Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Why Pre-Approval Is an Important Step for Today’s Homebuyers

Being intentional and competitive are musts when buying a home this season. That’s why pre-approval is so important today. Pre-approval from a lender is the only way to know your true price range and how much money you can borrow for your loan. Peter Warden, Editor of The Mortgage Reports, explains:

“The lender will check out your personal finances and issue you a letter confirming the amount you’re eligible to borrow. This not only gives you a firm budget for house hunting, but also lets sellers know you’re qualified to make an offer.”

Why does that matter so much today? There are many more buyers looking for homes today than there are homes available for sale, and that’s creating some serious competition. According to the National Association of Realtors (NAR), the average home is getting 4.8 offers per sale. As a result, bidding wars are still common.

Your pre-approval gives you a leg up in these situations. That’s because you know exactly what you’re approved to borrow before you write your offer, and it lets the seller know you’re qualified to buy their home. This helps both you and the seller feel confident in what you’re bringing to the table. And that puts you in a better position to potentially win a bidding war.

As Warden puts it:

“There’s another important reason to get preapproved, too. And that’s because there are way more buyers than homes in today’s market — which means you need to be ultra-prepared if you want to win a bidding war. Most sellers are getting multiple offers right now. And most won’t even entertain an offer without a preapproval letter included.”

Every advantage you can gain as a buyer is crucial in a market that’s constantly changing. Mortgage rates are rising, home prices are going up, and lending institutions are regularly updating their standards. You’re going to need guidance to navigate these waters, so it’s important to have a team of professionals, such as a loan officer and a trusted real estate advisor, on your side. They’ll help make sure you’re ready to put your best foot forward.

Bottom Line

Getting pre-approved for a mortgage helps you better understand what you can afford and signals to sellers you’re serious about purchasing their home. Let’s connect so you have the tools you need to succeed as a homebuyer in today’s market.

Using Your Tax Refund To Achieve Your Homeownership Goals This Year

If you’re buying or selling a home this year, you’re likely saving up for a variety of expenses. For buyers, that might include things like your down payment and closing costs. And for sellers, you’re probably working on a bit of spring cleaning and maintenance to spruce up your house before you list it.

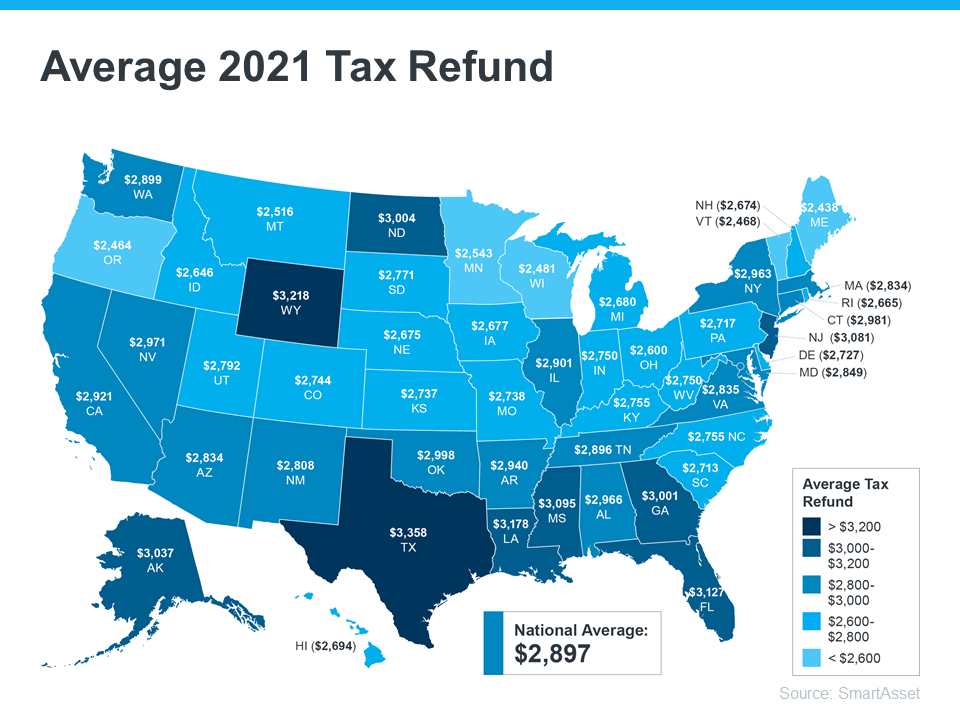

Either way, any money you get back from your taxes can help you achieve your goals. Using a tax refund is a common tactic for buyers and sellers. SmartAsset estimates the average American will receive a $2,897 tax refund this year. The map below provides a more detailed estimate by state:

If you’re getting a refund this year, here are a few tips to help with your home purchase or sale this season.

