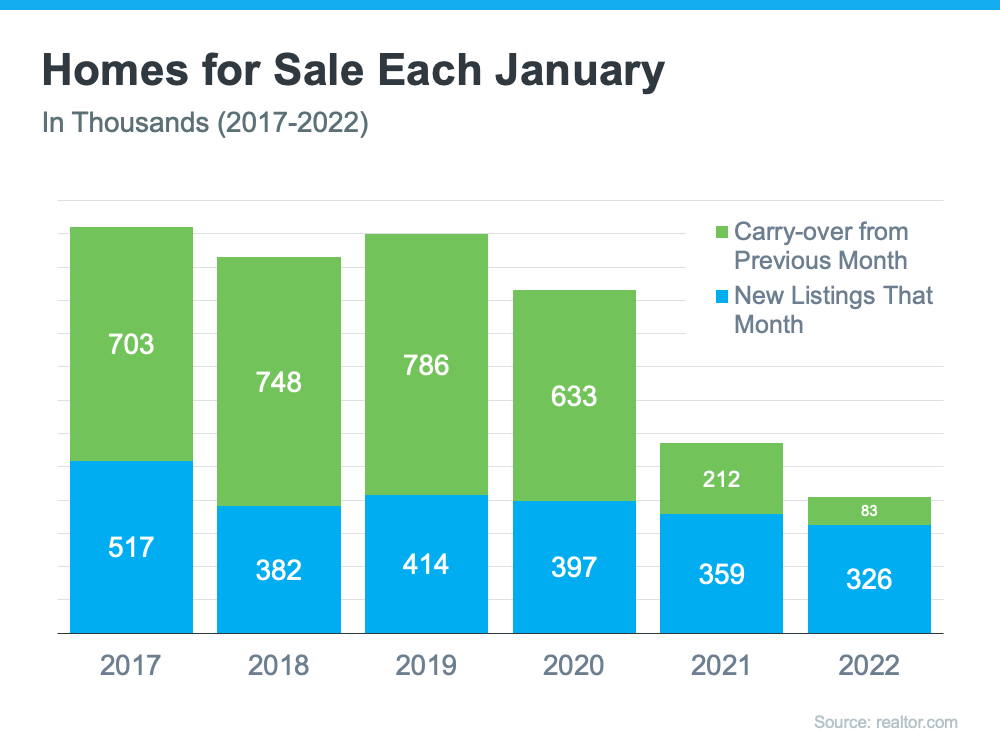

Earlier this month, realtor.com released their inventory data for January. It helps confirm this point. Here’s a graph comparing inventory levels for January over the last six years:

As the graph shows, new listings coming on the market have decreased over the last four years (shown in blue in the graph). The graph also reveals that carry-over inventory has plummeted in recent years. This is because listings are now sold so quickly, they don’t stay on the market long enough to carry over month-to-month (shown in green in the graph). In other words, homes are not staying on the market for months as they had prior to the pandemic. In the report mentioned above, NAR reveals that:

“Seventy-nine percent of homes sold in January 2022 were on the market for less than a month.”

Odeta Kushi, Deputy Chief Economist at First American, explains it like this:

“A higher velocity of sales (lower [Days on Market]) helps to explain a housing market characterized by both higher sales & lower inventory. Many resale transactions are happening so quickly that they ‘flow’ in & then out of the ‘stock’ between the fixed monthly measurement of inventory.”

What Does This Mean for Sellers?

Anyone thinking of putting their home on the market shouldn’t wait. A seller will always negotiate the best deal when demand is high and supply is limited. That’s exactly the situation in the real estate market today.

Later this year, inventory (and by extension, your competition) will increase as many homeowners are waiting to put their homes on the market in the spring and early summer.

In addition, Len Kiefer, Deputy Chief Economist at Freddie Mac, says:

“Housing starts start off 2022 strong, just edging out 2021 for most in January since 2006.”

As these newly built homes are completed, they will also become competition for your house. This gives you a tremendous opportunity right now. Don’t wait for that increase in competition in your area. If you want to sell in 2022 and are ready to start the process, today is the day to list your house.

Bottom Line

If you’re ready to sell, let’s connect to get your house on the market while today’s inventory situation is in your favor.