How Buyers Can Use Their Tax Refund

According to American Financing, there are multiple ways your refund check can help you as a homebuyer. A few include:

- Growing your down payment fund – If you haven’t started saving for your down payment, let your tax refund kick off the process. And if you have a fund already, the money you get back could put you closer to your goal.

- Paying for your home inspection – Your home inspection can save you a lot of headaches down the road by helping you determine the condition of the house. As a buyer, you’ll typically be responsible for paying for your inspection, and it’s definitely worth the investment.

- Saving for closing costs – Closing costs are additional expenses you’ll need to pay once it’s time to close. They average anywhere between 2-5% of the purchase price of your home.

This list is a great start, but it isn’t exhaustive of all the costs you may encounter as you set out on your homebuying journey. The best way to prepare is to work with a trusted real estate professional to make sure you understand what’s to come in the process.

How Sellers Can Use Their Tax Refund

If you own a home and are planning to sell this spring, your tax refund can help you make sure your home is ready to list. Here are a few ways current homeowners can put their tax refund to good use:

- Making small upgrades – NerdWallet provides a list of great ways to use your tax refund, including tackling small projects or boosting your curb appeal to help your home stand out.

- Making repairs – If there’s anything in your house that needs to be fixed, American Financing notes that completing repairs is another great use of that money.

- Buying your next home – Whether you’re selling to move up or downsize, you can use your tax refund to help pay for any costs on the purchase of your next home.

Of course, it’s important to talk with your trusted real estate advisor before taking on any projects. They’ll make sure you can focus on areas that’ll help you receive the best possible price when you sell.

Bottom Line

Funding your home purchase or sale can feel like a daunting task, but it doesn’t have to be. Your tax refund can help you reach your goals. Let’s connect to discuss how you can start on your journey.

Remote Work Trends Mean Flexibility for First-Time Homebuyers

Today’s low inventory can be challenging for homebuyers, especially if you’re looking to purchase your first home. But if you’re one of many people who work remotely, you may have a great opportunity to use the flexibility you have at work to achieve your homebuying goals this year.

In a recent report, Arch Capital Services explains how the ongoing trend of remote work can open up more options for homebuyers:

“. . . This will enable those who are able to work from home on a part-time or hybrid basis to move slightly farther away from job centers. . . . For workers who secure full-time remote jobs, their place of residence will be determined by affordability and personal preferences.”

Basically, working from home is great news if you’re a first-time buyer trying to find a home that meets your needs and budget. Here’s a deeper look at how it could benefit you.

Extra Flexibility in Your Career Means Extra Flexibility in Your Home Search

If your job is 100% remote, you don’t have to be tied to a specific location or office. So, if you’ve been having a hard time finding what you want in your local area, it may be time to expand your search.

One option you could consider is moving to a place where you’ve always wanted to live, like the mountains, beach, or closer to loved ones. When you broaden your search radius to include those locations, it’ll give you additional homes to consider.

It could also allow you to search for a more affordable location where you have more options in your price range. This can help you achieve two goals – saving money and finding additional features that meet your needs. To truly highlight this benefit, a recent First American article discusses the great ways remote work can really help you with your homebuying goals. Ksenia Potapov, Economist at First American, says:

“For potential first-time home buyers, leveraging their house-buying power in more affordable markets can also help them buy more attractive homes – more square footage and rooms, more options for different home styles and neighborhood amenities – increasing the opportunity to find a home that suits their preferences.”

That means you can use your work flexibility to search for homes with the amenities you need at a lower price point.

Bottom Line

Remote work doesn’t just give you expanded flexibility for your career. If you’re no longer tied to a location because of your office, you have a great opportunity to expand your housing search. Let’s connect to explore how this can open up your options.

There Are Several Great Reasons To Consider Buying a Condo Today

If you’re a first-time buyer looking to break into the housing market but struggling to find a home to buy, condominiums (or condos) could be a great alternative for you.

Here are a few reasons condos may be something you’ll want to consider.

Exploring Condos Could Add Options That Fit Your Budget

Supply challenges are a reality across the board in today’s housing market. Broadening your home search to include condos could increase your overall pool of options. Just keep in mind, condos generally differ from single-family homes in average space and floorplans.

In a recent article, Bankrate covers some of these differences:

“Condos are generally more affordable because they come with less space — you likely won’t have your own backyard, for example, and the interior tends to be smaller than the square footage of a single-family home.”

But if the size of a condominium meets your needs, they could match your budget as well. Data from the National Association of Realtors (NAR) shows the difference in the median price for both housing types. For single-family homes, the median price is $363,800. And for condominiums, the median price is lower at $305,400.

So, if budget is top of mind for you, a condominium could be a great fit within your target price range.

Not to mention, buying a condo is a great way to break into the market and start building equity that can help power a future move up. The condo you purchase today may not be your forever home, but it can be a great stairstep that can help you buy your dream home later on.

Find Out if Condo Living Is Right for You

In addition, owning and living in a condo is also a lifestyle choice. While it’s true they may be smaller than single-family homes, the amenities condos provide could be a draw for many buyers. Less space in your home might mean minimal upkeep, lower maintenance, and more time for you to spend doing the things you enjoy.

To understand if condo life is for you, Bankrate recommends asking yourself a few simple questions:

“Hate to mow the lawn and trim the hedges? What about pressure washing your driveway? Are your finances such that having to lay out $5,000 or more for a new roof will be a burden? . . . Condos tend to work best for those comfortable with most of the aspects of apartment living, minus the built-in maintenance.”

Ultimately, talking with an expert real estate advisor is the best first step to determining if condo living might work for you.

Bottom Line

Condominiums are a great option for many buyers, especially those looking to buy their first home. If you’re willing to consider condos in your search, you could find something that’s in line with your target numbers and your needs. To learn more, let’s connect so you have an expert in the condo-buying process on your side.

A Key To Building Wealth Is Homeownership

The link between financial security and homeownership is especially important today as inflation rises. But many people may not realize just how much owning a home contributes to your overall net worth. As Leslie Rouda Smith, President of the National Association of Realtors (NAR), says:

“Homeownership is rewarding in so many ways and can serve as a vital component in achieving financial stability.”

Here are just a few reasons why, if you’re looking to increase your financial stability, homeownership is a worthwhile goal.