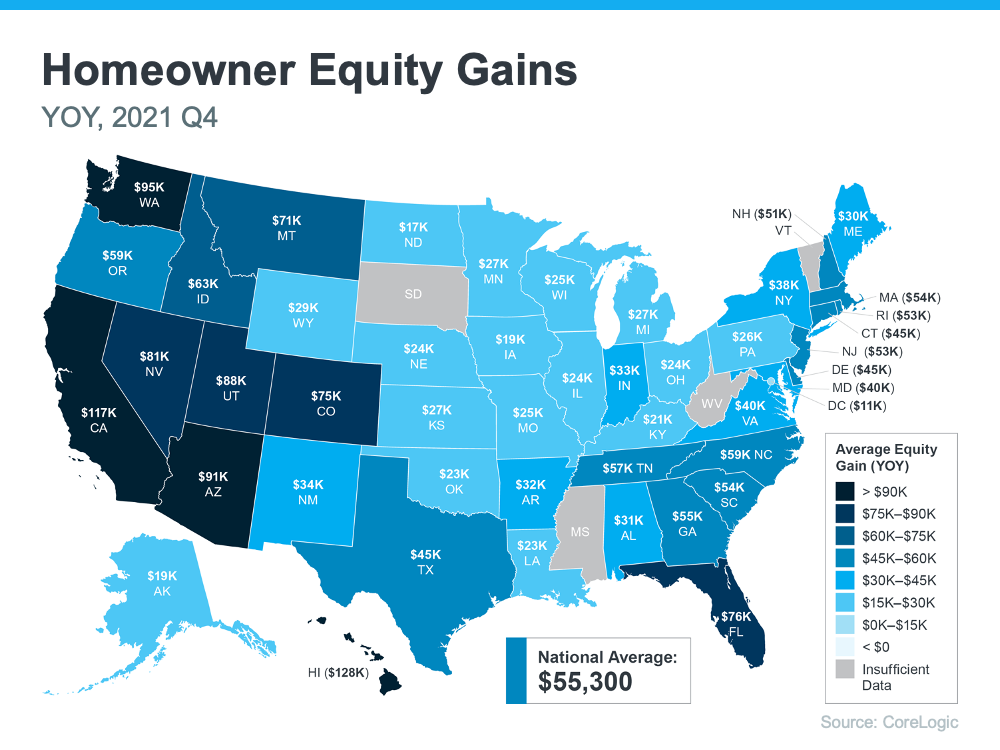

The Average Homeowner Gained More Than $55K in Equity over the Past Year

If you’re a current homeowner, you should know your net worth just got a big boost. It comes in the form of rising home equity. Equity is the current value of your home minus what you owe on the loan. Today, you’re building that equity far faster than you may expect – and this gain is great news for you.

Here’s how it happened. Home values are on the rise thanks to low housing supply and high buyer demand. Basically, there aren’t enough homes available to meet this high buyer interest, so bidding wars are driving home prices up. When you own a home, the rising prices mean your home is worth more in today’s market. And as home values climb, your equity does too. As Dr. Frank Nothaft, Chief Economist at CoreLogic, explains:

“Home prices rose 18% during 2021 in the CoreLogic Home Price Index, the largest annual gain recorded in its 45-year history, generating a big increase in home equity wealth.”

The latest Homeowner Equity Insights from CoreLogic shed light on just how much rising home values have boosted homeowner equity. According to that report, the average homeowner’s equity has grown by $55,300 over the last 12 months.

Want to know what’s happening in your area? Here’s a breakdown of the average year-over-year equity growth for each state based on that data.

How Rising Equity Impacts You

In addition to building your overall net worth, equity can also help you achieve other goals like buying your next home. It works like this: when you sell your house, the equity you built up comes back to you in the sale.

In a market where you’re gaining so much equity, it may be just what you need to cover a large portion – if not all – of the down payment on your next home. So, if you’ve been holding off on selling and worried about being priced out of your next home because of today’s home price appreciation, rest assured your equity can help fuel your move.

Bottom Line

Equity can be a real game-changer if you’re planning to make a move. To find out just how much equity you have in your home and how you can use it to fuel your next purchase, let’s connect so you can get a professional equity assessment report on your house.