Owning a Home Is a Building Block for Financial Success

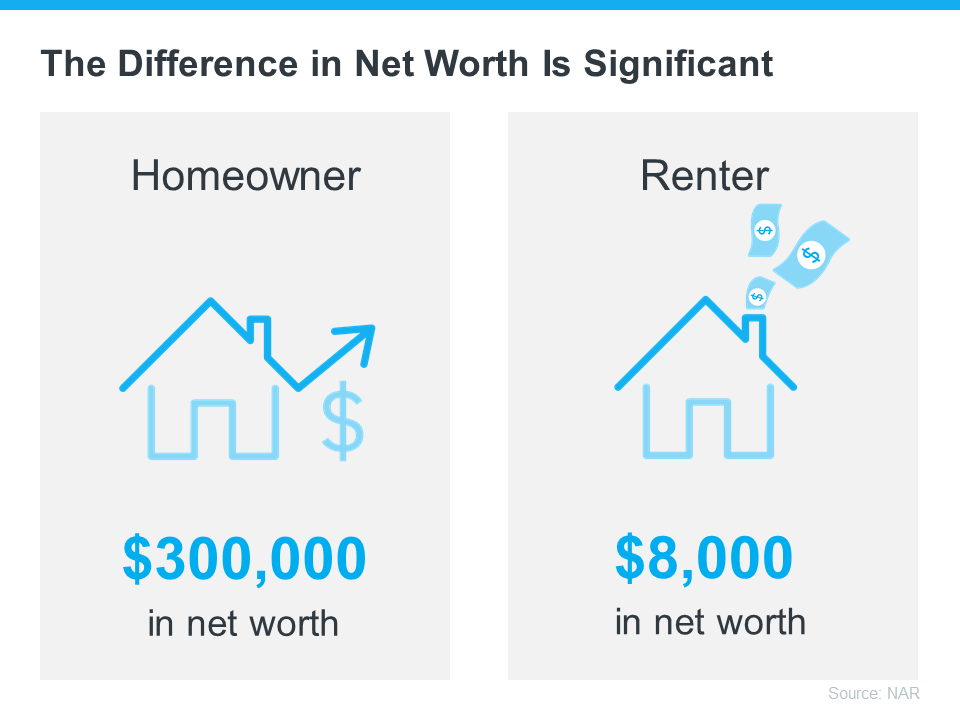

A recent NAR report details several homeownership trends and statistics, including the difference in net worth between homeowners and renters. It finds:

“. . . the net worth of a homeowner was about $300,000 while that of a renter’s was $8,000 in 2021.”

To put that into perspective, the average homeowner’s net worth is roughly 40 times that of a renter (see visual below):

The results from this report show that owning a home is a key piece to the puzzle when building your overall net worth.

Equity Gains Can Substantially Boost a Homeowner’s Net Worth

The net worth gap between owners and renters exists in large part because homeowners build equity. As a homeowner, your equity grows as your home appreciates in value and you make your mortgage payments each month.

In other words, when you own your home, you have the benefit of your mortgage payment acting as a contribution to a forced savings account. And when you sell, any equity you’ve built up comes back to you. As a renter, you’ll never see a return on the money you pay out in rent every month.

To sum it up, NAR says it simply:

“Homeownership has always been an important way to build wealth.”

Bottom Line

The gap between a homeowner’s net worth and a renter’s shows how truly foundational homeownership is to wealth-building. If you’re ready to start on your journey to homeownership, let’s connect today.

What You Can Expect from the Spring Housing Market

As the spring housing market kicks off, you likely want to know what you can expect this season when it comes to buying or selling a house. While there are multiple factors causing some uncertainty, including the conflict overseas, rising inflation, and the first rate increase from the Federal Reserve in over three years — the housing market seems to be relatively immune.

Here’s a look at what experts say you can expect this spring.

1. Mortgage Rates Will Climb

Freddie Mac reports the 30-year fixed mortgage rate has increased by more than a full point in the past six months. And despite some mild fluctuation in recent weeks, experts believe rates will continue to edge up over the next 90 days. As Freddie Mac says:

“The Federal Reserve raising short-term rates and signaling further increases means mortgage rates should continue to rise over the course of the year.”

If you’re a first-time buyer or a seller thinking of moving to a home that better fits your needs, realize that waiting will likely mean you’ll pay a higher mortgage rate on your purchase. And that higher rate drives up your monthly payment and can really add up over the life of your loan.

2. Housing Inventory Will Increase

There may be some relief coming for buyers searching for a home to purchase. Realtor.com recently reported that the number of newly listed homes has grown for each of the last two months. Also, the National Association of Realtors (NAR) just announced the months’ supply of inventory increased for the first time in eight months. The inventory of existing homes usually grows every spring, and it seems, based on recent activity, the next 90 days could bring more listings to the market.

If you’re a buyer who has been frustrated with the limited supply of homes available for sale, it looks like you could find some relief this spring. However, be prepared to act quickly if you find the right home.

If you’re a seller, listing now instead of waiting for this additional competition to hit the market makes sense. Your leverage in any negotiation during the sale will be impacted as additional homes come to market.

3. Home Prices Will Rise

Prices are always determined by supply and demand. Though the number of homes entering the market is increasing, buyer demand remains very strong. As realtor.com explains in their most recent Housing Report:

“During the final two weeks of the month, more new sellers entered the market than during the same time last year. . . . However, with 5.8 million new homes missing from the market and millions of millennials at first-time buying ages, housing supply faces a long road to catching up with demand.”

What does that mean for you? With the demand for housing still outpacing supply, home prices will continue to appreciate. Many experts believe the level of appreciation will decelerate from the high double-digit levels we’ve seen over the last two years. That means prices will continue to climb, just at a more moderate pace. Most experts are predicting home prices will not depreciate.

Won’t Increasing Mortgage Rates Cause Home Prices To Fall?

While some people may believe a 1% increase in mortgage rates will impact demand so dramatically that home prices will have to fall, experts say otherwise. Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, says:

“What I will caution against is making the inference that interest rates have a direct impact on house prices. That is not true.”

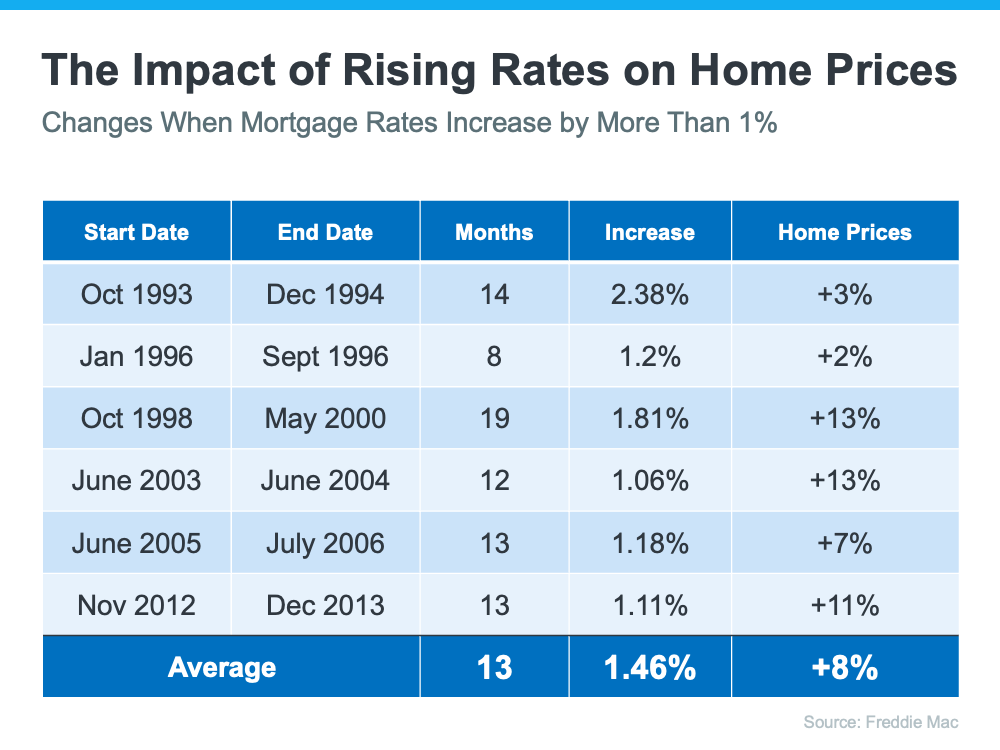

Freddie Mac studied the impact that mortgage rates increasing by at least 1% has had on home prices in the past. Here are the results of that study:

As the chart shows, mortgage rates jumped by at least 1% six times in the last thirty years. In each case, home values increased.

So again, if you’re a first-time buyer or a repeat buyer, waiting to buy likely means you’ll pay more for a home later in the year (as compared to its current value).

Bottom Line

There are three things that seem certain going into the spring housing market:

- Mortgage rates will continue to rise

- The selection of homes available for sale will modestly improve

- Home prices will continue to appreciate, just at a slightly slower pace

If you’re thinking of buying, act now before mortgage rates and home prices increase further. If you’re thinking of selling, your best bet may be to sell soon so you can beat the increase in competition that’s about to come to market.

The Many Benefits of Homeownership

The past two years have taught us the true value of homeownership, especially the stability and the feeling of accomplishment it can provide. But homeownership has so much more to offer. Here’s a look at a few of the non-financial and financial benefits of owning a home. If you’re looking to buy a home today, think about all the ways homeownership can impact your life.

Homeownership Has Impactful Personal and Emotional Benefits

Owning your home gives you a significant sense of pride because it’s a space that is truly yours. And as a homeowner, you can customize your home to your heart’s desire. Having a space you’ve put your stamp on enhances the pride and sense of ownership you may feel.

And that sense of ownership can extend beyond your shelter to help create social, community, and civic benefits as well. That’s because the average homeowner stays in their home for longer than just a few years. That means you’ll naturally feel a stronger connection to the community around you the longer you live there. This can help you experience a greater sense of belonging and a greater stake in your community as a whole. As the National Association of Realtors (NAR) says:

“Living in one place for a longer amount of time creates an obvious sense of community pride, which may lead to more investment in said community.”

Owning a Home Is a Significant Step Toward Financial Stability

In a financial sense, homeowners benefit from home price appreciation, equity gains, and having a shield against some of the effects of inflation. These benefits can have a big impact on your life. As you gain equity through home price appreciation and paying down your mortgage, you build your net worth. And in times of inflation, your 30-year fixed-rate mortgage can help you stabilize one of your largest monthly expenses for the duration of your loan.

Lawrence Yun, Chief Economist for NAR, explains how you can start to see these lasting effects of homeownership as soon as you make your purchase:

“Owning a home continues to be a proven method for building long-term wealth. . . . Home values generally grow over time, so homeowners begin the wealth-building process as soon as they make a down payment and move to pay down their mortgage.”

Knowing you’ve made a good investment soon after your purchase is powerful. And that may give you confidence in your decision to buy a home.

Bottom Line

The benefits of owning a home are foundational. As a homeowner, you can feel proud of the space you call home and know you’ve made a sound financial investment. To learn how homeownership can help you, let’s connect to start the conversation today.

The Difference Between Renting and Owning

![The Difference Between Renting and Owning [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/02/24130106/20220225-MEM-1046x2279.png)

Some Highlights

- If you’re deciding whether to rent or buy, consider the many financial benefits that come with owning a home.

- As a renter, you build your landlord’s wealth and face rising costs. As a homeowner, you build your own net worth and can lock in your monthly payments for the length of your loan.

- If you’re weighing your options, remember that owning a home is a decision that has considerable financial perks. If you want to learn more, let’s connect to talk about the perks of homeownership.

Are You Wondering if This Is the Year To Buy a Home?

Every year, many renters ask themselves the same question: Should I continue renting, or is it time to buy a home? If you’re a renter, chances are you’ve asked yourself that question at least once, and it’s likely because you’ve faced an increase in your monthly housing costs over time. After all, according to Census data, rents have risen consistently for decades.

To make an informed and powerful decision, the first step is understanding what’s happening in today’s housing market so you can determine which option is the better long-term financial decision for you.

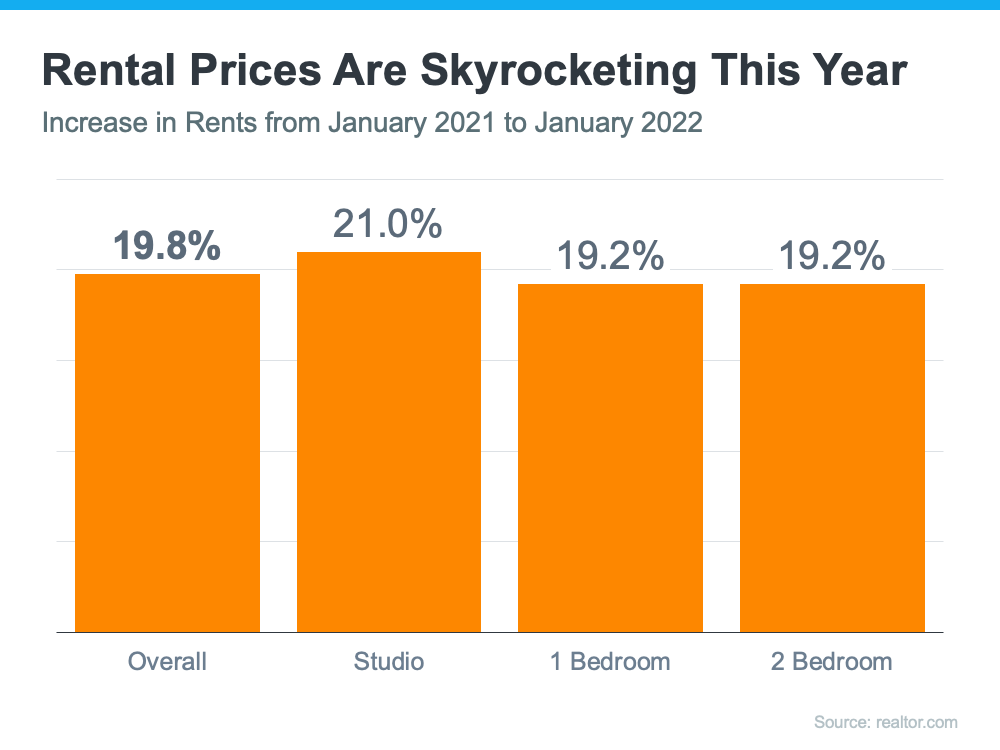

Rents Are Going Up Again This Year

Rents are skyrocketing right now. Data from realtor.com shows just how much rental prices are surging throughout the country. The graph below highlights rental unit price increases over the past year:

If you’re a renter and plan on signing a new lease, your monthly costs are likely to go up when you do. Those rising costs can have a big impact on your financial goals, including any plans you’re making to save for a home purchase.

Homeownership Offers Stable Monthly Costs

Of course, one of the key benefits of owning your home is that you’re able to lock in and stabilize your payments for the duration of your loan. That’s not the case when you rent.

While rents are already on the rise, there’s a good chance many people will see their rental costs increase even more this year. As Danielle Hale, Chief Economist at realtor.com, says:

“With rents already at a high and expected to keep going up, rental affordability will increasingly challenge many Americans in 2022. For those thinking about making the transition from renting to buying their first home, rising rents will remain a motivating factor. . . .”

So, if you’re ready to become a homeowner, waiting any longer may not make financial sense. Instead, escape the cycle of rising rents and enjoy the many benefits that come with homeownership today.

Bottom Line

Starting your journey towards homeownership can pay off significantly this year. If you’re financially ready today, let’s connect so we can discuss your options.

Don’t Get Caught Off Guard by Closing Costs

As a homebuyer, it’s important to plan and budget for the expenses you’ll encounter when you purchase a home. While most people understand the need to save for a down payment, a recent survey found 41% of homebuyers were surprised by their closing costs. Here’s some information to help you get started so you’re not caught off guard when it’s time to close on your home.

What Are Closing Costs?

One possible reason some people are surprised by closing costs may be because they don’t know what they are or what they cover. According to U.S. News and World Report:

“Closing costs encompass a variety of expenses above your property’s purchase price. They include things like lender fees, title insurance, government processing fees, upfront tax payments and homeowners insurance.”

In other words, your closing costs are a collection of fees and payments made to a variety of individuals and organizations who are involved with your transaction. According to Freddie Mac, while they can vary by location and situation, closing costs typically include:

- Government recording costs

- Appraisal fees

- Credit report fees

- Lender origination fees

- Title services

- Tax service fees

- Survey fees

- Attorney fees

- Underwriting Fees

How Much Will You Need To Budget for Closing Costs?

Understanding what closing costs include is important, but knowing what you’ll need to budget to cover them is critical to achieving your homebuying goals. According to the Freddie Mac article mentioned above, the costs to close are typically between 2% and 5% of the total purchase price of your home. With that in mind, here’s how you can get an idea of what you’ll need to cover your closing costs.

Let’s say you find a home you want to purchase for the median price of $350,300. Based on the 2-5% Freddie Mac estimate, your closing fees could be between roughly $7,000 and $17,500.

Keep in mind, if you’re in the market for a home above or below this price range, your closing costs will be higher or lower.

What’s the Best Way To Make Sure You’re Prepared At Closing Time?

Freddie Mac provides great advice for homebuyers, saying:

“As you start your homebuying journey, take the time to get a sense of all costs involved – from your down payment to closing costs.”

The best way to understand what you’ll need at the closing table is to work with a team of trusted real estate professionals. An agent can help connect you with a lender, and together they can provide you with answers to the questions you might have.

Bottom Line

In today’s real estate market, it’s more important than ever to make sure your budget includes any fees and payments due at closing. Let’s connect so you have the knowledge you need to be confident going into the homebuying process.